Over 60% of users already spend with crypto cards: Study by Changelly x Simple

Press ReleasePublishedSep 30, 2025

In Q3 2025, Simple Wallet analyzed anonymized transactional data from 1,000 randomly selected European cardholders to measure actual spending behavior.

Sponsored byChangelly

October 1, 2025 – In Q3 2025, Simple Wallet analyzed anonymized transactional data from 1,000 randomly selected European cardholders to measure actual spending behavior. At the same time, Changelly surveyed over 3,000 of its users worldwide to capture self-reported adoption trends. Together, this data provides one of the most detailed looks at how crypto cards are used in practice to date.

Simple is a European crypto wallet with an intuitive UX that bridges fiat and crypto, offering cards for everyday spending. Changelly is a leading instant cryptocurrency exchange platform and global blockchain API provider.

Key findings

- 60.6% of surveyed users already use crypto cards.

- Top use cases: online transactions (66%) and everyday purchases (61%).

- Average transaction size in Europe: €40.

- Top benefits: ease of use (65%), cashback (56%), flexibility (43%).

- Key barriers: 58% don’t know what crypto cards are, and 43% cite limited merchant acceptance (Changelly survey, 2025).

Adoption: 60% already use crypto cards

Survey data from over 3,000 Changelly users shows that 60.6% are already using a crypto card, while 39.3% are not. Transaction records from 1,000 Simple Wallet cardholders in Europe back this up, showing thousands of real-world purchases each month with an average ticket size of about €40. This combination of self-reported and observed data points to a clear majority of active crypto users already spending through cards.

User motivations: Over 60% of all transactions are everyday and online purchases

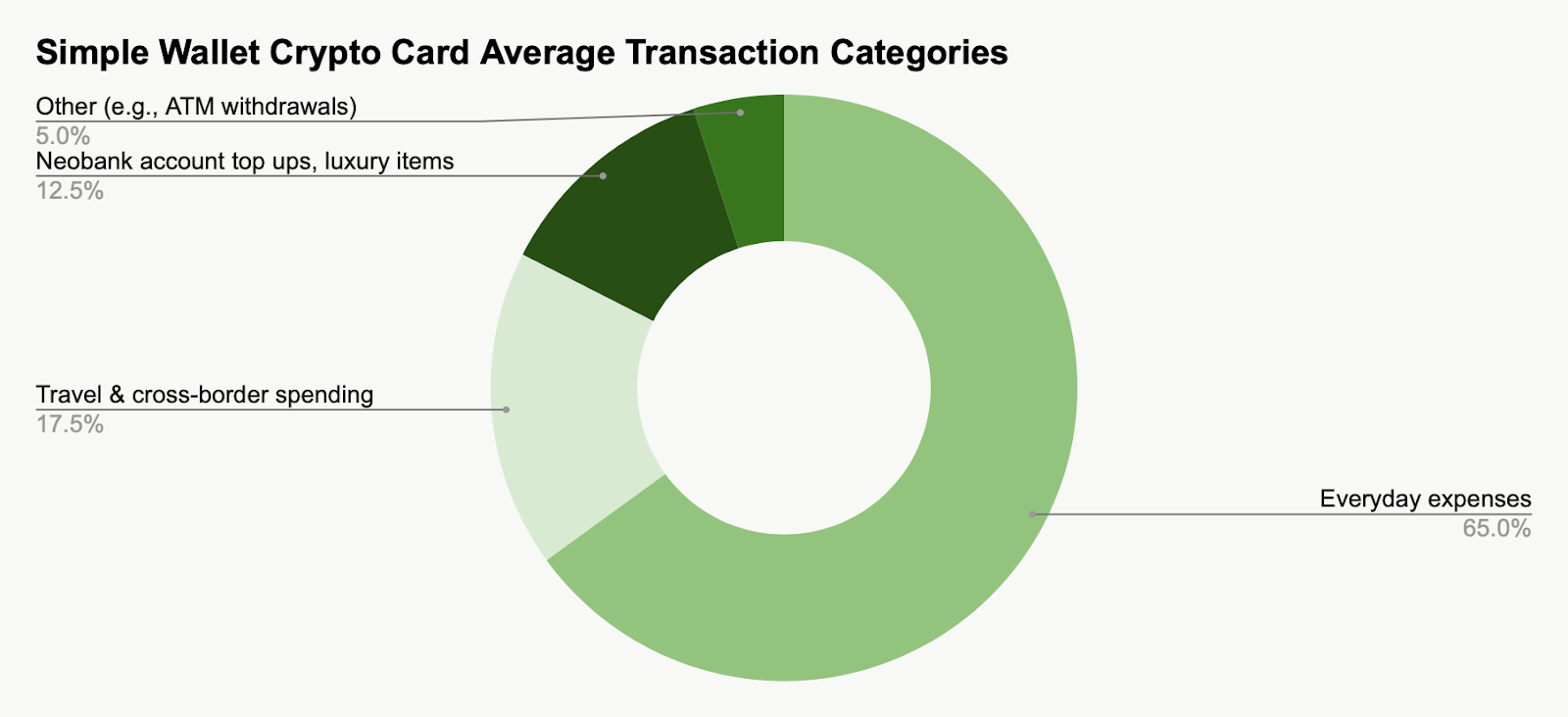

Crypto spending has shifted from occasional cash-outs to everyday use. Simple Wallet’s June 2025 analysis of 1,000 European cardholders shows that between 60% and 70% of all transactions go to routine expenses such as groceries, subscriptions like Netflix and Spotify, transport, utilities, online shopping, and cafés. Another 15% to 20% covers travel and cross-border spending: hotels, car rentals, purchases outside the EU, and tolls. Meanwhile, only 10% to 15% relates to topping up user accounts in neobanks like Revolut or high-ticket items. The average transaction size is about €40, and most payments are settled in USDC automatically converted at checkout.

Average crypto card transactions according to Simple’s user data (2025)

Changelly’s global survey tells the same story: 66% say they use crypto cards for online transactions and 61% for everyday purchases, compared with 45% for fiat conversion and 41% for travel.

Together, these findings indicate that crypto cards are functioning as utility payment rails, not just liquidation tools. Providers looking to capture this market need to focus on seamless, low-friction everyday use cases and benefits that mirror traditional cards.

“When a Simple Wallet user pays for groceries, streaming, or transport with USDC, it shows the shift: crypto isn’t a future promise, it’s already part of the everyday economy,” says Alex Emelian, CEO of Simple Wallet.

What users value most: 65% say simplicity, 56% say rewards

Survey and transaction data point to the same conclusion: crypto cardholders value what mainstream bank-card users do. In Changelly’s global survey, 65% cited ease of use as the top benefit, 56% highlighted cashback and rewards, and 43% pointed to flexibility—the ability to hold crypto until payment and spend on demand.

Simple Wallet’s data mirrors this. Customers favor crypto cards because they act like bank cards: tap-to-pay via Apple/Google Pay, instant conversion at purchase with no pre-swaps, and no wallet balance disclosure. Funds stay in crypto until checkout, keeping holders invested.

Pain points: 58% non-users claim lack of knowledge as key barrier

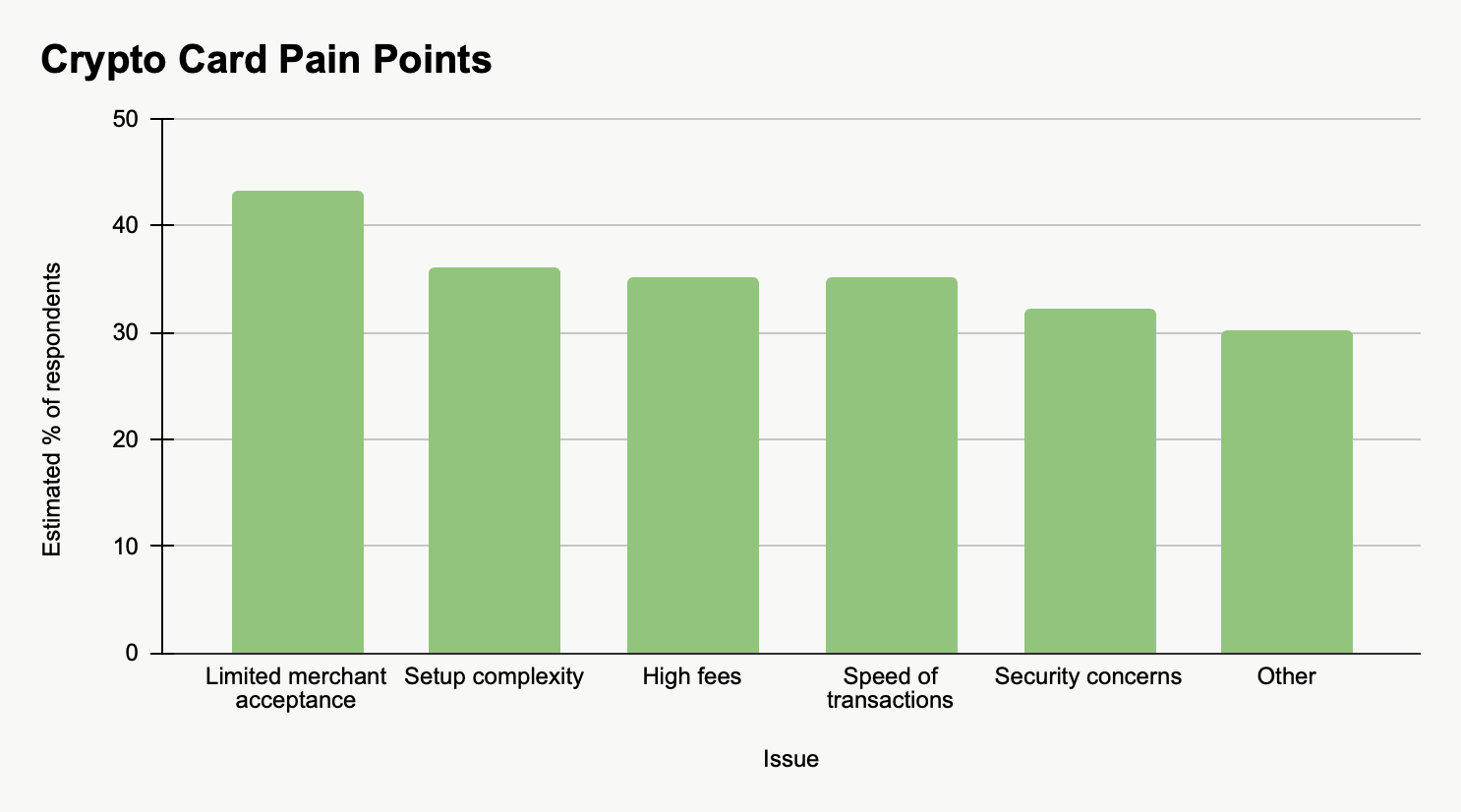

Changelly’s survey shows crypto card users face relatively few problems: 59% reported none. Among those who did, top issues were limited merchant acceptance (43%), setup complexity (36%), high fees (35%), slow transactions (35%), and security concerns (32%).

Crypto card pain points according to Changelly’s survey (2025)

For non-users, the picture differs. A lack of knowledge leads at 58%, followed by “I don’t own crypto” (24%) and smaller shares citing cost or trust.

Overall, the real bottlenecks are education, trust, and infrastructure, not the technology itself. Tackling these will likely drive adoption more than incremental feature tweaks.

Why crypto cards matter

Crypto cards are not just about spending tokens—they close the loop between Web3 assets and the real economy. Simple’s experience shows that their value lies in four operational advantages:

- Convenience. Users pay exactly like with a normal card or Apple Pay/Google Pay. No extra steps, no pre-conversion.

- Privacy. For enhanced user privacy, the merchant only sees a standard card transaction, without access to the user's crypto wallet details.

- Flexibility. Assets stay in crypto until the moment of purchase, allowing holders to remain invested and only convert at checkout.

- Crypto-native design. Cards accept direct crypto funding with a user-friendly compliance process for funding your account.

This positions crypto cards as everyday financial tools rather than speculative instruments. For businesses, they unlock new opportunities:

- Wallet providers gain higher stickiness and spend retention.

- Exchanges open revenue streams beyond spot trading.

In short, crypto cards make crypto easier to use in daily life and extend its reach across the wider financial ecosystem.

Strategic implications

Survey data shows that 58% of non-users cite lack of knowledge as the main barrier to adoption, making education the primary growth lever for issuers. Clear onboarding and in-app guidance can convert a large share of potential users without major product changes. For example, Simple has reduced registration to a five-minute online passport/ID check for EEA residents, turning what was once a complex process into a quick standard step, converting a higher percentage of their wallet users into crypto card customers as a result.

Rewards and cashback are also decisive: In the Changelly survey, 56% of respondents named rewards as a key benefit. For maximum ease of adoption, UX must also mirror traditional cards. Simple has addressed this by adopting a banking-style interface with a built-in exchange and automatic selection of low-fee networks, removing confusion about fees and settlement.

Last but not least, with stablecoins such as USDC and EURC dominating card spending, providers should optimize liquidity pools and FX routing to minimize costs and improve reliability.

Taken together, these measures—education, frictionless onboarding, rewards and stablecoin-optimized infrastructure—define the roadmap for winning a share in the crypto card market over the next few years.

“This survey shows that education and usability are the real catalysts for wider crypto-card adoption,” says Zifa Mae, Head of Product at Changelly. “Instant exchange API providers like Changelly can help by making funding and conversion seamless, while crypto cards providers focus on fast onboarding, clear rewards and stablecoin infrastructure to match the convenience of traditional cards.”

The next 5 years in crypto cards

Card functionality is likely to become standard in major crypto wallets in the coming years. Non-custodial, stablecoin cards will let users spend directly from wallets while avoiding double conversions and tax-triggering swaps.

Online banks like Revolut and N26 already integrate crypto, signaling that mainstream financial apps will soon route crypto natively. The model will shift from “convert then spend” to “spend directly,” with payroll, freelance income, and rewards flowing straight to cards.

The path forward is clear: close the knowledge gap with education, deliver seamless UX, and secure loyalty with stablecoins and rewards. Providers that execute on these levers will define the next wave of payment rails.

For a preview, Simple combines a stablecoin wallet with integrated cards, ensuring high acceptance rates. Changelly complements this with blockchain APIs, fiat ramps, and Changelly Pay for merchant crypto acceptance.

Disclaimer: This text is for informational purposes only and does not constitute financial or legal advice. Cryptocurrency investments are associated with high risks. The product or promotional offers described are not directed at, or available to, UK residents.

Subscribe to daily byte-sized crypto news from Cointelegraph

This publication is provided by the client. The text below is a paid press release that is not part of Cointelegraph.com independent editorial content. The text has undergone editorial review to ensure quality and relevance, it may not reflect the views and opinions of Cointelegraph.com. Readers are encouraged to conduct their own research before taking any actions related to the company. Disclosure.

More on the subject