Unstablecoins: Depegging, bank runs and other risks loom

MagazinePublishedMar 1, 2023

How stable are stablecoins? Growing doubts over reserves and antagonistic regulation mean a bank run is possible.

Stablecoins are entering a period of great uncertainty following the U.S. Securities and Exchange Commission labeling BUSD an “unregistered security” and ordering Paxos to stop minting new tokens.

Do these moves signal a wider war by U.S. regulators on stablecoins? Could the SEC declare all stablecoins securities, or is BUSD a special case?

Independent crypto reporter Amy Castor, who has been covering cryptocurrencies since 2016, believes the BUSD crackdown is aimed squarely at the world’s largest crypto exchange, Binance:

“Going after Paxos-issued BUSD is part of a much broader crackdown on crypto. They are going after the jugular, and they plan to cut off the blood supply.”

She continues, “They want to kill BUSD because BUSD is critical to Binance, which is the largest offshore crypto casino. Binance auto-converts every U.S. dollar and stablecoin to BUSD (the pegged version). Now they’ll have to find something else to auto-convert to… probably Tether. So, maybe the authorities will target Tether next, something that has been a long time coming.”

Even before these regulatory moves on BUSD, various indicators showed a large redemption of stablecoins between September 2022 and February 2023. Could a bank run on redemptions lead to a significant stablecoin depegging event? Some think so, pointing to convoluted cash reserves held by stablecoin treasuries, the need for third-party audits, and the uneasy relationship between stablecoins and the U.S. Treasury.

So, how stable are stablecoins?

BUSD has looked more wobbly than is ideal lately, but it’s nothing too serious so far. (Coinmarketcap)

Types of stablecoins

A stablecoin is just a token pegged to the value of an asset, an algorithm or a fiat currency. They’re hugely popular as a de facto working capital for traders or as a safe haven to cash out, with the total value settled using stablecoins last year hitting $7 trillion — that’s more than Mastercard.

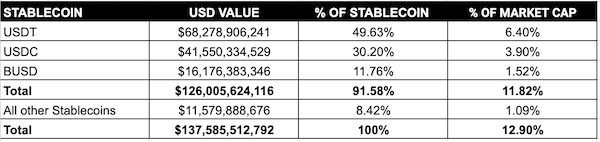

As of Feb. 10, the three big dollar-denominated fiat-collateralized stablecoins (USDT, USDC and BUSD) represent almost 12% of the total crypto market cap and account for 91.58% of the entire stablecoin supply.

The market for stablecoins as of Feb. 10, 2023. Source: CoinGecko

Given that the U.S. dollar is the global reserve currency, stablecoins gravitate toward it as a peg, but there are other categories. Asset-collateralized stablecoins use real-world assets, such as gold, for collateral to maintain stable price levels, like with Paxos’ PAXG.

Stablecoins collateralized by baskets of cryptocurrencies are backed by other cryptocurrencies and stablecoins, which might themselves be asset-collateralized or fiat-collateralized. MakerDAO’s Dai invented this model. Dai is an algo-stablecoin backed by various other stablecoins, Ether and wrapped Bitcoin.

Most controversial, algorithmic stablecoins combine a decentralized minting mechanism with economic incentives to maintain their peg to a target value, usually the dollar. Automated processes — in theory — keep their value close to that target. Clearly still experimental, price peg algorithms let traders mint and burn coins as needed to maintain their price.

In May 2022, Terra’s algorithmic stablecoin, UST, famously depegged because of its circular dependency design. Multiple wallets exploited vulnerabilities in the Terra ecosystem and its automated procedures. The UST stablecoin — and its collateral token, LUNA — collapsed, dragging the market into another winter.

The bad news is that fiat-collateralized stablecoins can also depeg in a bank run.

Stablecoins are tokens most often pegged to the dollar. Source: Pexels

Depegging and cash reserves

Stablecoins move up and down with their dollar pegs constantly, within a predefined range of normal movement. A small range of fluctuations is normal, but significant movement for a sustained duration leads to depegging concerns.

“The real problem is the actual pegging itself,” says Sinclair Davidson, an economist at RMIT University. “Creating a fixed exchange rate regime is tried and tested. Nation-states have failed, and now, the private sector is trying to do the same. Almost all pegged exchanges in human history have been subject to attacks.”

Bank runs are a self-fulfilling prophecy, as customers race to withdraw funds in a panic before others beat them to it. Stablecoins can depeg and potentially collapse at hyperspeed, as they are sold on hundreds of crypto exchanges and traded 24/7.

Some collateral is less liquid, and valuations of stated collateral may change based on the price of the underlying assets and the costs of converting it to cash. Even USDT, USDC and BUSD face risks that are hard for seasoned crypto investors to see.

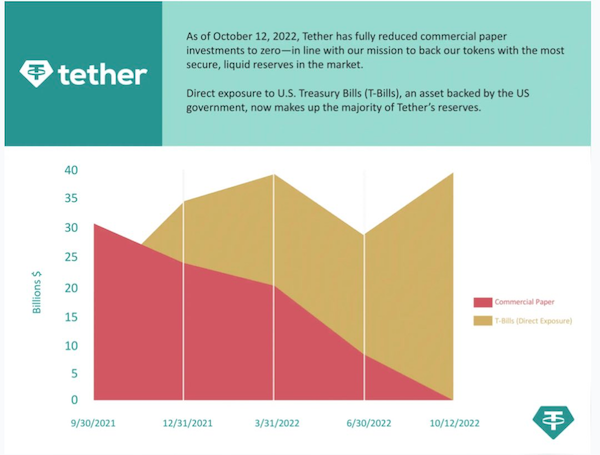

Tether says it has reduced its risky commercial paper to zero. Source: Tether

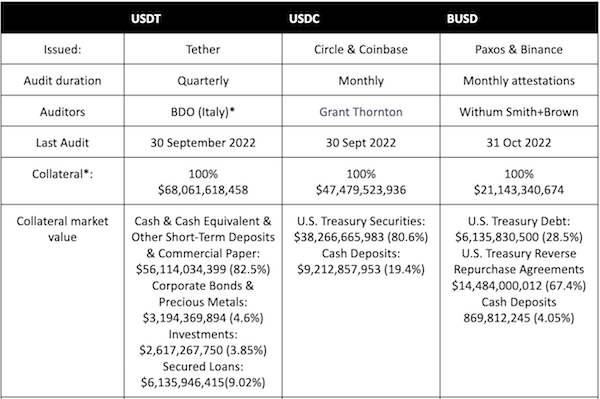

For example, USDT’s collateral incorporates secured loans (8.7%) and other investments (4%), with unknown information on their maturity details or underlying security. USDT also lists corporate bonds and precious metals (5.1%) in its audited reports.

The USDT report dated December 2022 shows only 58.5% of cash reserves in U.S. Treasurys, with an average maturity date of fewer than 60 days. By comparison, USDC and BUSD have 100% of their collateral with the U.S. Treasury Department as bonds and also strong cash deposits.

So, as fiat-collateralized stablecoins grow in market cap, third-party audits verifying “proof of collateral” will become a crucial part of the industry. They are already a topical issue since the FTX collapse and for DAO treasuries, whose native tokens might be highly volatile. So, a bank run depeg is plausible.

Recent redemption depeg threats

Whale Alert — a blockchain analytics system reporting token burns and mints for USDT, USDC and BUSD — records that from late 2022 to early 2023, there was a significant increase in stablecoin redemptions, predominantly in BUSD.

The declining market caps of these stablecoins confirm this. Since their all-time supply highs in November 2022 until Feb. 10, 2023, a combined $9.8 billion — or 7.23% of stablecoins — were redeemed and exited the crypto market. Before Feb. 13’s SEC actions, BUSD already represented over 31% of redemptions.

90-day market cap charts for fiat-collateralized stablecoins USDT, USDC and BUSD as of Feb. 10, 2023. Source: CoinGecko

Crypto investors might not have noticed the decrease in stablecoin dominance in the crypto market. Stablecoins slid down from a 16.5% market cap to 12.9% over the past three months, removing almost $10 billion of liquidity from the market.

Large-scale redemptions have meant reduced liquidity for stablecoins. These fiat-collateralized or Treasury-collateralized stablecoins might stress-test the current cash-on-hand ratios (the 20% range in the case of USDC, 6% for BUSD, and an unknown ratio for USDT).

So, “fiat-collateralized” may be a misnomer, as up to 80% of the collateral is held in 30-day fixed-maturity Treasury bills, with only 20% held in liquid cash deposits.

Stablecoins are likely to remain relatively stable during a market crash. However, large withdrawals of stablecoins on centralized exchanges to self-custody wallets or into fiat may cause delays. CEXs, the fiat on- and off-ramps, may not have sufficient stablecoins to meet withdrawals, or the volume of stablecoin redemptions may be larger than the cash on hand for instant redemptions.

The latter example is untested but possible. On Dec. 13, 2022, Binance paused over $1.6 billion in USDC withdrawals, as the exchange didn’t have the USDC on hand to fund said withdrawals.

The delay was around eight hours, but these redemption delays have the potential to temporarily depeg a stablecoin.

Third-party audits needed

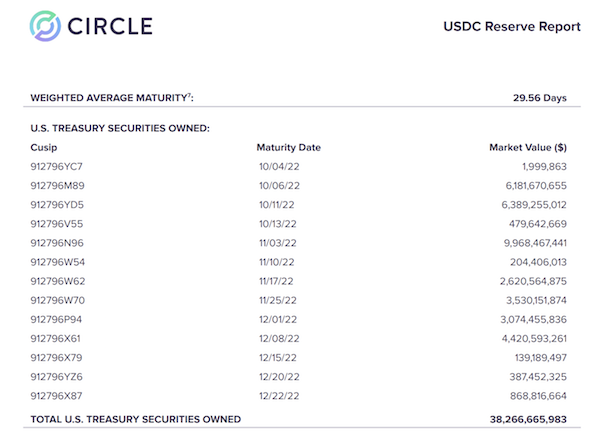

According to the September 2022 attestation report from Grant Thornton — USDC’s auditors — only 19.4% of USDC was held as cash deposits. The remaining 80.6% was held as “reserve assets,” a range of U.S. securities with a weighted average maturity date of 29.6 days.

“Report of Independent Certified Public Accountants.” Source: Circle

Therefore, trust in stablecoin auditors is paramount — and there’s not much trust around. Many in the crypto community, for example, have reservations about Tether, which has engaged six different accounting firms since 2017. It has also been fined $41 million by the Commodity Futures Trading Commission for publishing false reserves data. The CFTC said that rather than having $1 of backing for every 1 USDT — as Tether claimed — Tether at one point had $61.5 million while having more than 442 million USDT circulating.

Tether’s accounting firm, Friedman LLP, was accused by the SEC of “serial violations of the federal securities laws” as well as improper professional conduct and fined $1 million.

Castor highlights Tether’s tricky actions when it opened an account at Noble Bank on the morning of Sept. 15, 2017:

“Bitfinex transferred $382 million into Tether’s account from their account, and then Tether showed Friedman LLC their new account balance at 8:00 pm that day.”

Crucially, while stablecoin providers have engaged independent auditors, there are significant differences between attestations and full audits. For example, Grant Thorton’s September 2022 report on USDC’s financials is called an “attestation report,” not a full audit. In the introduction, there is a disclaimer that Circle self-attests its own financial reporting:

“Circle Internet Financial, LLC’s management is responsible for its assertion. Our responsibility is to express an opinion on the Reserve Information in the accompanying USDC Reserve Report based on our examination.”

Castor points out that “An attestation is a snapshot. It means that maybe the stablecoins were fully backed for a minute. That’s about all it means.” She continues:

“In a full audit, you want to look for unreported liabilities. You also want to check the reserve over time — to make sure the stablecoin issuer doesn’t pull the wool over the accountant’s eyes as Tether did in 2017.”

In summary, the next bank run could depeg USDC if more than 20% of cash deposits are required to fulfill customer redemptions in a short space of time, and contagion could spread quickly. The market cap for stablecoins is now too big for the U.S. government to ignore.

Data from published attestations from Tether, Circle and Paxos.

What happened with BUSD?

In February, the SEC issued a Wells notice (meaning it is considering enforcement action) to Paxos, alleging that BUSD is an unregistered security. Paxos can now respond with its case against being sued. But the SEC has stated that it considers most crypto assets securities, including stablecoins.

“We don’t know exactly why the SEC is targeting BUSD because the Wells notice is not public and the SEC has not filed a complaint yet,” Castor tells Magazine.

“So, we don’t know if there is something special about BUSD that the SEC doesn’t like or if they are planning to target all stablecoins. Certainly, the latter is what everyone in crypto is afraid of.”

A rumor the SEC had sent Circle a Wells notice over USDC was quickly denied.

According to Castor, BUSD issued by Paxos is not an “investment contract” according to the Howey test (which determines what a security is under U.S. law) because there’s no expectation of profit. However, the Securities Act of 1933 includes more than 30 features that define a security.

“We also can’t rule out that the SEC may also be targeting BUSD because it doesn’t like the relationship that Paxos has with Binance.”

She continues, “Paxos’ relationship with Binance and the Binance-peg BUSD does not sit well with the NYDFS, so the NYDFS has asked Paxos to stop issuing BUSD and proceed with an orderly redemption, which means KYC/AML.”

To clarify, there are two forms of BUSD: the Paxos-issued BUSD, which is an Ethereum ERC-20 token, and a second version called Binance-Peg BUSD that is issued by Binance and is run on a plethora of other blockchains.

“While Paxos-issued BUSD is backed by real dollars in bank accounts, the Binance-Peg BUSD is a stablecoin of a stablecoin. Sometimes it’s properly backed, and sometimes it’s not,” Castor says. That could be the SEC’s concern.

Paxos will only redeem BUSD on the Ethereum blockchain, not wrapped BUSD. Some believe the price of Bitcoin has spiked because users who cannot redeem their BUSD are buying Bitcoin to cash out.

Castor also thinks this BUSD redemption is causing issues with banks, as $16 billion is getting sucked out of the banks. Paxos keeps deposits in a few banks, including the two major crypto banks, Silvergate and Signature. “Silvergate is already under fire because it got a $4.3 billion bailout from a Federal Home Loan Bank. Following the FTX implosion, Silvergate’s other crypto customers took out their money in a panic, and the bank lost $8.1 billion in deposits,” she says.

“They weren’t insolvent — they had loans to cover those deposits but didn’t have cash-on-hand liquidity. So, they got a $4.3 billion loan from the Fed.”

This is an example of the sort of contagion the U.S. government is worried about and explains why it has been busy trying to erect firewalls between traditional banks and the crypto industry.

Davidson cautions, however, that a certain amount of issues are to be expected with any innovative financial technology.

“Failure here in the crypto industry shouldn’t be condemned as showing how terrible crypto is. This has always happened in human history. Not to say stablecoins won’t succeed, but we should still expect a lot of trial and error,” says Davidson.

The U.S. Treasury has concerns about the impact of stablecoins. Source: Pexels

U.S. Treasury and contagion risk

Stablecoins are also becoming substantial holders of U.S. securities, creating risks for not only the crypto markets but also bondholders and the U.S. government.

According to the U.S. Department of Treasury, the combined market cap of U.S. dollar stablecoins as of October 2022 would make them the 16th-largest holder of U.S. securities, behind Singapore and ahead of Saudi Arabia, Korea, Norway, Germany and 20 other nations.

A majority of the collateral held by these stablecoins was in U.S. Treasury securities. A run on stablecoins could spill into bond markets, as issuers of these cryptocurrencies may have to sell U.S. Treasurys to honor redemptions, warns Eswar Prasad, an economics professor at Cornell University:

“And a large volume of redemptions even in a fairly liquid market can create turmoil in the underlying securities market. And given how important the Treasury securities market is to the broader financial system in the U.S., [...] I think regulators are rightly concerned.”

Davidson agrees. “Depegging can spill over into non-crypto markets. As investors sell off crypto assets, they also sell off non-crypto assets. Over time, we will expect to see the correlation to rise, similar to all risky assets.”

The correlation takes place, says Davidson, “because some groups of individuals increasingly own both classes of assets.”

This complex relationship between stablecoins and U.S. Treasury securities as collateral means regulation is coming. While the SEC can attempt to regulate via enforcement, Congress will have the final word.

Regulation imminent

Just before Christmas 2022, outgoing Pennsylvania Senator Pat Toomey introduced a bill titled “Stablecoin Transparency of Reserves and Uniform Safe Transactions Act of 2022” to the U.S. Senate. The bill included plans for standardized disclosure requirements and attestations by registered accounting firms for stablecoin issuers. It also proposed a licensing system for stablecoin issuers and improved consumer protections by prioritizing consumers if a stablecoin issuer became insolvent.

Ari Redbord, head of legal and government affairs at TRM Labs — a blockchain intelligence company — tells Magazine that blockchain’s transparency is actually quite beneficial for regulators and law enforcement agencies and “can ultimately help avoid illicit activity, maintain market integrity and mitigate systemic risks.”

Redbord was formerly a senior adviser to the deputy secretary and the undersecretary for terrorism and financial intelligence at the Treasury. He notes that even the collapse of Terra didn’t affect the broader economy.

“Policymakers such as the U.S. Treasury secretary — even in response to Terra — made clear that stablecoins do not, today, pose a significant risk to the broader financial system.”

While Congress could not reach an agreement on legislation last year, Redbord points out that “stablecoins are one of the few areas on which we see general agreement between policymakers and industry.”

“We are likely to see progress on a bill on stablecoins this year that requires 1:1 segregated reserves, meaningful audits and other consumer protection controls,” he says. In this more optimistic view, regulatory guidance will help the industry and lead to broader adoption.

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph publishes long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team with subject-matter expertise. All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Some articles contain affiliate links, from which Cointelegraph may earn a commission. These relationships do not influence which products we review or our editorial conclusions. Content published in here does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence.

More on the subject