Are stablecoins just digital dollars with blockchain branding?

LearnPublishedMay 20, 2026

The Iran-linked wallet case shows why some stablecoins can behave more like regulated digital dollars than fully decentralized crypto assets.

Stablecoins sit between crypto and traditional finance

Stablecoins may move on public blockchains, but many of these tokens are issued by centralized companies, backed by traditional reserves and designed to follow legal obligations.

Stablecoins can look and move like crypto on public networks, but in practice, they often behave more like regulated digital dollars. Issuers can freeze wallets, blacklist addresses and cooperate with sanctions authorities, even while the underlying blockchain continues to run normally.

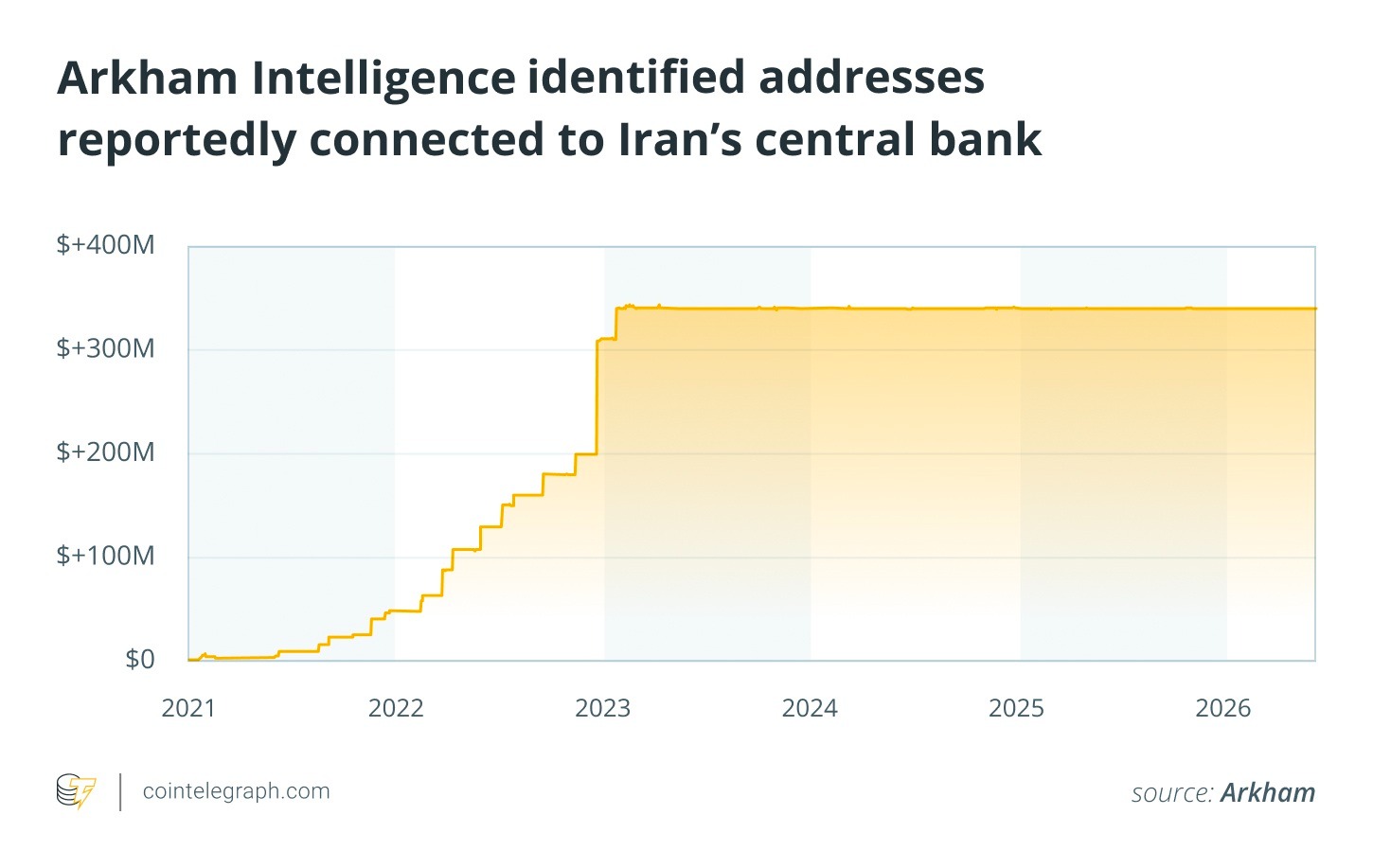

That distinction became clearer in a high-profile case involving wallets reportedly connected to Iran’s central bank. Blockchain analytics firm Arkham Intelligence publicly identified the addresses, following reports that the US Treasury’s Office of Foreign Assets Control (OFAC) had flagged two Tron network addresses linked to the institution. Soon after, stablecoin issuer Tether announced it had locked more than $344 million in USDt on those wallets in collaboration with American authorities.

The key point is simple. The blockchain did not stop working, the wallets did not disappear and the transaction history remained publicly visible. But the stablecoins inside those wallets reportedly became unusable because the issuer had the technical and legal ability to intervene.

Why stablecoins depend on traditional finance

Although stablecoins run on blockchain networks, they remain closely tied to conventional banking and financial structures. Their peg to a stable value is typically supported by reserves held in commercial banks, cash-like instruments or low-risk government securities such as short-term US Treasuries.

Issuers depend on established banking relationships to safeguard these reserves, handle conversions and enable exchange between digital tokens and traditional currency. As a result, most stablecoins behave more like digital versions of conventional money moving on faster blockchain rails than truly independent decentralized assets.

If market participants begin to doubt the quality or accessibility of the backing reserves, the peg can quickly come under pressure. Operationally, these coins also require support from legal frameworks, independent auditors, professional custodians and legacy payment networks to function across borders.

Even the largest stablecoins must maintain ongoing ties with regulators and traditional financial players to remain viable. Without reliable access to banking services, reserve accounts and established settlement systems, they could face serious difficulties preserving stability or managing heavy redemption volumes. In the end, while blockchain upgrades the speed and method of transfers, the underlying economic foundation still rests on conventional financial infrastructure.

Stablecoins vs. bank deposits: What is the difference?

Stablecoins often look more like conventional bank deposits than truly decentralized cryptocurrencies. Like regular bank balances, they represent claims on fiat currency, primarily the US dollar, and rely on institutional backing to sustain trust and day-to-day operations.

Bank deposits depend on commercial banks and central bank systems, whereas stablecoins rely on private issuers, custodians, reserve administrators and banking relationships.

Both exist within established legal and regulatory environments. Authorities can freeze traditional bank accounts through legal orders or sanctions, while stablecoin providers can block specific wallets or limit transfers when required. In each case, access to value ultimately depends on compliance requirements rather than pure technical control.

The main distinction is how the money moves. Stablecoins transfer across transparent, open blockchain networks that are publicly verifiable and accessible worldwide. Traditional bank money, on the other hand, moves through proprietary banking channels managed by financial institutions and payment networks.

As a result, many stablecoins act less like stand-alone cryptocurrencies and more like digital representations of the US dollar optimized for blockchain-based settlement and movement.

How the Iran-linked wallet case exposed stablecoin controls

The matter drew widespread notice when Arkham published detailed on-chain profiles of the wallets in question. Intelligence reports indicated that these addresses had handled hundreds of millions of dollars in transfers over multiple years.

According to blockchain monitoring firm TRM Labs, the accounts had received roughly $370 million across nearly 1,000 separate transactions dating back to 2021. The sequence showed how analytics providers, government agencies and stablecoin operators can coordinate when compliance or national security issues surface.

The case shows the difference between a decentralized network and a centrally issued token running on that network.

Why public blockchains make stablecoins easier to track

A common misunderstanding is that blockchain activity is inherently private or anonymous. However, major public networks like Bitcoin, Ethereum and Tron operate as fully visible, immutable records. Anyone with an internet connection can inspect wallet balances, transaction flows and historical activity using public explorers.

Although users interact through alphanumeric addresses rather than personal identities, specialized firms can cluster related addresses by studying transaction patterns, fund movements and interactions with centralized platforms such as exchanges. Over time, this can create detailed maps of financial activity that may be reviewed long after the transactions occurred.

Firms including Chainalysis, Arkham Intelligence and TRM Labs provide these forensic services to governments, compliance teams and law enforcement agencies worldwide.

For stablecoins, this visibility can combine with issuer-level controls, making it possible to both trace funds and restrict their movement.

Did you know? Many stablecoins include contract-level controls that allow issuers to freeze or blacklist certain addresses without stopping the underlying blockchain.

What does it mean when a wallet address gets sanctioned

When regulators sanction a specific blockchain address, they are essentially signaling that regulated entities such as exchanges, payment processors and financial institutions should avoid dealings with it.

In the US, OFAC maintains lists that now routinely include crypto wallet addresses alongside individuals and organizations. Once blacklisted, compliant platforms often restrict or block interactions with that address to stay within legal bounds.

This does not halt the underlying blockchain. The address and any assets inside it continue to exist on the ledger. However, using regulated on-ramps, off-ramps or services can become nearly impossible.

A sanctioned wallet may face serious limitations such as:

- Inability to deposit or withdraw on major centralized exchanges

- Restricted access to regulated on-ramps and off-ramps

- Limited access to compliant payment or custody services

- Additional screening when interacting with regulated platforms

As a result, the wallet can become largely cut off from the broader economy, even while the blockchain itself runs without interruption.

How stablecoin issuers can freeze digital dollars on-chain

Stablecoins like USDt and USDC are digital tokens designed for price stability, typically backed by reserves and pegged to the US dollar. This is why they often function less like independent crypto assets and more like tokenized versions of dollars moving through blockchain networks.

Unlike native cryptocurrencies such as Bitcoin or Ether, most popular stablecoins are issued and managed by centralized entities. These companies control token issuance, redemptions and the underlying smart contracts.

This setup gives issuers built-in capabilities to intervene, including:

- Blocking transfers from designated addresses

- Freezing token holdings

- Restricting access or movement of funds

- Applying contract-level restrictions where supported

Once an address is blacklisted in the smart contract, the tokens may still appear in the wallet when viewed on a blockchain explorer, but the holder often cannot send or use them effectively. The network keeps running normally because the restriction applies only at the token contract level.

Why the blockchain is decentralized while the asset is not

Not every crypto asset has the same level of decentralization. The key difference is whether a central issuer can manage, restrict or redeem the asset.

These differences matter:

- Bitcoin has no central authority that can freeze or blacklist coins at the protocol level.

- Ether operates similarly, with no issuer capable of directly controlling individual balances.

- Stablecoins like USDt and USDC typically include centralized controls that allow issuers to manage or restrict usage.

- Tokenized traditional assets often rely even more on issuer oversight and regulatory compliance.

This means a fully decentralized blockchain can still support assets that carry significant centralized elements.

Stablecoins, in particular, function more like bridges to traditional finance than fully independent crypto assets. Their reliability comes from centralized features such as banking partnerships, reserve custody, legal frameworks, redemption processes and cooperation with regulators. These elements help support price stability and adoption, but they also introduce clear points of intervention and control.

Why stablecoin issuers work with regulators

Stablecoin companies face strong regulatory expectations because their tokens act as digital versions of traditional currencies.

To keep banking relationships, access payment networks and hold reserves safely, issuers frequently collaborate with law enforcement and sanctions bodies. Refusing to cooperate could lead to heavy fines, legal trouble or even the loss of their ability to operate across borders.

From the issuer’s point of view, freezing tokens linked to suspected sanctions evasion, ransomware payments, terrorist financing, fraud or major security breaches may be necessary to preserve regulatory standing and credibility.

Tether, for instance, has publicly stated that it works with authorities worldwide and has blocked billions in assets tied to illegal activities over time.

Advocates see these capabilities as essential for reducing misuse and protecting users. Critics, however, argue that they undermine the core promise of censorship resistance that drew many people to crypto in the first place.

Did you know? A wallet can technically hold frozen stablecoins indefinitely. The tokens may still appear on a blockchain explorer, but transfer functions can stop working once the issuer blacklists the address linked to those funds.

Why self-custody does not always mean full control

The recent events involving sanctioned wallets highlight an often-overlooked reality: Holding your own private keys does not always mean you have full, unrestricted control of your funds.

You can self-custody certain assets without depending on a central issuer. Bitcoin and Ether are the clearest examples because no company can freeze balances at the protocol level. But with many stablecoins, controlling the wallet does not always mean controlling the token without restriction. The issuing company may still be able to blacklist or freeze those specific assets.

For instance:

- With Bitcoin or Ether, there is no central issuer that can freeze your holdings at the protocol level.

- With USDt or similar stablecoins, the issuer retains the technical ability to blacklist and freeze tokens in a wallet, even if you hold the keys.

This difference surprises many people who enter the crypto space primarily through stablecoins. Simply owning the wallet and truly controlling the asset are not always the same.

Stablecoins are a bridge between blockchain and traditional finance

Stablecoins are frequently promoted as building blocks of a decentralized financial system, but their role is more complex.

While stablecoins enable near-instant global transfers over public blockchains, they remain subject to freezing, monitoring or limitations when regulators intervene.

This does not indicate failure. Rather, stablecoins appear to be developing into a hybrid type of digital currency that combines blockchain speed and efficiency with the backbone of conventional finance. Instead of fully displacing the existing system, they are becoming programmable, borderless, internet-native versions of traditional dollars. They stay linked to institutions, regulatory oversight and government-supported currencies.

The underlying technology is innovative, but the core elements of trust, control and legal authority remain strikingly similar to those in traditional money.

This article is produced in accordance with Cointelegraph's Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

More on the subject