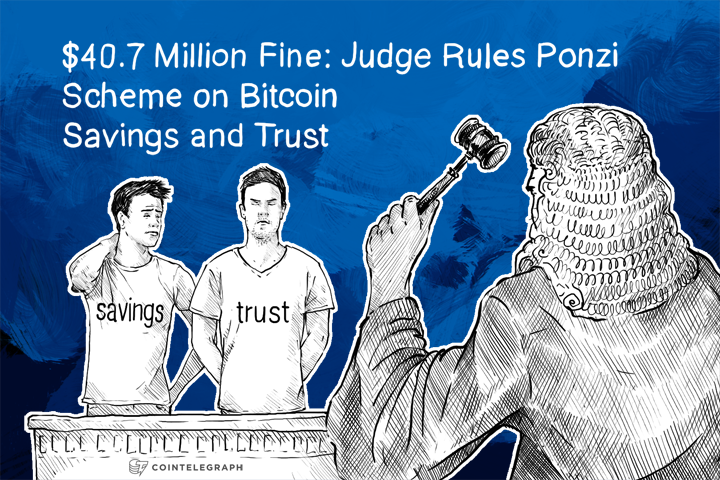

$40.7 Million Fine: Judge Rules Ponzi Scheme on Bitcoin Savings and Trust

Latest NewsPublishedSep 22, 2014

A US Federal Judge has ruled in case is SEC v. Shavers et al, U.S. District Court, Eastern District of Texas, No. 13-00416 that the Bitcoin Savings and Trust was indeed a criminal enterprise and Shavers was guilty of running a Ponzi Scheme.

There are several high profile criminal and civil cases involving Bitcoin in the United States. In some of these the prosecution is clearly applying law to Bitcoin transactions that might not apply. But in the case of Trenton Shavers and his Bitcoin Savings and Trust this turned out not to be the case, even though his attorneys tried to make it look like it.

A US Federal Judge has ruled in case is SEC v. Shavers et al, U.S. District Court, Eastern District of Texas, No. 13-00416 that the Bitcoin Savings and Trust was indeed a criminal enterprise and Shavers was guilty of running a Ponzi Scheme.

US Magistrate Judge Amos Mazzant ruled that Shavers had “knowingly and intentionally” ran his business “as a sham and a Ponzi Scheme.” The ruling included an order for Bitcoin Savings and Trust and its owner, Trenton Shavers, to pay a total of US$40.7 million. The judge ruled that the SEC had presented sufficient evidence that his virtual currency investments were a complete scam.

The decision was rendered on Thursday and Shavers or his attorney have so far declined to comment on either the decision or on Shavers ability to pay the judgment. Trenton Shavers is also involved in a civil case surrounding the same issue and his attorney withdrew from the case.

While using the name “pirateat40” Shavers was able to trick his victims into giving him more than 720,000 Bitcoins over a several month period by convincing that his investment skills allowed him to earn them up to 7% weekly interest on their investments. The problem was that Shavers was investing none of the coins. Instead he was using new investments to pay off older investors who were expecting returns. He also diverted significant amounts into his personal accounts, using the funds for things like shopping and casino vacations.

Shavers’ attorney filed a motion to dismiss citing that because the Internal Revenue Service ruled that Bitcoin was a commodity, he could not be charged with a Ponzi scheme due to the wording of the statute. The Judge disagreed however, and ruled that the IRS’s position was only for tax purposes and suggested that because Bitcoin could be used for purchases of goods and services, then it qualified to be under the definition of money in this case.

The judge, whose bench is in Sherman, Texas put the collective losses of victims at 265,675 bitcoins, which totals nearly US$150 million and along with liabilities that he was ordered to return, Shavers was also fined US$150,000. He will have an opportunity to appeal first to the District Judge and then to the Fifth Circuit in New Orleans.

But since his only real defense was the technical point about Bitcoin’s definition as money, a successful appeal in one of the most conservative circuits in the United States is unlikely.

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.