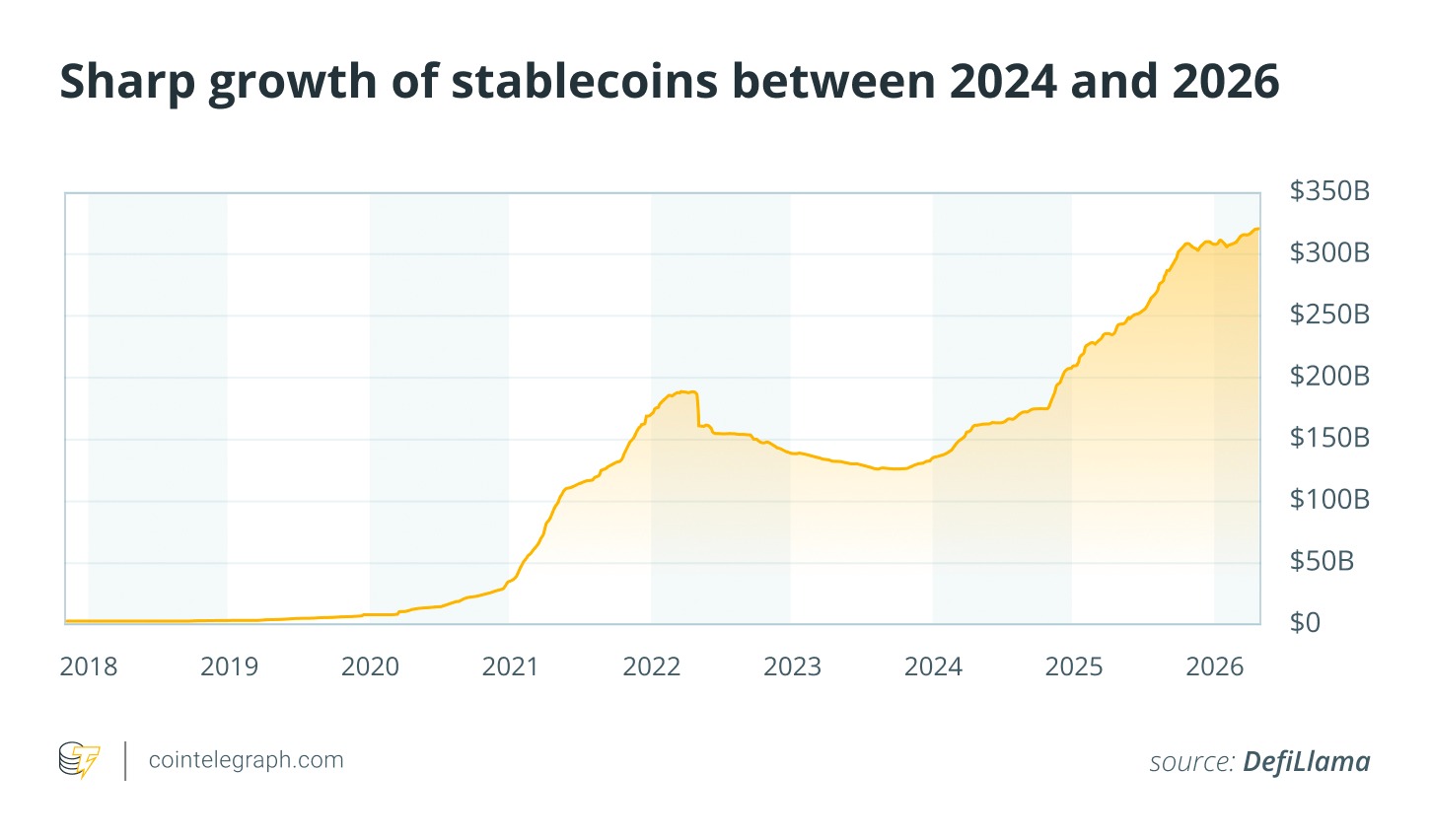

How the stablecoin market tripled from $100B to $300B in one year

LearnPublishedMay 15, 2026

From trading liquidity to cross-border payments, stablecoins have scaled rapidly. The $300 billion milestone shows how they are reshaping digital finance.

The $300 billion milestone: What is driving stablecoin growth?

The stablecoin market’s surge past the $300 billion mark stems from multiple overlapping dynamics that aligned over time. While the market may appear to have tripled quickly from $100 billion, the growth was more gradual. It built up over time and accelerated during a strong period for crypto and stablecoin adoption.

Throughout 2025, overall stablecoin issuance rose significantly, carrying the total well above $300 billion. This marked a move into fresh territory, where these assets function as core elements of wider financial systems. This evolution signals a broader shift from specialized applications to use cases across trading, cross-border payments, regulatory frameworks and even international relations.

At the start of 2025, the market stood slightly above $200 billion and grew by nearly $100 billion over the following 12 months. By the beginning of 2026, aggregate supply had settled in the $317 billion to $320 billion zone.

No single element propelled this rise. It resulted from the convergence of stronger cryptocurrency market participation, improved regulatory environments, greater institutional involvement and growing applications in everyday finance. The increase in supply also aligned with a broader rebound in digital assets, which typically heightens the need for reliable dollar-linked liquidity options.

Crypto’s liquidity layer regained momentum

Stablecoins have again become one of the main ways traders move money across crypto markets. They serve as an essential bridge for transferring value between trading venues, opening and closing positions and engaging with decentralized finance (DeFi) applications.

As overall trading activity rebounded in 2025, demand grew for efficient, dollar-linked instruments that could keep pace with market movements. Their ability to enable near-instant transfers without relying on conventional banking systems made stablecoins especially useful when volatility and volume increased.

This growth both reflected and helped reinforce the broader crypto market recovery. As more money moved through stablecoins, trading became easier. That encouraged more activity and added further demand for stablecoins.

Did you know? Some stablecoins can process more daily transaction value than major card networks during periods of peak crypto activity. This is largely because bots and arbitrage traders constantly move funds between exchanges to capture small price differences across markets.

Regulatory clarity strengthened market confidence

A key factor behind this expansion was meaningful regulatory progress in leading financial centers.

In the US, ongoing policy discussions and draft legislation pointed toward formal rules focused on asset reserves and transparency obligations. Meanwhile, the EU’s Markets in Crypto Assets Regulation (MiCA) introduced comparable standards. Hubs such as Singapore, Japan and the UAE advanced their own frameworks to support compliant issuance and adoption.

These developments did not remove all risks or doubts, but they provided a clearer structure that could attract larger institutional players. As a result, stablecoins started to be seen less as speculative tools and more as established financial instruments operating within clearer guidelines.

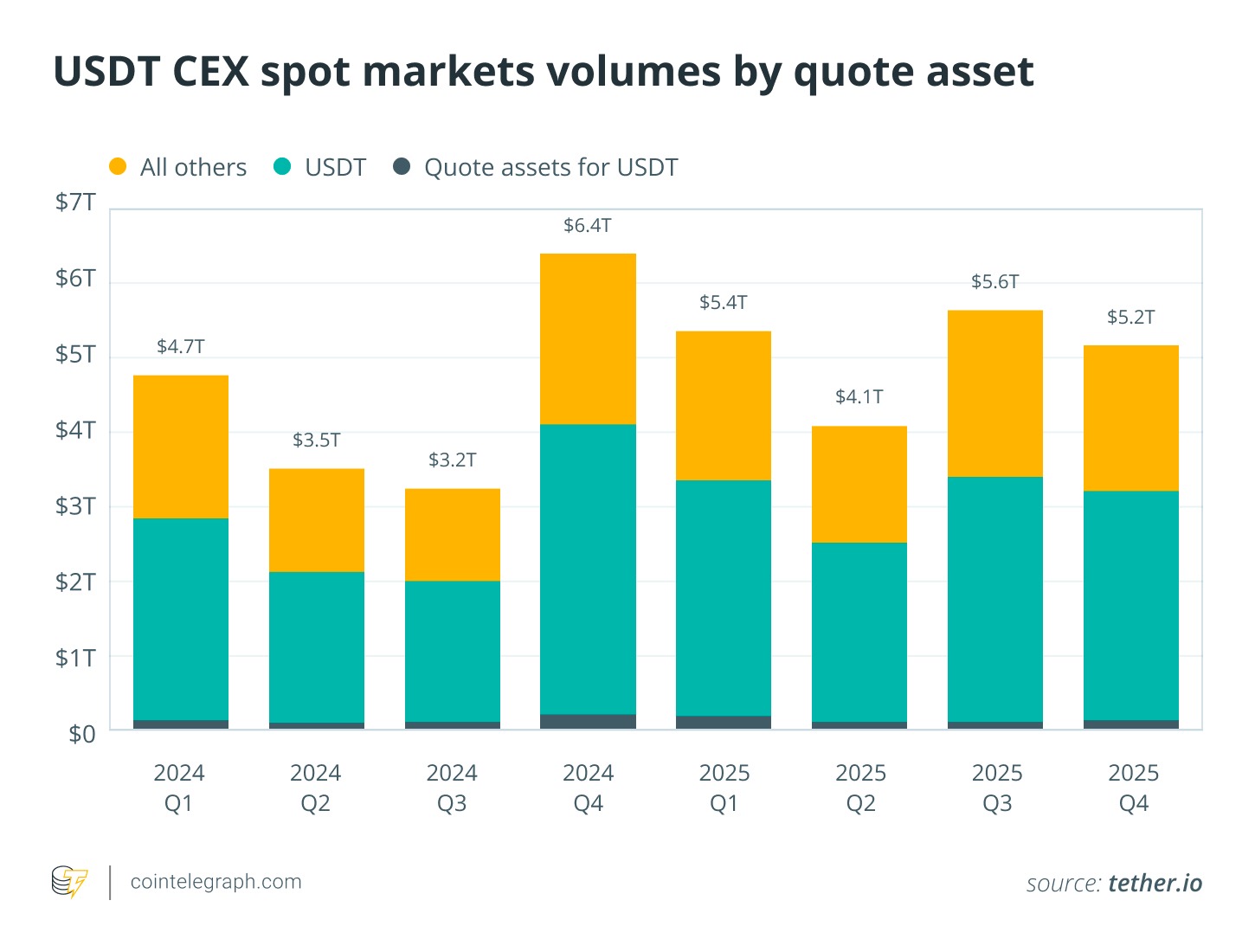

Scaling of two dominant stablecoin models

The stablecoin market is defined by two leading players that have grown through distinct approaches: USDt and USDC.

USDt has maintained its dominant position as a go-to liquidity provider on exchanges worldwide, especially in markets where traditional dollar banking services are restricted or difficult to access. Its expansion remains closely linked to overall trading volumes and strong offshore demand for dollar-denominated assets.

USDC, on the other hand, has followed a compliance-focused path. Its progress has been fueled by deeper connections with banks, payment providers and corporate applications, particularly in regions that prioritize regulatory compliance and transparency.

These contrasting paths show how stablecoins have expanded on separate fronts: one driven mainly by on-chain trading needs, the other by closer alignment with traditional finance.

Cross-border transfers become a major growth area

Outside of trading, stablecoins are seeing growing adoption for cross-border transactions. This shows that stablecoins are steadily moving beyond crypto-focused use cases into everyday global finance.

Conventional remittance and business payment channels remain slow and costly. Stablecoins provide a more efficient option by reducing reliance on multiple intermediaries and enabling quicker value transfers across borders.

Although aggregate stablecoin transaction volumes routinely surpass trillions of dollars each month, a large portion comes from crypto market activity such as trading, arbitrage and liquidity provision. Still, genuine off-chain payment activity, particularly in corporate transfers and personal remittances, continues to grow at a strong pace.

Did you know? A large portion of stablecoin demand comes from countries facing currency volatility. In these markets, users often treat dollar-pegged tokens like digital savings accounts, even without earning interest, in an attempt to preserve purchasing power.

A geopolitical dimension took shape

Stablecoins are also starting to intersect with national policy decisions, as governments assess how these dollar-linked assets affect capital flows, monetary control and cross-border settlement options.

A major example is Russia’s proposed crypto legislation, which classifies digital assets as property. While it prohibits the use of digital assets for everyday domestic payments, it permits them in international trade settlements. This balanced stance shows how authorities can maintain strict control over local currency matters while allowing greater flexibility for cross-border financial operations.

In such settings, stablecoins offer practical utility for global transactions, particularly in regions facing economic sanctions, capital controls or restricted access to conventional banking networks. While adoption varies widely, these developments show that stablecoins are now becoming part of broader state-level financial and strategic planning.

Stablecoins are reshaping US treasury demand

A subtler but significant part of stablecoin growth lies in its connection to conventional financial markets.

Most fiat-collateralized stablecoins are collateralized by reserves consisting of cash and short-term government debt instruments. As total issuance grows, stablecoin issuers have become meaningful participants in markets such as US Treasury bills.

This dynamic creates a channel through which demand for digital dollar equivalents flows back into traditional assets. The full effects of this relationship, including its impact on market liquidity, overall stability and future regulatory needs, remain under review.

Did you know? Stablecoin wallets do not always belong to individuals. Many are controlled by automated trading systems that can execute thousands of transactions per minute without human involvement, quietly driving a significant share of total network activity.

Interpreting the volume with caution

Despite impressive growth figures, stablecoin data requires careful interpretation. A significant portion of on-chain activity reflects internal transfers, trading strategies and liquidity movements rather than direct real-world economic use.

Raw transaction figures can overstate real activity because they include automated trading loops, internal exchange movements and other non-payment-related flows. As a result, the true scale of practical, real-economy usage remains more modest than surface numbers suggest.

Even after these adjustments, however, the data still points to substantial progress. What stands out is not just the volume but the widening range of use cases, spanning trading, payments and institutional transfers.

Risks continue to shape the market

The growth of stablecoins also brings a set of risks that continue to be debated. These include reserve transparency, issuer concentration, redemption pressures and potential spillover effects on traditional financial markets.

The high degree of market concentration is a prominent risk, as a handful of issuers control the majority of supply. Persistent questions around reserve verification, redemption reliability and inconsistent global regulations add to the complexity. There are also systemic stability concerns, particularly in scenarios involving sudden, large-scale withdrawals during periods of market stress.

Furthermore, deeper integration into cross-border finance raises important issues related to compliance, sanctions enforcement and supervisory coordination. These challenges do not undermine the overall growth narrative, but they define the environment in which it is developing.

Subscribe to daily byte-sized crypto news from Cointelegraph

This article is produced in accordance with Cointelegraph's Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

More on the subject