Japan, China and Hong Kong step up stablecoin push

Major Asian economies are accelerating their stablecoin initiatives, with notable moves from Japan and China over the past week.

Japan’s top financial regulator is reportedly preparing to approve the country’s first yen-pegged stablecoin within the year. The token, issued by fintech startup JPYC, will be backed by liquid assets such as government bonds.

According to finance outlet Nikkei, JPYC is expected to register as a money-transfer business this month and aims to issue 1 trillion yen (about $6.81 billion) worth of stablecoins over the next three years.

Interest in stablecoins is rising globally, especially after US President Donald Trump signed the GENIUS Act on July 18, establishing a federal framework for dollar-denominated tokens. Even China — which has banned most crypto-related activities — is reportedly considering a yuan-backed stablecoin. Reuters reported on Wednesday that China’s State Council is set to review a roadmap that includes yuan-denominated stablecoins as part of its renminbi internationalization strategy. While reports indicate that Beijing has signaled openness toward offshore stablecoins, it continues to warn against the promotion of such products.

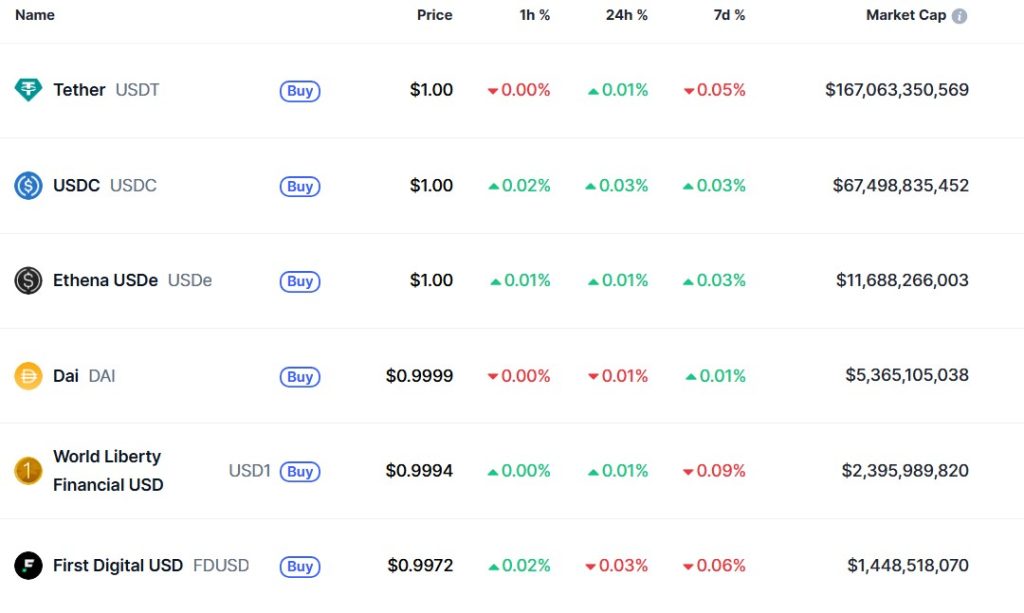

For now, the US dollar dominates the stablecoin market. Tether’s USDt and Circle’s USDC both rank among the top ten cryptocurrencies and have a combined market capitalization exceeding $234.5 billion, according to CoinGecko data.

The GENIUS Act is expected to reinforce this dominance by requiring issuers to maintain a 1:1 reserve ratio in highly liquid assets like US Treasuries or cash. Zhang Monan, deputy head of the Institute of American and European Studies at the China Center for International Economic Exchanges, argued in a commentary for Sina Finance that this framework further entrenches the global influence of the dollar and US Treasuries.

Zhang added that Hong Kong is a strategic player capable of challenging dollar hegemony. The city’s stablecoin regulations have already taken effect, and multiple firms, including Chinese tech giants, are preparing to issue compliant tokens.

“Although in the short term the launch of compliant offshore renminbi stablecoins in Hong Kong faces bottlenecks, Hong Kong’s stablecoin policy framework has reserved space for this. In the future, if a stablecoin pegged to offshore renminbi can be launched, it will open up an entirely new path for renminbi internationalization,” a machine translation of Zhang’s commentary reads.

India’s long-awaited crypto tax reform enters talks

India’s tax authority is reconsidering the country’s crypto tax policy and has begun asking industry players whether the current regime is driving businesses offshore, the Economic Times reported.

India imposes one of the world’s harshest crypto tax regimes: a flat 30% levy on capital gains and a 1% tax deducted at source (TDS) on all transactions. Authorities have long taken a hostile stance toward the sector. In 2018, the Reserve Bank of India (RBI) barred banks from serving crypto firms, a move struck down by the Supreme Court in 2020.

In mid-2022, the government introduced the punitive tax framework. Within months, Indian exchanges reported a collapse in activity, with trading volumes plunging by 90%–95%.

Former RBI governor Shaktikanta Das was one of the most vocal opponents of crypto and resigned in December 2024, just as major economies softened their stances following Trump’s presidential election. Das’s successor has continued the hard line. Current governor Sanjay Malhotra has said there is “no change” in the central bank’s opposition to cryptocurrencies.

Philippines quashes crypto ban but disappoints stock traders

The Philippines did not ban cryptocurrency trading, the country’s Securities and Exchange Commission said.

The market regulator was pushed to isse a clarification after the new rules on crypto exchanges took effect. The nation has since cracked down on unregistered exchanges,flagging 10 in the process.

But that has raised confusion among local investors on whether cryptocurrency trading itself is permitted.

“The [Crypto Asset Service Providers] rules do not prohibit cryptocurrency trading or investment. Rather, they require platforms to obtain the appropriate registration and licenses before offering their services in the Philippines,” the SEC said in its advisory statement.

Though the clarification is good news for local traders, Joey Roxas, president of Eagle Equities has a different perspective.

“I’m a little saddened by that,” Roxas told local broadcaster ONE News on Monday.

“One thing that can get this market moving faster, higher and getting more attention from the general public is a ban on crypto. Because it does not do anything at all for the Philippine economy — zero. There’s nothing.”

Roxas argued that the crypto market does not contribute taxes to the local economy, unlike a “healthy” stock market.

Philippines was ranked eighth in Chainalysis’s 2024 crypto adoption index. During the pandemic, play-to-earn non-fungible tokens (NFT) game Axie Infinity became a platform for players to earn at home, offering a financial lifeline for many in a displaced workforce.

S. Korea presidential aide not guilty on false reporting of crypto holdings

Kim Nam-kuk, South Korea’s presidential secretary for digital communications and a former Democratic Party lawmaker, has been acquitted on appeal of charges that he falsified property disclosures to conceal nearly 10 billion won in cryptocurrency holdings.

On Thursday, a three-judge panel at the Seoul Southern District Court upheld his initial not-guilty verdict, rejecting the prosecution’s claim of “obstruction of official duties by deceit.”

The judges acknowledged that Kim had not fully reported his crypto assets but said the omission stemmed from a “legislative gap.” The Public Officials Ethics Act, they noted, does not clearly require the disclosure of virtual assets or set precise reporting standards.

After the ruling, Kim denounced the prosecution, calling the case a “blatantly political indictment.”

Prosecutors had accused Kim of concealing holdings in 2021 and 2022 by transferring about 950 million won into a bank account disguised as stock-sale proceeds and converting the remaining 8.95 billion won into coins, then underreporting his wealth. They alleged he used the same method in 2023.

Both trial courts concluded that because cryptocurrency was not legally recognized as a reportable asset at the time, Kim could not be held criminally liable.

Yohan Yun

Disclaimer

Cointelegraph Features and Cointelegraph Magazine publish long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team and selected external contributors with subject-matter expertise.

All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Contributions from external writers are commissioned for their experience, research or perspective and do not reflect the views of Cointelegraph as a company unless explicitly stated.

Content published in Features and Magazine does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence. The selection, commissioning and publication of Features and Magazine content are not influenced by advertisers, partners or commercial relationships.

They solved crypto’s janky UX problem — you just haven’t noticed yet

Crypto has finally become user-friendly thanks to intents, chain abstraction, passkeys and other new tech — and it’s already live.

Read more

SEC’s U-turn on crypto leaves key questions unanswered

The SEC dropped a raft of crypto cases and Trump’s talking up a crypto reserve. But lawyers warn crypto laws and regulations remain unclear.

Read more9 weirdest AI stories from 2025: AI Eye