It is the dream for many people to trade in a decentralized way on the chain. After countless experiments, we found that the automatic market maker (AMM) model solved the problem of extremely high matching costs for on-chain aggregation. However, an AMM also has a problem, that is, it has not solved the asset pricing problem of the liquidity provider. Therefore, with a new generation of decentralized exchange based on the equilibrium pricing model (EPM), CoFiX was born.

What is the core ideology of the EPM?

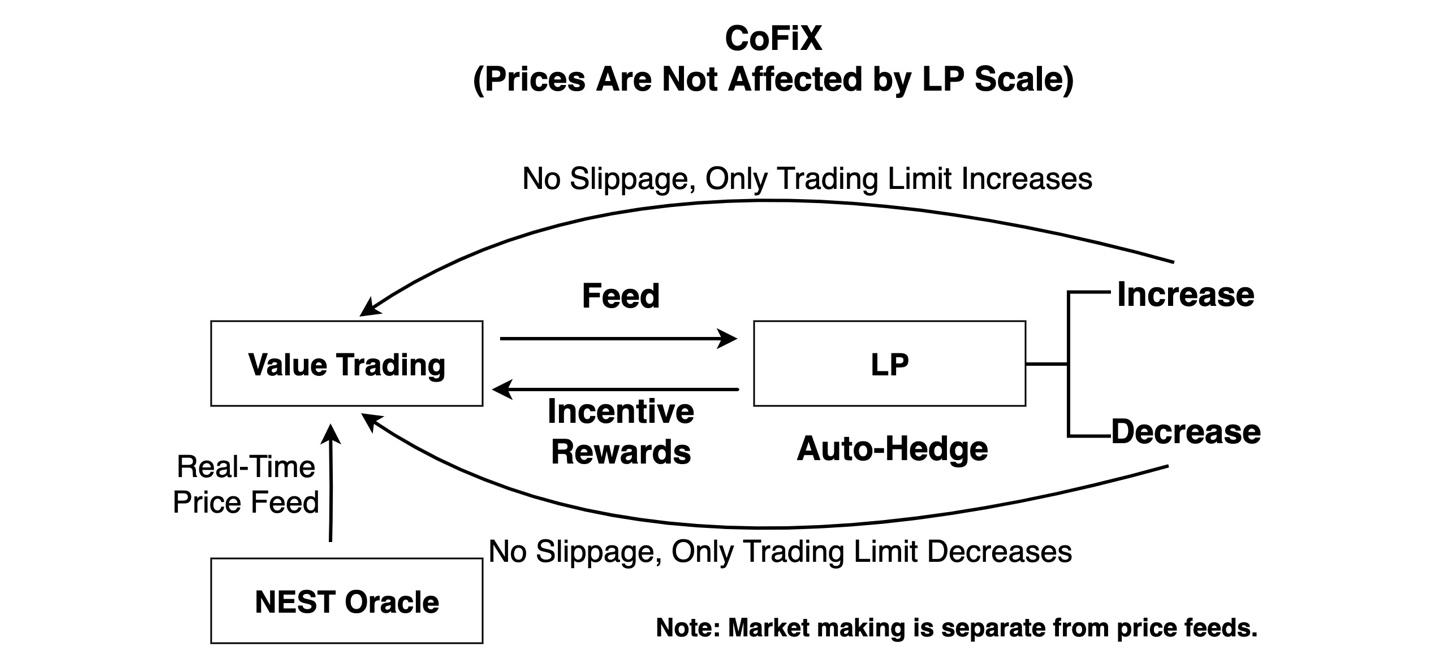

Unlike an AMM, the EPM uses real-time market prices when trading, and at the same time, pricing and trading are separated. In traditional exchanges, pricing and trading are always together, but they do not function and cost the same. The infrastructure required for pricing is much higher than that of trading, which is difficult on the chain. The EPM is based on oracle pricing which uses COFiX for trading, and this separation makes trading purer.

It is clear that the current pricing model used by an AMM is far less efficient and secure (for the seller) than aggregated transactions. Considering the particularity of the chain and transaction costs, it is still acceptable but the pricing cost (forced to accept arbitrage to modify the price) is much higher than the EPM, which only requires targeted compensation for each transaction.

Computability

According to the analysis above, the EPM-based DEX design invokes on-chain risk compensation at the very beginning. This creation is made possible thanks to the computability of the price. Credit risk cannot be computed if only a centralized price is invoked, so it must be a fully decentralized oracle to provide a computable sequence of prices.

Equilibrium deviation

A stable AMM requires an equilibrium between value traders, arbitrageurs and LPs, where the fees contributed by value traders need to cover the arbitrageurs’ returns and the LPs’ cost of capital. This leads to a situation where with fewer actual traders, the actual fee return is lesser and a larger number of arbitrage returns need to be made up. This leads to the LPs’ withdrawal from the pool, reinforcing the disadvantage of price slippage and further underpinning the value trading volume, trapping it in a negative cycle until the entire trading system collapses.

In contrast, the CoFiX equilibrium based on the EPM is more straightforward. There is a commission if there is a transaction, and there is no commission if there is no transaction. No matter the size of the fund pool, there will be no price slippage, which is the same as buying in the market. Therefore, it does not cause a negative cycle but is stable at some reasonable trade size. It can be said that an AMM is an unstable equilibrium and CoFiX can form a stable equilibrium.

Automatic hedging design

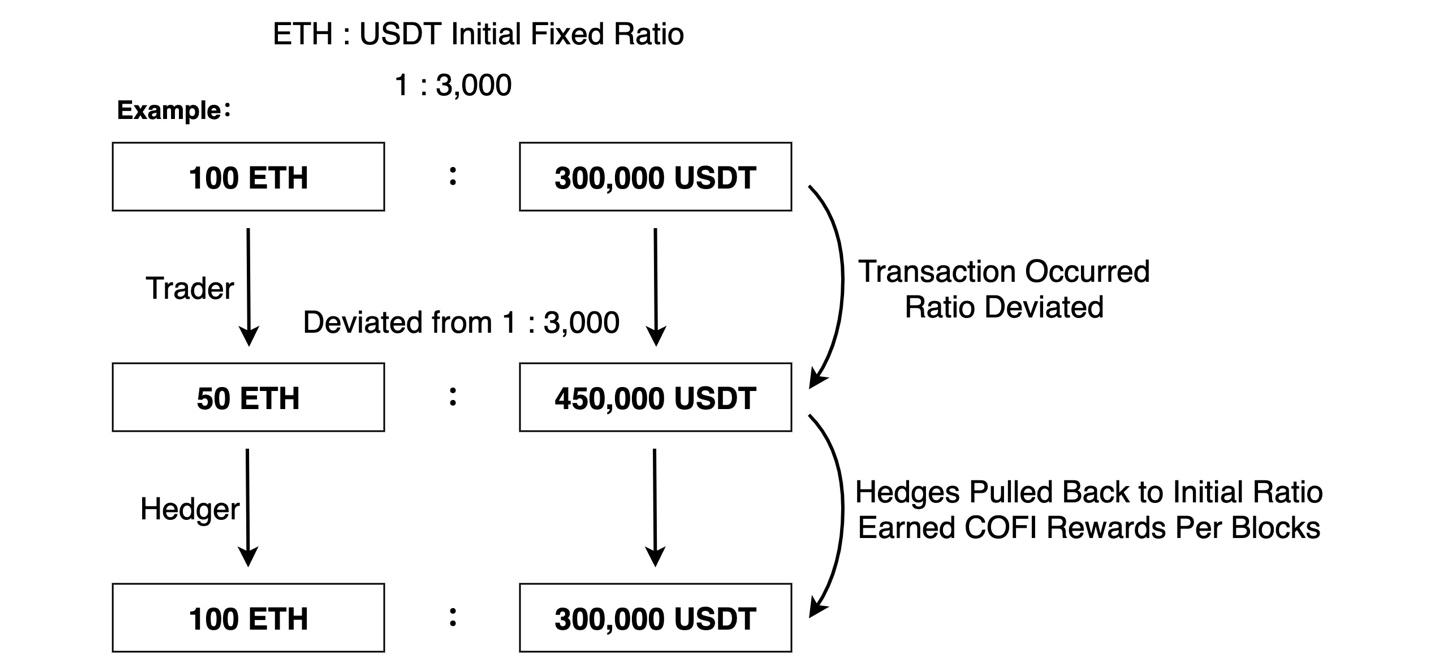

CoFiX has a creative automatic hedging design, that is, keeping the initial asset ratio unchanged. Once the trader deviates, the automatic hedging traders will trade back for CoFiX (COFI) token incentives. The LP collectively pays a portion of the return to the hedgers and does not have to do so themselves.

The main idea of auto-hedging is that if the initial ratio is broken, the system generates COFI rewards. Automatic hedging traders make decisions based on the COFI value and transaction costs of the mine. The former will complete the hedging transaction when the cost of the latter is covered. Since COFI is mined according to blocks, the deviation will always be traded back.

CoFiX’s net worth performance

Since the launch of CoFiX 2.0, the net worth data has remained relatively stable, which means that hedging is relatively effective even after considering extreme price volatility and the arbitrageurs’ interaction. Even though CoFiX’s LP net worth changes within 4%, its APY stays above 150% and the LP market-making returns can be precisely calculated.

Future development

A simpler automatic hedging mechanism than quoting oracles for pricing is to trade stablecoins. There is no need to make a detailed distinction between the prices of stablecoins as the default is a one-to-one ratio. However, the difference in price can be compensated by the mining returns of the stable pool’s funders with a higher value compensation (although the deviation is minimal). The automatic hedge is mined based on the LP’s share, guiding the hedger through balancing transactions. This model will be available in the upcoming version of CoFiX 2.1 and will be especially effective when the stablecoin and parallel asset Parasset are integrated.

As a result of the invention of automatic hedging, CoFiX could also enable another model in the future, automatic asset management, through a gaming structure that allows LPs to achieve a target risk-return (unlike Yearn.finance’s YFI liquidity mining, which cannot set a specified target return) without having to perform any operations. This direction will be the key to explore in CoFiX 3.0.