Crypto markets won’t fly without more credit

OpinionPublishedFeb 12, 2026

Crypto markets lack credit. Pre-funded trades and thin prime brokerage cause liquidity droughts that amplify volatility and cap institutional adoption.

Opinion by: Harpal Sandhu, CEO of Integral

Despite the recent plummet in Bitcoin (BTC) and other major cryptocurrencies, 2025 was a high watermark year for crypto as new price highs were hit for major coins.

The US administration’s regulatory push provided a seal of approval, signaling that crypto was on the path to maturity. Banks, that have been cautious with crypto over the past five years, rapidly changed their tune.

Beneath all this progress lie deeper structural issues in the crypto market that more US regulation won’t solve.

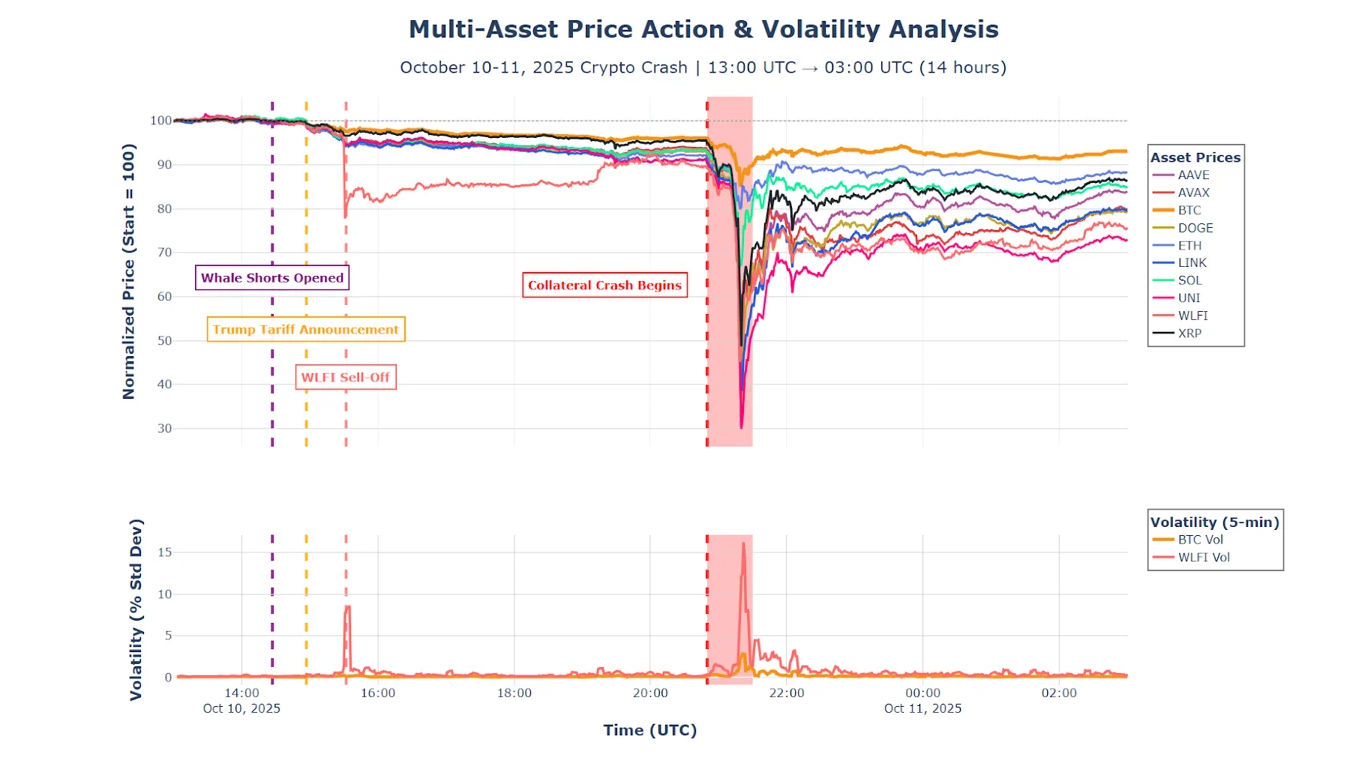

The October 2025 market correction clearly revealed liquidity issues which are still prevalent today. While they are not causing the current crash, illiquidity hampers market stability.

A shortage of crypto credit and prime brokerage are directly contributing to crypto’s liquidity droughts. If the industry does not create more crypto credit, an artificial ceiling will be placed on cryptocurrencies.

Market shock

The Oct. 10, 2025 correction itself was not unusual; sudden sharp volatility continues to be a staple of crypto. It’s for this reason some market participants, like hedge funds, find it attractive. What was more revealing was how quickly liquidity evaporated and how slowly it has — or in this case hasn’t — returned. Geopolitical and policy decisions have caused spikes in volatility across traditional financial markets, including equities, bonds and foreign exchange (FX).

Synchronized price declines and volatility spikes during October’s correction highlight the market’s limited ability to absorb selling pressure under stress. Source: Amberdata.

Yet liquidity in these markets recovered rapidly, allowing traders to easily access these markets. FX traders have highlighted how advancements in trading technology have made those markets so efficient that spreads have disappeared. It leaves very little for those firms that benefit when the price between buy and sell orders widens.

Structural, not cyclical, issues

The same cannot be said of crypto. Not only did liquidity dry up in the aftermath of Oct. 10, but it remained thin months later as sellers struggled to find buyers. The same is still the case today, as the value of major coins plummeted. The fall in value is due to a loss of conviction in cryptocurrencies as an asset, but poor liquidity is being fuelled by structural issues.

One of the principal constraints is a shortage of credit. In crypto, trades are mostly pre-funded, and the use of leverage for market making is small. When volatility spikes, capital is quickly withdrawn, and spreads widen dramatically. The absence of sustainable, transparent credit mechanisms leaves the market brittle at precisely the moments when liquidity is most critical. This isn’t necessarily enough to stop a decline in prices, but it can shore up market conditions.

To overcome these structural issues, the industry needs to look at what works well in traditional finance and adopt similar mechanisms that play into crypto’s decentralized finance strengths. Better access to credit is the essential step.

Related: Mercado Bitcoin expands LatAm RWA push with $20M in Rootstock private credit

In FX, for example, market makers can become risk takers temporarily, supported by credit lines from prime brokers that allow them to continue quoting prices to liquidity takers even during periods of high stress. Credit fuels market activity. Crypto lacks this support due to the absence of adequate credit.

More crypto prime brokerage is essential

Regulation constrains how investment banks engage in crypto. The capacity of banks to hold and finance crypto exposures is limited by Basel III and the prudential rules around crypto assets, which imposes high capital requirements. Even if a more favourable US administration loosens these rules, the likelihood of banks entering crypto prime brokerage at scale is low due to the volatile nature of crypto.

The crypto market needs a resilient and wide layer of crypto prime brokerage to provide more credit and better access to it if liquidity conditions are to improve.

In many cases, there are buyers and sellers out there, but they exist in fragmented pools between isolated markets. Better access to credit via prime brokers that can connect the major liquidity pools would substantially improve liquidity, with market makers and investors not needing to wholly pre-fund trades at isolated venues.

Capital can be used more dynamically instead of being locked up, which is prevalent today. This would enable firms to deploy more of their capital, connecting with more buyers and sellers to place more trades.

At the same time, crypto prime brokers connected across different pools and major market makers can enable netting between counterparties, which in turn frees up capital for more trading. Crucially, broader provision of credit allows more institutional firms to directly participate in spot cryptocurrency markets bringing much needed participants to deepen trading and liquidity.

Credit, combined with trading and settlement infrastructure, would quickly bring more firms together with credit and shared infrastructure for margin exchange and settlement.

Looking at crypto markets as they are today, this scenario would help to stabilise conditions, with credit and margin offsetting between venues helping to reduce air pockets and smooth execution during stress.

The crypto market structure expand credit access in 2026. Regulatory developments or crypto friendly administrations will not be enough to power the asset class forward amid dramatic sell offs. If more credit is available with more convenient access for most firms, the crypto market will have deeper trading activity and more resilient liquidity.

Most crypto prime brokerages today do not have the ability to scale to meet market demand or connect the crucial liquidity pools and liquidity providers to move the dial.

More must be done. Failure to broaden credit access will limit crypto to being an asset class of booms and busts.

Opinion by: Harpal Sandhu, CEO of Integral.