DCG-backed Korean exchange faces closure if it can’t find banking partner

Latest NewsPublishedSep 17, 2021

South Korean crypto exchange Gopax has told users if it can’t resolve its banking difficulties before a looming regulatory deadline, it will need to shut down.

South Korean crypto exchange Gopax, which is backed by Digital Currency Group, is facing potential closure ahead of the country’s fast-approaching deadline for platforms to submit their requests for an official operating license.

To be eligible for a license, all crypto exchanges must show evidence that they are operating using real-name accounts at South Korean banks. The catch is that domestic banks have, for the most part, refused to engage in any risk assessment process for the country’s numerous small and medium-sized exchanges and have only been confident enough to service the country’s top four trading platforms: Upbit, Bithumb, Korbit and Coinone. The deadline for all license applications is now just one week away, on Sept. 24.

In a notice to users published on Friday, the Gopax team wrote that the exchange “is currently negotiating with a financial institution to establish a real-name verification deposit and withdrawal account,” as stipulated by the new regulatory regime.

Until Sept. 24, the exchange will continue to operate its Korean won crypto trading services as normal, but if the negotiations do not resolve the issue, Gopax has warned that it will inform users of the end of support for won transactions, deposits and withdrawals in a follow-up notice. The platform has already ceased services for non-Korean users, who are prohibited from using the country’s exchanges under the new rules.

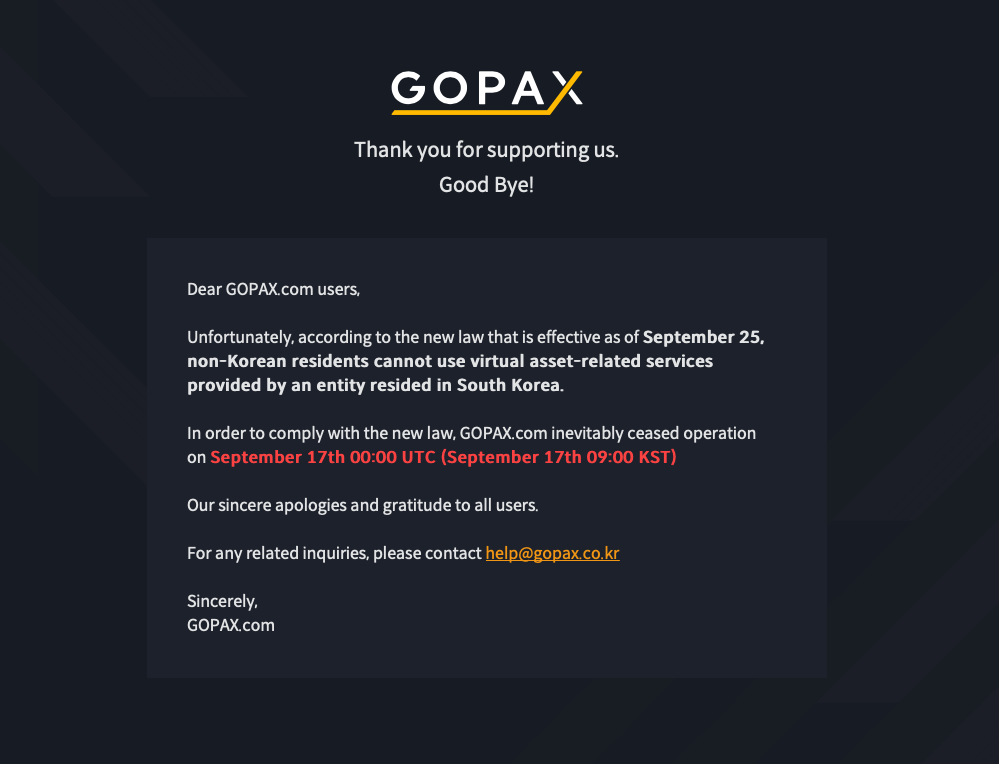

Gopax landing page accessed from outside of South Korea on Sept. 17. Source: Gopax

Gopax’s operator is a company called Streami, which has received funding from Shinhan, one of South Korea’s largest commercial banks. The exchange operator has been proactive in trying to establish the platform’s compliance credentials, working to acquire an ISO/IEC 27001 certification and K-ISMS certification, both in 2017. CryptoCompare currently ranks Gopax as the top platform in the country when taking factors such as legal and regulatory metrics, the caliber of investment, quality of data provision, and trade surveillance into account.

Related: South Korean crypto exchanges face Sept. 24 deadline to submit licence request

Experts have estimated that close to 40 of South Korea’s estimated 60 crypto exchange operators will be forced to shut down due to the new licensing rules. The Financial Services Commission, which is overseeing the new regulations, has justified its requirements by arguing that there has been high demand from traders for more protection for their assets held on smaller cryptocurrency exchanges.

Banks have themselves contested the incoming measures, arguing that they are essentially being asked to indirectly vet the country’s exchanges by having to take responsibility for issuing real-name accounts. One banking industry representative claimed that this is a “dangerous and costly task” for financial institutions.

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.