Sun Sets on Offshore Banking as Assets Worth $11 Trillion Uncovered

Latest NewsPublishedJul 2, 2020

The three-year old Common Reporting Standard is uncovering offshore assets on a massive scale, highlighting cryptocurrencies as a potential alternative.

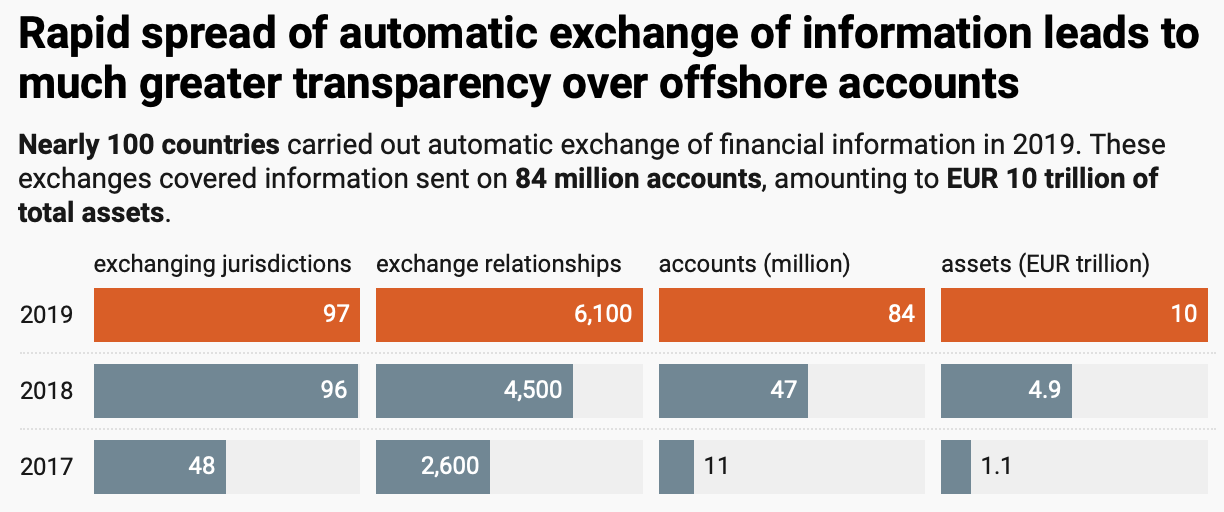

The Organization for Economic Cooperation and Development, or OECD, reported on Tuesday how automatic reporting in 2019 helped uncover $11 trillion worth of assets in offshore accounts.

The result came as the Common Reporting Standard, or CRS, entered its third year of operation since its launch in 2017.

Unlike many previous iterations of international tax reporting standards, the CRS requires countries to automatically report activity in accounts held by foreign nationals to their respective country of origin. This solves issues deriving from request-based information sharing, which required active suspicion and investigation from the originating country.

This is supported by over 100 countries across the globe, which seek to curtail tax evasion enabled by offshore bank accounts and regulatory arbitrage. Notably, the standard was adopted in 2017 by popular offshore destinations like the Cayman Islands, Seychelles and many others.

Since the introduction of CRS in 2017, the amount of assets that fell under scrutiny increased almost tenfold from $1.2 trillion. The OECD explained that the growth is largely attributable to more countries joining the system, as well as a wider scope of reported information.

Source: OECD report

The organization also discovered in November 2019 that between 2008 and 2019, deposits to foreign-owned accounts decreased by 24%, or $410 billion.

Crypto to take over?

The anonymous and decentralized nature of cryptocurrency can be helpful in filling the void left by traditional offshore banking.

This is why tax agencies across the world are beginning to clamp down on potential evasion routes using cryptocurrency, with the IRS including targeted questions related to digital assets in a 2019 tax filing draft.

The U.K.’s tax agency similarly began preparations as it signaled intentions to use blockchain tracking software in January 2020.

As demonstrated quite often, generic blockchains like Bitcoin and Ethereum are not anonymous and can be tracked quite easily. But even blockchain’s relative transparency still returns authorities to pre-CRS investigation methods, which require active suspicion.

While privacy solutions can make cryptocurrencies exponentially harder to track, their volatility makes them a tough sell as practical store of value assets — legal or not.

Stablecoins can fix the volatility issues, but centralized iterations like Tether and USDC have inbuilt freezing mechanisms that can be used for compliance purposes. Decentralized stablecoins, on the other hand, pose unknown technical risks.

Cryptocurrencies may step in to fill offshore banking’s shoes, but mass adoption may not quite be there yet.

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.