Every four years, a few months after the Bitcoin halving, the blockchain ecosystem undergoes heightened public scrutiny. Typically lasting over a year, this period is driven by fundamental economic principles: When an asset’s supply is reduced while demand remains steady or increases, its value generally rises. Historically, this supply shock has triggered Bitcoin-led market appreciation, sparking increased interest and participation from users, developers, investors and policymakers.

During these post-halving periods, the blockchain industry has showcased its projects, technological innovations and potential utilities. None of the prior cycles have yielded a blockchain application that unequivocally eclipses existing technologies in any specific area. Yet, blockchain’s core strengths — immutability, data transparency and user asset sovereignty enabled by private key encryption — continue to attract innovators. These features have been creatively applied across numerous sectors, including borderless payment systems, DeFi, NFTs, gaming systems with recorded in-game assets, fan and loyalty tokens, transparent grants and charity disbursement systems, agricultural subsidies and loan tracking.

While past cycles have highlighted blockchain’s potential, the next period promises to audition new use cases, as detailed below.

Lessons from past halving cycles

The 2012 post-halving period highlighted the potential for non-mediated, borderless payment systems. Before Bitcoin, intermediated payments and sluggish cross-border transactions were the norm — international transfers took days and check clearances were equally slow. Bitcoin hinted at a future of seamless payments, and early adopters tracked the number of businesses accepting Bitcoin. Still, scalability issues and rising transaction costs limited this utility. Ironically, many blockchain networks penalized their success through fee structures that hindered growth. This cycle ended with security breaches, notably the Mt. Gox hack 20 months after the halving.

The 2016 cycle introduced an explosion of initial coin offerings (ICOs), democratizing access to venture funding. Ordinary individuals could now invest in early-stage projects — an opportunity once reserved for major financial institutions. The market was, however, flooded with tokens backed by little more than white papers. The lack of investor protection and accountability led to the rapid collapse of many ICOs. Most projects from that era are obsolete, with even the largest ICO no longer ranking among the top 100 blockchain projects.

In 2020, three significant trends dominated: DeFi schemes, NFTs, and play-to-earn (P2E) games. DeFi projects promised unsustainable yields — sometimes exceeding 100% — by minting more tokens to provide the yields without any backing economic activity. Similarly, NFTs saw massive valuations, some for mere pixel art that couldn’t hold value. The metaverse hype also fizzled as expectations of mass virtual adoption failed to materialize. P2E games relied on inflationary tokenomics that collapsed when growth stalled, exposing the fragility of these models.

The 2024 post-halving cycle began on solid footing with the approval of US-based Bitcoin ETFs, formally integrating cryptocurrency into traditional financial markets. This move, paired with blockchain communities increasingly influencing democratic processes, marked a significant shift.

For the first time, crypto assets are within financial systems rather than outside, potentially leading to balanced regulation instead of blanket hostility toward the technology. The people intrinsically see its utility and have spoken to it. The US is poised to take a leading role in adopting blockchain technology, which augurs well, especially considering the US role in other prior technological innovations and advancements. The next question: How far will this integration go? Could we see more countries adding crypto assets to national reserves beyond the one or two that already have them? Beyond regulatory progress, several blockchain applications are poised for scrutiny this cycle.

Decentralized real-world assets

Tokenizing real-world assets and decentralizing their financing have gained traction. RWAs allow asset owners to directly benefit from blockchain-based financing. Key sectors include real estate and home financing, stocks, bonds, Treasury bills, agricultural funding, DePIN and DePUT.

Blockchain-AI synergy

AI combined with blockchain is emerging as a powerful force. Decentralized management of AI models and secure data handling offer new solutions, particularly for privacy. AI could outperform solutions like ZK-SNARKs by managing encrypted data, revealing it or proof of data only to its owner, as instructed by its owner, or to authorized law enforcement entities under specified conditions, depending on the blockchain’s constitution.

Microtransactions

Traditional financial systems can’t support microtransactions owing to high operational costs. With low-cost transaction models, blockchains are naturally suited for micropayments, especially for content consumption. This could dismantle outdated bundling practices in media and drive a new era of seamless payments.

Memecoins and celebrity tokens

Memecoins have proliferated, with nearly 10 now in the top 100 by market cap and lacking in virtually any real utility. Lower-cost blockchains and user-friendly token-creation tools fuel this trend. Meme tokens launched by or around popular public figures are also gaining popularity, but most are just as lacking in utility.

Stablecoins

Stablecoins continue to bridge traditional finance and blockchain. With faster, cheaper blockchains dominating this cycle, stablecoins are becoming widely used for payments, challenging legacy systems like slow check clearing and expensive cross-border transfers. Regulatory clarity could push stablecoins toward mainstream adoption.

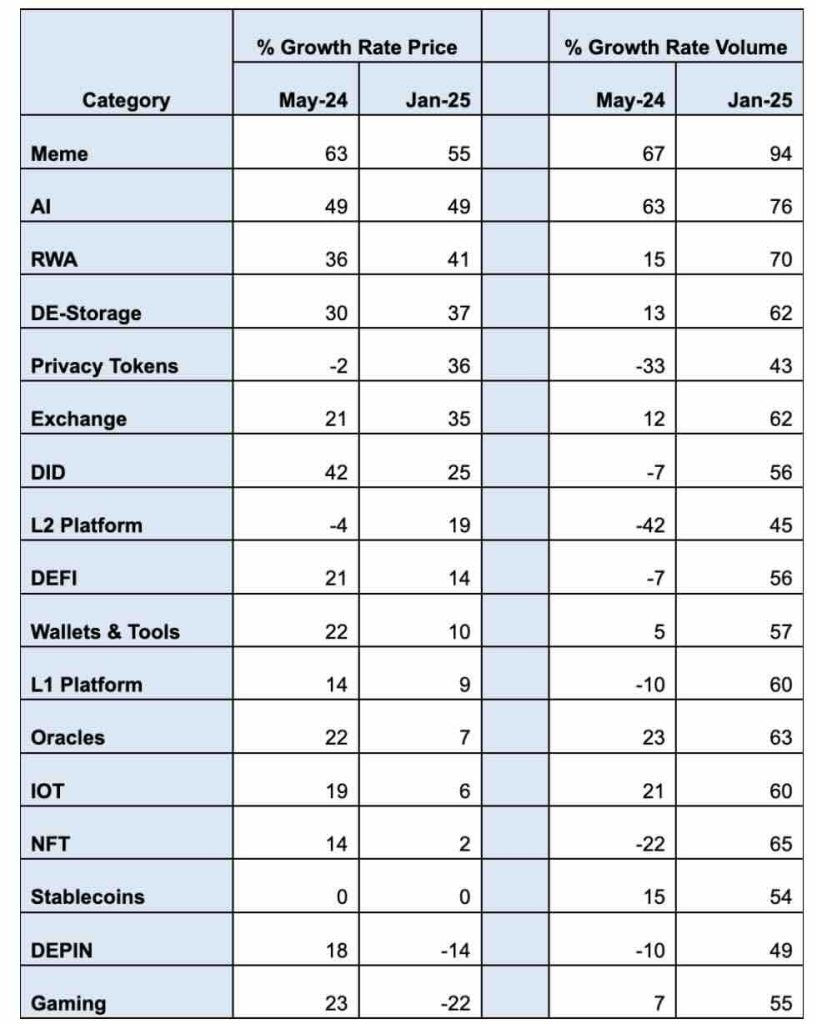

What the early data reveals

Toronet Research tracked token performance across categories from January to May 2024, projecting trends into December. The findings:

The data showed that memecoins, AI-related, and RWA tokens were early growth leaders. Other observations include that all categories showed volume growth, typical during the heightened interest and participation in blockchain projects that seem to occur every four years. DePIN projects might not have experienced much growth to start the cycle, although one or more innovative projects could achieve some breakthroughs. Growth in layer-2 projects is outstripping those of layer-1 projects or absorbing much of the growth that the latter would have experienced. The results for January 2025 are presented in chart form below.

CoinGecko’s2024 Q3 Crypto Industry Reportreviewed trending categories by web traffic with similar findings for the top three categories. An additional observation from the Toronet Research report is that, as we saw in past cycles, application areas with little utility that led the prior cycle’s mania, such as ICOs in 2017 and NFTs in 2021, tend to be repudiated in the next cycle. Developers and industry leaders should endeavor to guide new adopters toward sustainable, utility-driven projects to reduce market volatility and minimize investor disillusionment. This will reduce the intensity of the quadrennial boom-bust cycles and the extent and numbers of those disillusioned, many already lining up to chase memecoins and ultimately worthless airdrops into futility.

Will we break the cycle?

The ongoing cycle offers blockchain its most significant opportunity yet to deliver lasting impact. The industry is poised for meaningful growth with increasing institutional integration, the promise of more thoughtful regulations and a shift toward real-world utility. The increasing acceptance and integration of blockchain solutions within the broader economy and the potential for thoughtful incoming regulations will likely deliver a much better outcome this cycle than previous ones.

Opinion by: Ken Alabi

This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts, and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Jack Butcher’s no fan of NFT royalties: ‘You’re getting paid on churn’ — NFT Creator

Jack Butcher — creator of meme culture NFT collection Opepen which has seen $240 million in volume — has an unexpected take on NFT royalties.

Read more

Microsoft set to vote on Bitcoin, Peter Todd hiding, and more: Hodler’s Digest, Oct. 20 – 26

Microsoft shareholders are set to vote on whether it should add Bitcoin to the balance sheet, Peter Todd is hiding in fear: Hodlers Digest.

Read moreBitcoin to suffer if it can’t catch gold, XRP bulls back in the fight: Trade Secrets