Northern Marianas vetoes bill for Tinian to launch its own USD stablecoin

Latest NewsPublishedApr 15, 2025

Northern Mariana Islands Governor Arnold Palacios has vetoed a bill that would have allowed a local government in the US territory to launch its own stablecoin.

Update (April 15, 10:47 am UTC): This article has been updated with comments from Marianas Rai Corp. co-founder Vin Armani.

The governor of the Northern Mariana Islands, a small Pacific US territory just north of Guam, has killed the legislation that would have allowed one of the territory’s local governments to launch a fully backed US dollar-pegged stablecoin.

In an April 11 letter seen by Cointelegraph, Northern Mariana Islands Governor Arnold Palacios said he vetoed the bill as it “presents several legal issues and may be unconstitutional.”

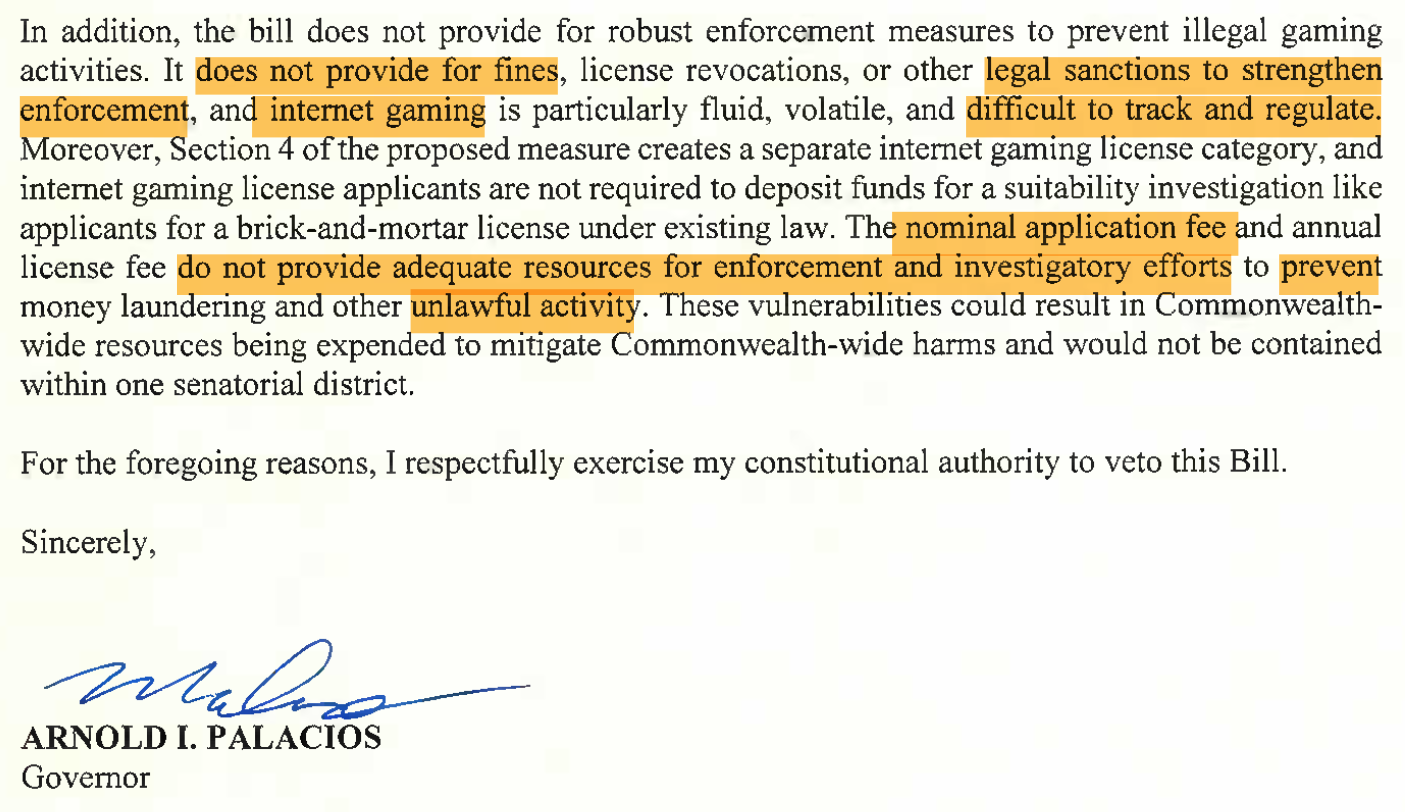

Palacios’ letter said the bill, which largely dealt with issuing licenses to internet casinos, would regulate an activity that could not “be clearly restricted” to Tinian, a small island forming part of the territory that was hoping to launch a stablecoin.

Tinian, which has just over 2,000 residents and a largely tourism-based economy, is governed by the local government, the Municipality of Tinian and Aguiguan, one of four municipalities in the Commonwealth of the Northern Mariana Islands.

In February, Republican Northern Marianas Senator Jude Hofschneider led the introduction of the bill to amend a local Tinian law to allow internet-only casino licenses, which tacked on a provision allowing the Tinian treasurer to issue, manage and redeem a “Tinian Stable Token.”

The four-member Tinian delegation to the Marianas legislature passed the bill in a unanimous vote on March 12.

In vetoing the bill, Palacios didn’t comment on the proposed stablecoin, instead taking issue with its aim to police an industry that can cross jurisdictional boundaries, and said the measure lacked “robust enforcement measures to prevent illegal gaming activities.”

A highlighted excerpt of Governer Palacios’ letter noting his reasons for vetoing the stablecoin and internet gambling bill Source: Northern Mariana Islands Governor’s Office

The stablecoin, called the Marianas US Dollar (MUSD), was to be fully backed by cash and US Treasury bills held in reserve by the Tinian Municipal Treasury, according to statements shared with Cointelegraph last month.

The Tinian government chose tech services firm Marianas Rai Corporation, based in the Commonwealth’s capital of Saipan, to exclusively provide the infrastructure to issue and redeem MUSD and develop its ecosystem.

Marianas Rai Corp. co-founder and technology chief Vin Armani told Cointelegraph that the company doesn’t see a chance for a stablecoin bill to pass on its own and added that “the legal opinions noted are deeply flawed and do not reflect the actual contents of the bill.”

“It is unfortunate, at a time when our Commonwealth is severely struggling financially due to decades of decline in and dependency on tourism, that this opportunity to launch the first fully-reserved, fiat-backed stable token issued by a public entity in the United States has not been achieved for the people of the Commonwealth,” he added.

Tinian misses chance at beating Wyoming

The bill’s passage could have seen Tinian’s government be the first US government entity to issue a stablecoin ahead of Wyoming, whose Governor Mark Gordon said in March that the state’s stablecoin could be ready for a launch in July.

Armani said the bill “would have been an incredible accomplishment for a small self-funded company based in a small island nation in the middle of the Pacific, beating Wyoming to the finish line, given the resources [the state has] invested.”

Related: The GENIUS stablecoin bill is a CBDC trojan horse — DeFi exec

He said Marianas Rai Corp. fully owns the technology behind MUSD, which is built on the eCash blockchain, a network that rebranded from Bitcoin Cash ABC in 2021 and is a fork of Bitcoin Cash — a blockchain that split off from Bitcoin in 2017.

Armani added that the company was “in active discussions with potential partners” about launching the token and was “poised to act quickly” as US Congress is looking to pass stablecoin laws.

The Senate Banking Committee passed the stablecoin-regulating Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act in mid-March, while the US House Financial Services Committee passed the Stablecoin Transparency and Accountability for a Better Ledger Economy (STABLE) Act in early April.

Magazine: Elon Musk’s plan to run government on blockchain faces uphill battle

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.