Turkey to empower watchdog to freeze crypto accounts in AML crackdown: Report

Latest NewsPublishedSep 29, 2025

Turkey plans new legislation letting Masak freeze crypto accounts to fight money laundering, aligning with FATF standards.

The Turkish government is reportedly preparing legislation that would grant its financial crime watchdog, Masak, the authority to freeze cryptocurrency accounts as part of a wider effort to combat money laundering and financial crime — a move that potentially highlights regulators’ ongoing concerns over crypto-related illicit activity.

According to a report by Bloomberg, citing people familiar with the matter, the proposed changes would expand Masak’s Anti-Money Laundering (AML) mandate, enabling it to freeze both cryptocurrency and traditional bank accounts.

The measures are said to align with recommendations from the Financial Action Task Force (FATF), which is an intergovernmental body that sets global standards for combating money laundering and terrorist financing.

The bill is expected to be introduced in the Grand National Assembly, though no timetable was provided, according to Bloomberg.

Source: Bloomberg

If passed, Masak would be empowered to freeze or close accounts suspected of illicit use across payment systems, electronic money institutions, banks and cryptocurrency exchanges. It would also be able to impose transaction limits or blacklist crypto wallets linked to criminal activity.

A key focus of the legislation is to curb the rise of so-called “rented accounts” — accounts that criminals pay individuals to use for activities such as illegal gambling or financial fraud.

Although cryptocurrency trading and investment remain legal in Turkey, and profits are not yet subject to taxation as of October, the government has been moving to tighten oversight.

As Cointelegraph reported, the Finance Ministry is preparing new rules that would require crypto exchanges to collect detailed information on the source and purpose of transactions, as well as introduce limits on stablecoin transfers.

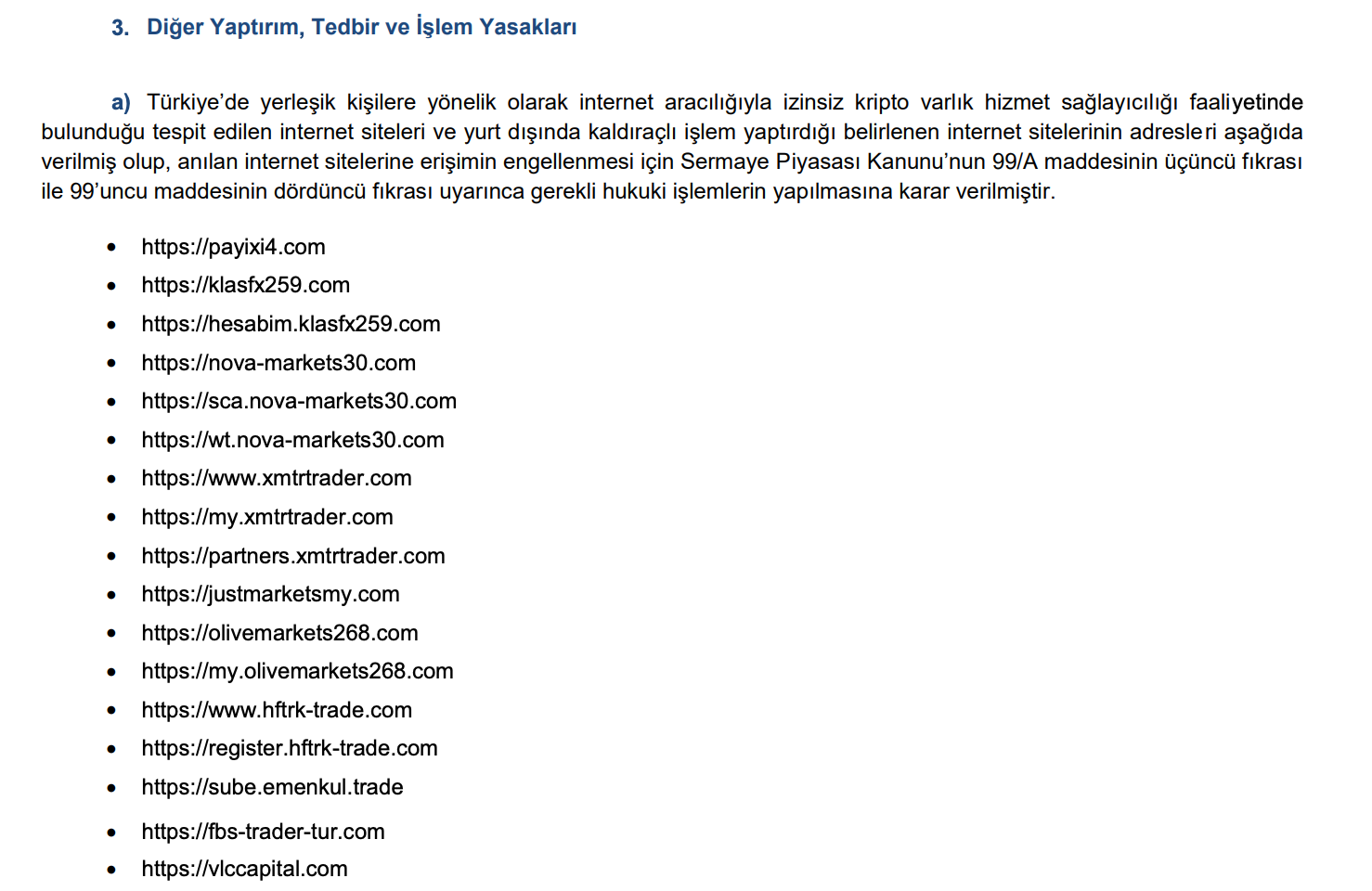

In July, the Capital Markets Board (CMB), one of Turkey’s key financial regulators, announced it had blocked access to several platforms offering “unauthorized” digital asset services, including PancakeSwap, a popular decentralized exchange.

A CMB bulletin lists blocked crypto-related sites. Source: CMB

Related: Crypto payments abroad may be legal despite domestic bans in several countries

Turkish crypto adoption on the rise

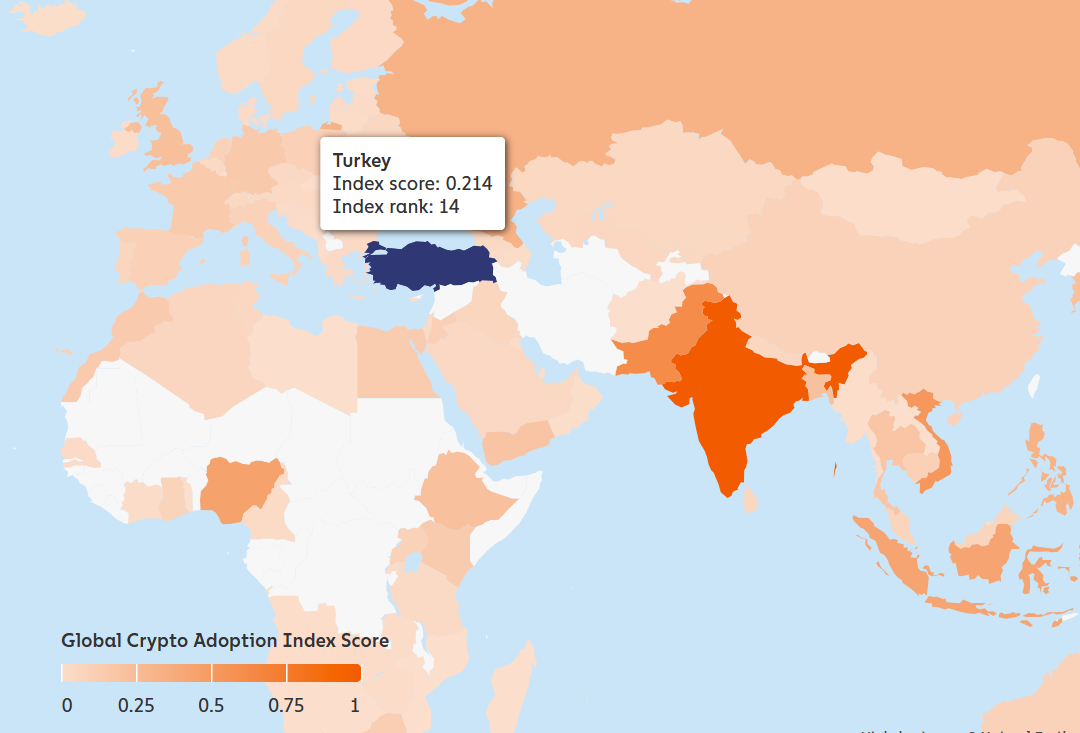

Cryptocurrency adoption in Turkey has been climbing steadily, supported by the growth of centralized retail platforms and the increasing presence of institutional crypto services in the country, according to the latest Chainalysis Global Crypto Adoption Index, released in September.

Turkey ranks 14th in the Global Crypto Adoption Index. Source: Chainalysis

One of the biggest drivers of adoption, however, has been the sharp depreciation of the Turkish lira, which has been in steady decline since 2018 amid a prolonged financial and economic crisis marked by high inflation, rising borrowing costs and loan defaults.

As the lira’s value has eroded, many citizens have turned to dollar-pegged stablecoins and Bitcoin (BTC) as alternative stores of value.

Bitcoin priced in the Turkish lira. Source: CoinGecko

To illustrate the scale of the lira’s decline: In 2020, one Bitcoin was worth about 100,000 Turkish lira. Today, that figure exceeds 4.6 million lira, reflecting both Bitcoin’s price appreciation and the lira’s steep depreciation.

Related: Singapore, UAE are the ‘most crypto-obsessed’ countries: Report

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.

More on the subject