Betting on turmoil: Deribit launches Bitcoin volatility futures

Latest NewsPublishedMar 17, 2023

Volatility products are popular with traditional investors, as they enable portfolio hedging, risk management and speculation.

Crypto derivatives exchange Deribit will soon launch Bitcoin (BTC) volatility futures, giving investors a direct way to measure and trade BTC market volatility.

On March 17, Deribit introduced BTC DVOL futures — a derivatives contract built on the Deribit Bitcoin Volatility Index, which measures the implied volatility of the largest cryptocurrency. Deribit’s volatility gauge provides a 30-day outlook on investors’ expectations for annualized volatility.

Like other volatility products, BTC DVOL can potentially help traders with risk management, portfolio hedging or market speculation.

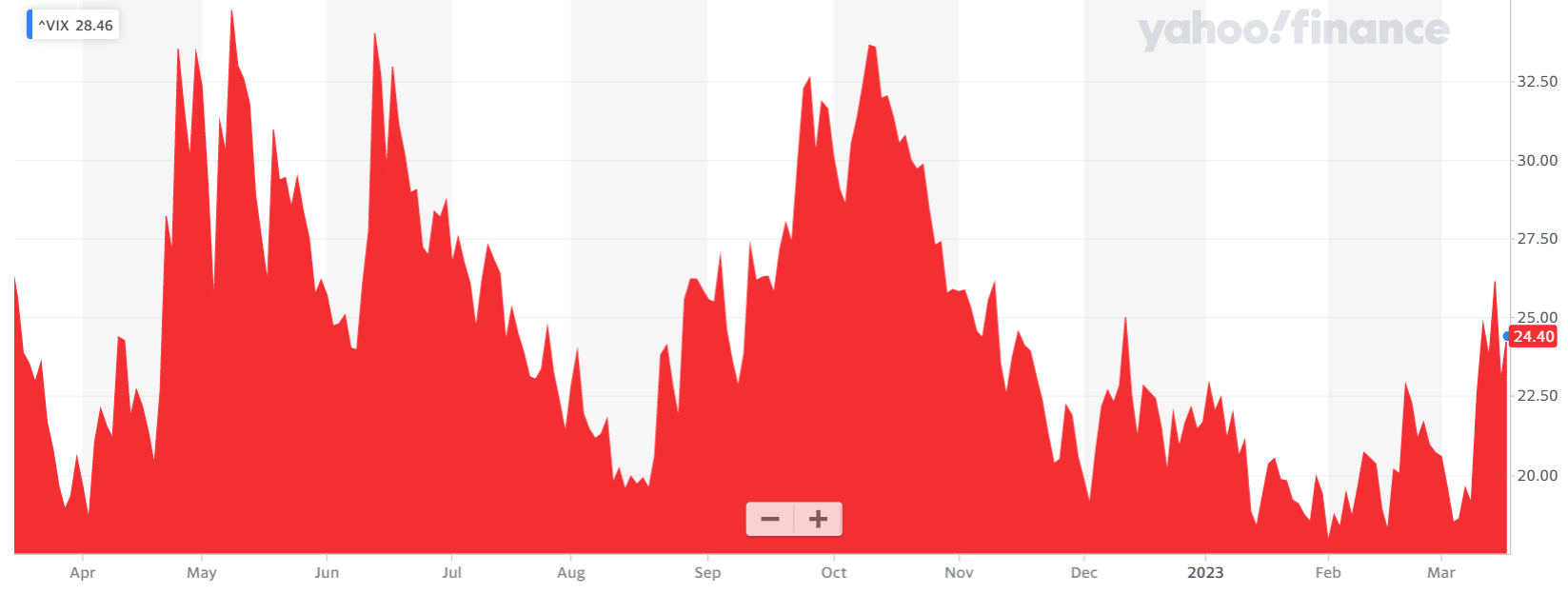

Volatility-as-an-asset is widely traded in traditional finance, with the most popular product being the Chicago Board Options Exchange Volatility Index, also known as VIX. On the VIX scale, a reading of around 20 represents the historical average. Readings below that level signal lower implied volatility than the historical mean. Readings above 20 are usually associated with more turbulent financial conditions, while anything above 30 signals significant market volatility, usually due to uncertainty, risk or investor fear.

VIX measures the volatility of S&P 500 index options, a leading indicator of the U.S. stock market.

Traditional markets have battled extreme volatility over the past 12 months, marked by major fluctuations in the S&P 500 index and broader stock market. Source: Yahoo Finance

Bitcoin and the broader crypto markets have exhibited extreme volatility over the past 12 months. The period known as crypto winter is usually associated with deep corrections in digital asset prices following an over-extended bullish phase.

Related: Crypto acted as safe haven amid SVB and Signature bank run: Cathie Wood

Although crypto investment products experienced record outflows last week following the collapse of Silicon Valley Bank and Signature Bank, regulatory clarity on investor deposits has helped Bitcoin stage a large relief rally. Bitcoin’s price crossed $27,000 on March 17 for the first time in over nine months.

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.

More on the subject