Why 1 in 3 European investors would switch banks for crypto access

LearnPublishedMay 23, 2026

A new survey shows that 35% of European investors would change banks for crypto services, highlighting growing demand, trust gaps and the role of regulation.

How crypto is entering core banking decisions

Cryptocurrency integration is evolving from a specialized add-on into a core factor influencing client retention for traditional banks. Across Europe, digital assets are now playing a growing role in how clients assess their main financial providers.

According to research from Börse Stuttgart Digital, more than one-third of European investors say they would switch to a rival bank offering stronger cryptocurrency capabilities. This points to a meaningful shift: Access to crypto is moving from an optional extra to a core influence on loyalty within everyday banking.

The study, which drew on input from approximately 6,000 investors in Germany, Italy, Spain and France, found that about 35% would consider changing their primary bank to access better crypto options.

Expectations are shifting as well. Close to one in five participants expect their primary bank to offer crypto services within the next three years. This suggests a growing belief that digital assets could become a more common offering alongside conventional products such as deposits, stocks and funds inside regular banking platforms.

This interest is grounded in real behavior. Roughly 25% of those surveyed already own crypto, and 36% intend to make further investments over the next five years. The findings suggest that crypto is becoming a recurring consideration for some investors rather than a passing area of interest.

Demand is strong among existing crypto investors

Existing crypto holders tend to demonstrate high interest in switching banks. Those already familiar with digital assets tend to see restrictions in traditional banking as an inconvenience instead of a necessary safeguard.

National variations support this pattern. Spain leads with crypto ownership close to 28%, followed by Germany at 25%, Italy at 24% and France at 23%. Although the gaps are modest, they reflect a widespread group of crypto-experienced investors throughout Europe’s major markets.

This development reframes the discussion away from basic interest in crypto toward the preferred channels for obtaining it.

Did you know? Bank switching has historically been driven by factors such as fees, interest rates and service quality. Crypto is now among the first major new asset categories in decades to influence that decision.

Why investors seek crypto services from banks

For many investors, the value lies in seamless integration rather than isolated trading. Banks already oversee identity checks, transfers and broader wealth management.

Incorporating crypto into this environment reduces the hassle of moving money between different services or learning new platforms.

From the client’s viewpoint, this offers greater simplicity through:

- A unified view across different asset types

- Established regulatory and reporting standards

- A sense of continuity from a trusted institution

Put simply, the interest centers on ease of use and bringing everything together, not primarily on high-risk trading.

Confidence issues continue to limit crypto uptake

Even with growing enthusiasm, progress is being held back by ongoing concerns around oversight and knowledge.

The survey indicates:

- 76% of participants consider crypto regulation inadequate

- More than 60% describe themselves as insufficiently knowledgeable about digital assets

These numbers reveal a clear gap between interest and readiness. People may want access, yet many hesitate to manage the uncertainties on their own.

This creates an opportunity for banks to offer organized, well-explained services and support. Success in this area will likely depend on clearer regulatory frameworks.

Did you know? Europe’s crypto-friendly banking experiments date back to the early 2010s, when a handful of smaller institutions began exploring Bitcoin custody and related services. This was years before many mainstream banks publicly treated digital assets as a legitimate financial category.

How Markets in Crypto-Assets Regulation (MiCA) is shaping sentiment

The EU’s MiCA regulation, which took full effect for crypto service providers on Dec. 30, 2024, is beginning to shape how investors view digital assets.

Almost half of the respondents indicated that MiCA has made crypto feel more secure and appealing. By establishing uniform standards for licensing, transparency and oversight across the EU, the framework helps reduce inconsistencies that previously existed between individual countries.

Sector leaders have highlighted the significance of this development. Building trust through clear regulatory measures will be critical for the next stage of mainstream crypto adoption.

That said, MiCA brings order rather than removing all risks entirely. This important distinction will continue to guide how banks approach and present their crypto-related services.

Banks are opting for collaboration over solo development

The research reflects a wider industry shift in which conventional financial institutions are turning to crypto technology providers instead of building their own solutions from scratch.

Börse Stuttgart Digital was among the earliest German entities to obtain a full EU-wide MiCA license through its custody arm in early 2025. The company now provides back-end infrastructure to banks, brokers and asset managers looking to add crypto capabilities.

This approach points to a future in which many banks integrate crypto through strategic partnerships. It can help them offer compliant custody, trading and settlement options while avoiding the complexities of managing the core technology themselves.

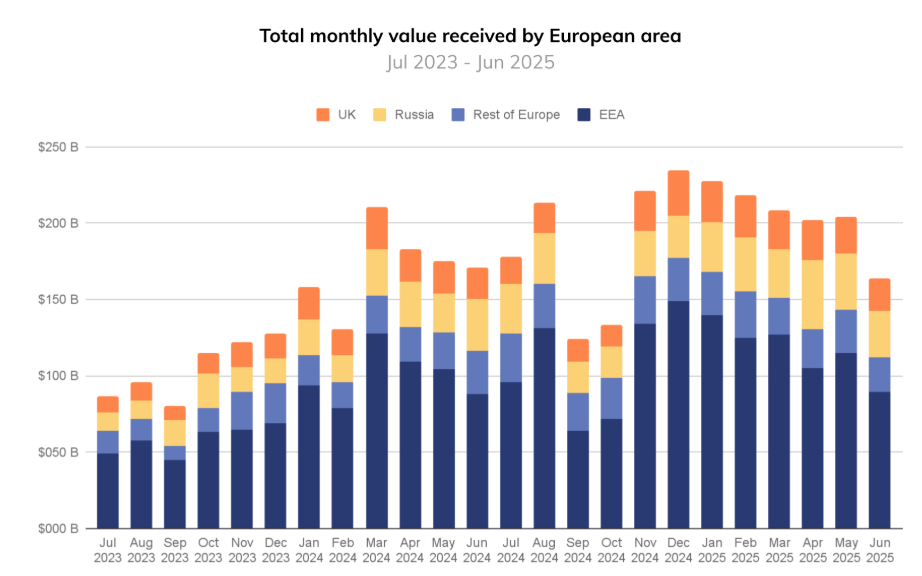

A mature European crypto market

The push for crypto access within traditional banking is happening against the backdrop of an already sizable regional market. Recent Chainalysis data points to strong crypto volumes across Europe.

From July 2024 to June 2025:

- Russia accounted for roughly $376 billion in crypto transactions

- The United Kingdom saw around $273 billion

- Germany recorded approximately $219 billion

These figures show that crypto activity is far from insignificant. It already forms a meaningful part of financial activity in the region. The main challenge is bridging this activity more effectively with established, regulated banking channels.

Regulatory vigilance persists even after MiCA

Although MiCA has brought greater predictability, European regulators continue to urge restraint. The European Securities and Markets Authority has cautioned companies against exaggerating the level of protection the new rules actually provide.

This matters for banks because customer expectations may not always align with regulatory reality. When introducing crypto services, institutions must clearly explain:

- Which offerings are covered by MiCA safeguards

- The significant price fluctuations involved

- The limits of investor protections

Poor communication in these areas could erode the very confidence banks seek to build.

Did you know? A growing number of European fintech apps are experimenting with “round-up” crypto allocation. This involves automatically converting small spare amounts from everyday purchases into digital assets, blending traditional spending habits with crypto accumulation.

Implications for European investors

Moving crypto services into traditional banks could deliver several practical advantages. These include streamlined account opening, secure storage, smoother links with existing financial holdings and more consistent supervision.

This shift could reshape the banking sector, moving it away from the traditional role of a static wealth repository and toward a more dynamic entry point for digital assets. As this market develops, modern investors’ expectations are likely to rise. They may seek a unified financial ecosystem that provides clearer insights, real-time portfolio tracking across asset types and automated tax reporting built directly into their primary banking dashboards.

Nevertheless, the fundamental nature of digital assets remains the same. Significant price swings, market fluctuations and ongoing regulatory developments will continue to influence outcomes. While access may become easier, the underlying risks will not disappear.

Crypto as a new arena for bank competition

Providing crypto capabilities is becoming a key differentiator in the competition for clients. Banks have long competed on factors such as deposit rates, credit offerings and user-friendly apps. The option to provide properly regulated crypto services is now joining that list.

With roughly one in three investors open to changing their primary bank for better crypto features, this trend has moved beyond speculation. It is happening gradually, can be measured and carries growing weight.

As rules become more established and supporting systems develop, the central challenge for banks is not simply deciding whether to enter the space. They need to determine how best to implement crypto services while strengthening client trust, controlling exposure and responding to changing demand.

This article is produced in accordance with Cointelegraph's Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

More on the subject