Ever since Robinhood co-founder Vlad Tenev bounded onto the stage in Cannes two weeks ago, channeling old-time movie star David Niven in his white suit and cravat, everybody’s been talking about tokenized stocks.

It certainly seems like a big deal for mainstream adoption of crypto. Robinhood is a TradFi equities platform with 26 million retail customers tokenizing stocks on Arbitrum and offering them to EU users through its user-friendly app interface.

There are no crypto wallets or seed phrases required — and Tenev suggests it’s a test run for a wider integration of crypto, a demonstration of “what Robinhood itself could look like, built entirely on blockchain technology.”

That same week, Gemini launched its own tokenized stocks on Arbitrum in the EU, and 60 of Backed’s xStocks went live on Solana, supported by Kraken, Bybit, Bitrue and Gate.io.

Tokenized stocks may be just months away from launching in the US too, after dShares issuer Dinari was awarded a broker-dealer license and Ondo Finance acquired Oasis Pro to make use of its licenses.

Coinbase has wanted to launch tokenized equities in the US since 2018 and is reportedly seeking the Securities and Exchange Commission’s permission to finally do so. Chief law officer Paul Grewal called tokenized equities “the future of finance, and a huge priority” for the company.

But this isn’t the first time tokenized equities have been attempted, and the playing field is littered with the bodies of issuers from the last cycle.

And while tokenization brings many advantages, there are considerable downsides to the models Robinhood and Kraken use to tokenize stocks. Here are the pros and cons of tokenized equities in 2025.

Con: Tokenized stocks are not really stocks at all

Critics argue that the tokenized equity offered by xStocks and Robinhood is just a synthetic representation of a share held in a vault somewhere and does not confer any shareholder rights and protections that come with real ownership.

In Robinhood’s case, the tokenized stocks are considered derivatives under EU regulations, even if the model uses licensed US broker-dealers who issue tokenized stocks and custody the underlying assets. Tenev calls it “a derivative that’s backed by the real share.”

Backed’s xStocks tokens are also backed 1:1 by a Special Purpose Vehicle in Liechtenstein. Even if Kraken or Bybit collapses, the underlying assets theoretically remain safe. The token can be redeemed for the offchain price when the market opens.

Alan Keegan, the DeFi portfolio manager at M31 Capital, says this is halfway to the goal. “We’ve solved the issue of issuing a claim for an offchain asset onchain, via tokenizations,” but adds that there’s still a long way to go.

“There are regulatory questions and legal infrastructure to be built to get to a place where an onchain transaction of a security actually represents a transfer of that security,” he says.

“Building the infrastructure to solve that problem requires a great degree of legal know-how, traditional finance know-how, blockchain sophistication, and (speaking frankly) money to spend.”

The closest example to date is Securitize’s Exodus token on Algorand, which represents direct legal ownership of the security on Securitize’s shareholder registry

“It’s going to take time, but native tokenization is the necessary first step,” Securitize CEO Carlos Domingo tells Magazine.

“You can’t decentralize stock ownership unless the stock is represented onchain in a compliant, legally valid way. Securitize is one of the only platforms in the US that can do this today.”

Neutral: Tokenized stocks are in a legal gray area

Tokenized stocks operate in a legal gray area, with Robinhood and xStocks pushing the envelope in a similar way to how Uber did with its ridesharing app a few years ago.

Robinhood’s tokenized stocks are only available in the EU for now, but as it’s a listed company working with a US-listed broker-dealer to offer US securities, US regulators could decide to shut it down.

The Securities Industry and Financial Markets Association (SIFMA) has already urged the SEC to reject trading models that fall outside the Regulation National Market System for equities.

However, new SEC chair Paul Atkins has expressed in-principle support. “Tokenization is an innovation. And we at the SEC should be focused on how we advance innovation in the marketplace,” Atkins told CNBC.

JUST IN: ?? SEC Chair Paul Atkins says "tokenization is an innovation" and the agency is committed to advancing it. pic.twitter.com/lcuq7X2oIb

— Fiat Archive (@fiatarchive) July 2, 2025

OpenAI has also highlighted legal issues with Robinhood selling tokens tied to its private stock, noting the company needs to approve any transfer and has not done so. The Bank of Lithuania subsequently opened an investigation.

Rob Hadick, general partner at Dragonfly, said on X that the risk for tokenholders is that private companies end up “just cancelling equity sales altogether for those who violate their shareholder agreements.”

But for every SpaceX or OpenAI that isn’t keen on the tokenization of its private shares, there are many more who see it as a big opportunity, according to Tenev.

“Lots of private companies have been reaching out to me and asking… when can we get our own private stock tokenized?” he told podcaster Camila Russo recently.

The bigger legal issue around selling tokenized private stock to the public is that it essentially does an end run around the disclosure and transparency rules governing publicly listed companies.

If companies can sell private stock and raise funds without having to go through the expense and compliance requirements of an initial public offering, why would anyone go public?

Pro: 24-hour a day trading for tokenized equity and use in DeFi

Traditional markets are closed for around 81% of the hours in a given year, meaning tokenized stocks that trade around the clock will have a big advantage.

xStocks and Robinhood’s tokenized equity are initially available 24/5, but Tenev says that will be changing soon.

“Where it starts to get really interesting is when we start plugging it into Bitstamp, which is when 24/7 trading becomes possible. And at that point, the stock tokens start to behave like other cryptos, Bitcoin and Ethereum,” Tenev said. The next phase will be to integrate the assets in DeFi.

“So you could imagine swapping collateralized lending and borrowing and really self-custody, which I think would be very powerful for stocks because it would untether your stock tokens from any individual brokerage or crypto provider.”

Keegan agrees that 24-hour a day functionality, lower costs, more reliable execution and faster settlements are big advantages, along with the potential for composability in the DeFi ecosystem.

Pro: Blockchain platforms may outcompete TradFi platforms

Galaxy Digital’s analysis argues that 24/7 trading of tokenized equity on Bitstamp is a big threat to traditional markets like the New York Stock Exchange:

“This directly challenges the deep concentration of liquidity and activity that gives major TradFi exchanges (e.g. NYSE) their competitive advantage […] more brokerages adopting a blockchain-based strategy for trading could put immense pressure on traditional exchanges.”

But Securitze’s Domingo argues there’s a way to go yet.

“To reach a point where entire markets operate 24/7 on crypto rails, we need three things,” says Domingo.

“Regulatory clarity that enables onchain trading venues to exist under a modified framework. Liquidity and infrastructure — market makers, secondary markets and settlement systems — that function reliably outside of traditional hours [and] institutional trust and adoption.”

TradFi isn’t going quietly either, with traditional markets already offering pre- and after-market trading that helps cover about 16 hours of the day.

The New York Stock Exchange’s electronic Arca exchange also in February received approval to offer trading 22 hours a day, five days a week, with the extended trading expected to kick off this year.

Con: After-hours volatility of tokenized stocks

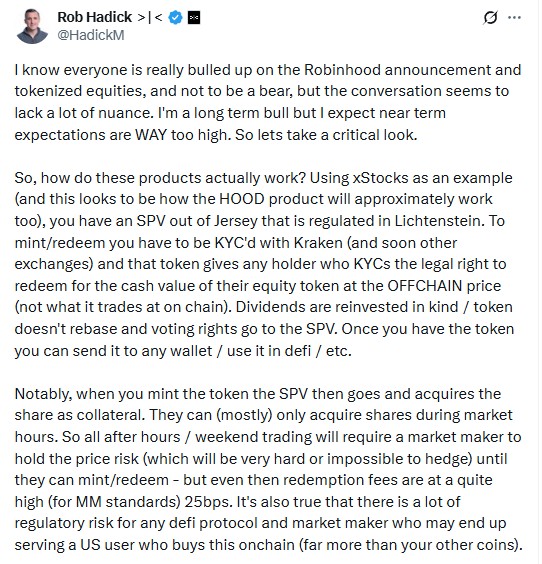

Hadick from Dragonfly points out that trading outside of market hours may create a plethora of issues.

Using xStocks as an example, he says that when investors buy a token after hours, the SPV has to acquire that stock when the market opens, exposing the market maker to pricing risks.

This will mean higher spreads, and market makers may end up pulling liquidity entirely during times of market stress. “Which, if these things permeate DeFi lending and [derivatives], will create major cascading liquidation risk,” he says.

He also notes the token only entitles the holder to the offchain price, meaning stocks may rapidly return to that price when markets open.

“That means when people buy in times of that low liquidity euphoria on weekends/after hours, but the equities market then opens lower than token buyers expected, you will see quick, rapid losses at open, which will primarily be borne by retail,” says Hadick.

“Functionally, that means these are just not good products […] They cannot serve a sophisticated, real, and global equities market. And they likely won’t even serve the needs of the professional crypto traders who know they can get significantly better pricing and less risk elsewhere.”

Con: Fragmented liquidity accompanies stock tokenization

Having multiple issuers tokenize stocks will also fragment liquidity. Imagine a future where you have to choose between “rTSLA, cTSLA, sTSLA, xyzTSLA, ethTSLA, solTSLA or hyperTSLA,” as crypto VX Mike Dudas joked.

Johann Kerbrat, Robinhood’s crypto chief, concedes that it will be a problem.

“I hate the idea of having a Tesla-Kraken token and a Tesla-Robinhood token,” he said. “Instead of actually moving forward and creating a better financial system, we’re splitting [up] liquidity.”

Domingo wryly asked on X, “Isn’t that exactly what Robinhood is doing?” Having multiple tokenized stock issuers also greatly increases the chance that one of the issuers will blow up somehow, leading to tokenholders being left out of pocket.

Con: Tokenized stocks failed in 2021

Last cycle, Synthetix offered synthetic tokens offering price exposure to stocks such as Tesla in 2021. sTSLA saw a grand total of just 798 transactions before being phased out that same year.

Low liquidity played a part, but it’s also possible that DeFi degens preferred to speculate on altcoins with a potential 10X upside, rather than a stock that might move a few percent in a month.

Mirror offered synthetic stocks too, but collapsed alongside Terra. Binance also offered stock tokens for a few months in 2021 before delisting them following regulatory pushback in the UK and Germany.

The most “successful” issuer last cycle was FTX, which offered tokenized stocks with 1:1 backing via CM Equity. It peaked at almost $1 billion in volume in October 2021. But after FTX collapsed the following year, it emerged that CM Equity had withdrawn from the agreement in December 2021, casting doubt on the backing of the tokens. Tokenized stockholders lost their funds in the collapse.

There is one survivor from those dark days, however. Securitize tokenized the shares of wallet provider Exodus in 2021, and with a market cap of $294.7 million, it accounts for 78% of today’s entire tokenized equity market by itself.

Domingo points out it’s not 2021 anymore, with a favorable regulatory environment and the involvement of asset managers like BlackRock, Apollo and Hamilton Lane. “The credibility that top-tier asset issuers provide is now expanding from tokenized treasuries and private credit to other assets such as tokenized equities,” he says.

How will tokenized stocks affect crypto prices?

As the chain with the largest amount of stablecoins and RWAs, Ethereum stands to benefit from the wider adoption of tokenized shares. Robinhood’s choice of Ethereum L2 Arbitrum was seen as a huge vote of confidence in the ecosystem and L2 roadmap.

Keegan says financial institutions can tailor-make L2s to comply with KYC and privacy requirements, along with transaction rollbacks.

“The most exciting feature of the L2 scaling infrastructure is that L2s can inherit the decentralization and credible neutrality guarantees of Ethereum while also being built to suit the needs of a specific use case (including regulatory compliance).”

Since the announcement, Ethereum’s price has increased by a quarter. Solana has also demonstrated over the past two years that it’s very popular with retail traders, so it also stands to benefit from the wider adoption of xStocks.

Some argue that tokenized stocks will compete for the same capital that is currently being spread among altcoins. But Domingo argues that a halo effect is more likely.

“We don’t view tokenized stocks and altcoins as necessarily competing for capital. Instead, we are seeing traditional financial institutions embracing blockchain infrastructure, utilizing the same rails that power DeFi. That’s undeniably bullish for staying power and expansion of the broader crypto ecosystem.”

Andrew Fenton

Web3 games shuttered, Axie Infinity founder warns more will ‘die’: Web3 Gamer