UK blockchain carbon offset platform raises $45M in seed funding

Latest NewsPublishedFeb 8, 2023

Carbonplace says it will use the funds to scale its services and become the “SWIFT of carbon markets.”

According to a press release published on Feb. 8, blockchain carbon credit transaction network Carbonplace has secured $45 million in an investment round from its nine founder banks with a combined $9 trillion in assets under management. The banks are BBVA, BNP Paribas, CIBC, Itaú Unibanco, National Australia Bank, NatWest, Standard Chartered, SMBC and UBS. The London-based fintech company has also announced that it will become an independent entity, led by new CEO Scott Eaton.

As told by Carbonplace, the company will use the investment to strengthen its platform and workforce, allowing it to scale its services to a larger client base of financial institutions and seek partnerships with other carbon market players, such as registries and stock exchanges around the world. Carbonplace has been described as the “SWIFT [Society for Worldwide Interbank Financial Telecommunications] of carbon markets” that will allow participants to share carbon data in real-time, ensuring a secure and traceable settlement of transactions.

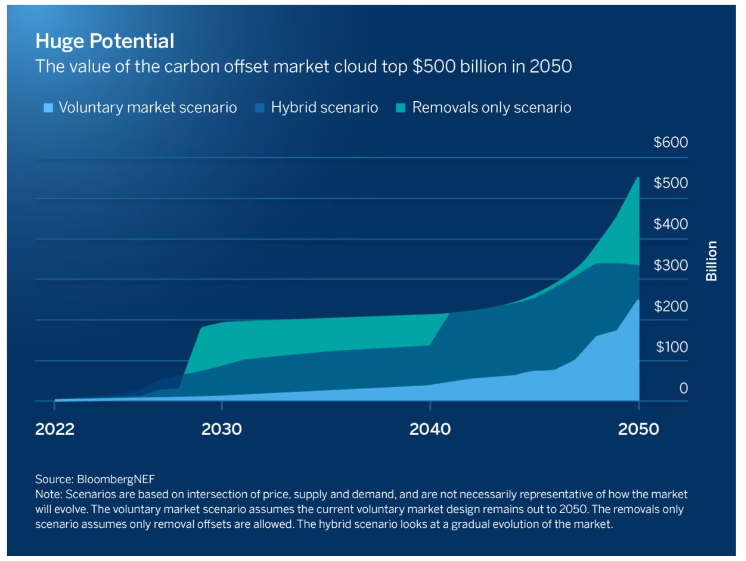

Commenting on the development, Robert Begbie, CEO of NatWest Markets, cited data from McKinsey showing that “global demand for voluntary carbon credits is likely to increase by a factor of 15 in the next several years.” He said Carbonplace is uniquely positioned to meet that demand by providing scalable technology to environmentally conscious businesses.

While the service is expected to launch later this year, Carbonplace has already piloted trades with companies such as Visa and Climate Impact X. Carbonplace uses its own distributed ledger technology to facilitate offset transactions and has hailed digital wallets as a tool to “enable owners to reliably demonstrate ownership to the market, reducing the risks of double counting and simplifying reporting.”

Projections of the global carbon offset market. Source: BBVA, BloombergNEF

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.

More on the subject