Data Suggests Some Americans May Be Buying Crypto With Stimulus Check

Latest NewsPublishedApr 18, 2020

Data suggests that a portion of the American population may be spending their coronavirus stimulus check on cryptocurrency.

A chart published by Brian Armstrong, CEO of United States crypto exchange, Coinbase, suggests that a small portion of the American population may be using their coronavirus stimulus checks to purchase cryptocurrency.

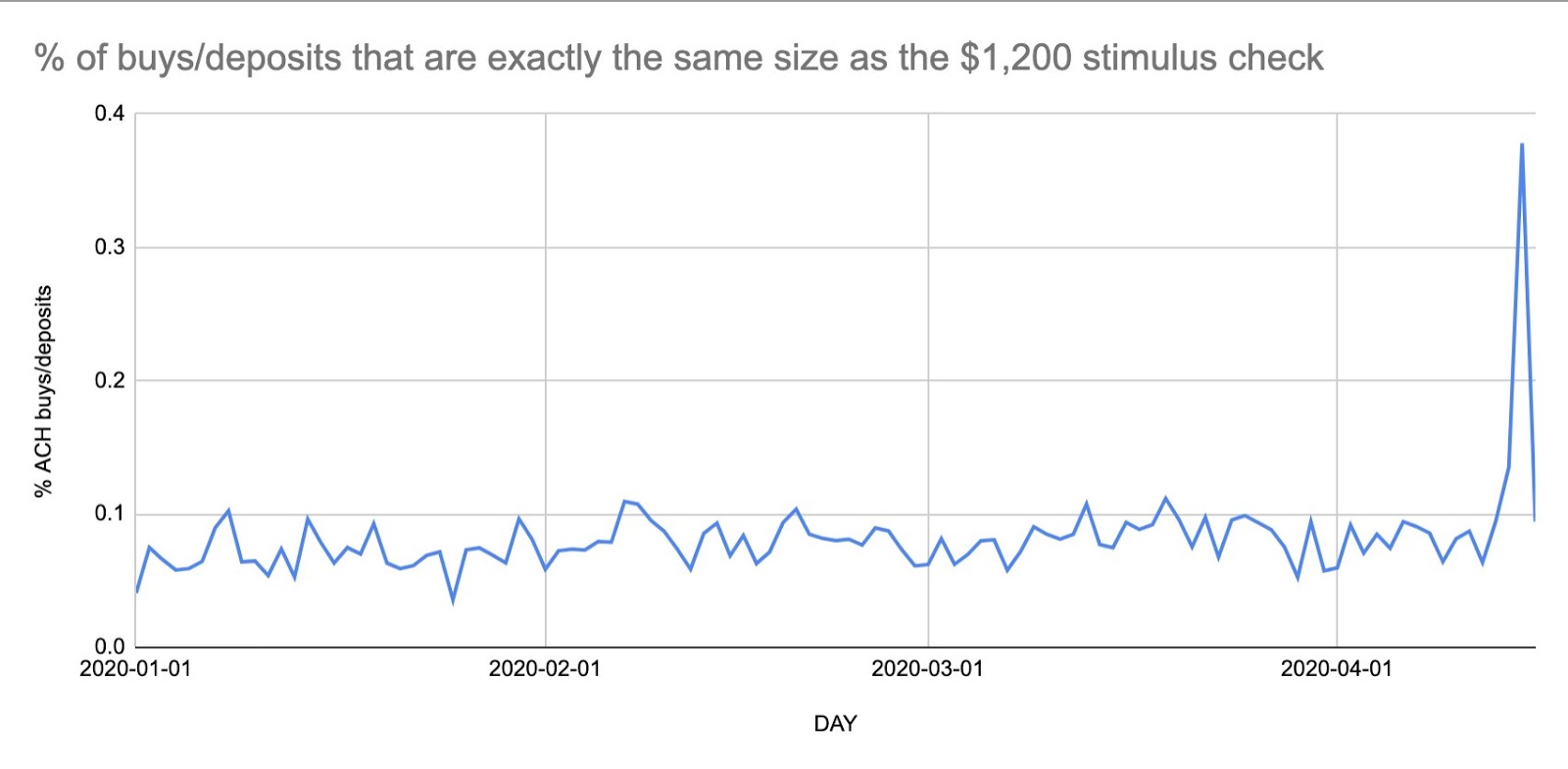

A tweet, published by Armstrong on April 17, shows that the percentage of deposits and buys worth $1,200 — the exact value of the stimulus check — recently increased over four times. While the tweet does not explicitly state so, Armstrong’s position at Coinbase may suggest that this is the exchange where the data comes from.

Percentage of buys and deposits worth $1,200 each day. Source: Twitter

Coinbase did not answer Cointelegraph's request for more information by press time.

Financial aid for a pandemic-struck economy

The upsurge in the amount of $1,200 deposits and buys coincides with when residents began receiving stimulus checks, making the stimulus appear to be the most likely source of those funds.

The stimulus checks are meant to ease the economic hardship suffered by many U.S. residents who lost their jobs or are seeing much lower income amid the pandemic.

Many production activities, especially customer-facing social activities such as restaurants or cinemas, closed worldwide to help stop the spread of the coronavirus. These closures have left many without a source of income.

As the Washington Post recently reported, even low-income Americans who do not file tax returns have the right to receive the package. Parents are entitled to an additional $500 per child.

As Cointelegraph previously reported, the demand for the stimulus checks is so great that the servers of some banks were unable to manage the request and failed to work properly. About 80 million U.S. residents have access to aid.

Wayne Chen — CEO of Interlapse and founder of virtual currency platform Coincurve — recently told Cointelegraph that the stimulus package may push the Bitcoin (BTC) market upwards.

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.

More on the subject