Fenwick denies allegations that it was key to multibillion-dollar FTX fraud

Latest NewsPublishedAug 28, 2025

Fenwick & West, a law firm once contracted by FTX, asked a judge to toss an updated lawsuit that claims it was key to the exchange’s fraud.

Law firm Fenwick & West denied allegations from an updated class-action lawsuit claiming it was central to crypto exchange FTX’s fraud and eventual collapse.

Earlier this month, FTX users asked to update their suit against Fenwick, first filed in 2023, claiming new information from a bankruptcy and criminal case shared evidence that the law firm “played a key and crucial role in the most important aspects of why and how the FTX fraud was accomplished.”

Fenwick told a Florida federal judge in a filing on Monday that the court should deny FTX users’ request to update the suit against the firm, arguing their theory that it helped the exchange carry out fraud “is as facile as it is flawed.”

“Fenwick is not liable for aiding and abetting a fraud it knew nothing about, based solely on allegations that Fenwick did what law firms do every day — provide routine and lawful legal services to their clients,” it said.

Lawsuit uses “stale information,” Fenwick says

The new accusations against Fenwick stem from a massive multi-district class-action lawsuit filed by FTX users after it collapsed in late 2022.

The group has also brought claims against celebrities and companies alleged to have worked with FTX, including the law firm Sullivan & Cromwell, which the group later dropped for a lack of evidence.

Fenwick argued the proposed updated complaint is “untimely — based on stale information that has been available to them for years — but also misleading and futile.”

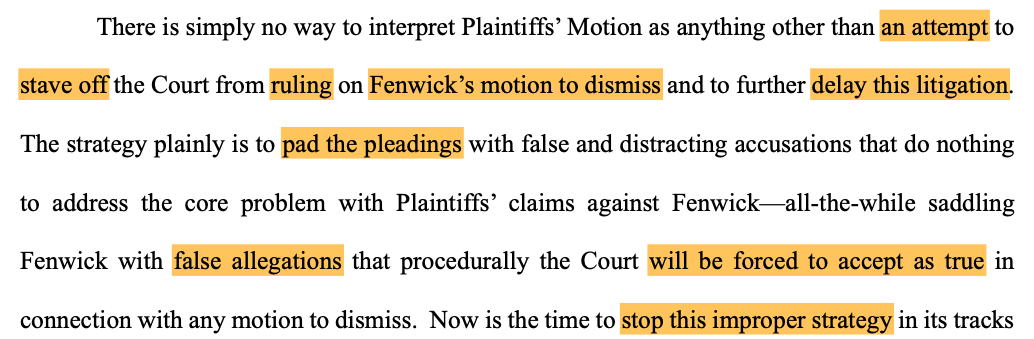

A highlighted excerpt of Fenwick’s claims that FTX users are looking to delay the court. Source: CourtListener

Fenwick also noted the allegations against the firm “mirror” the ones they had used “quite aggressively” against Sullivan & Cromwell, before the group dismissed the action when a report concluded that Sullivan didn’t know about FTX’s fraud.

“They offer no credible reason why the same allegations should survive against Fenwick,” it added.

“False characterization” of FTX executive’s claims

Fenwick also denied that Nishad Singh, FTX’s lead engineer, had testified that Fenwick was aware and helped hide the “misuse of customer funds” and “improper loans” during FTX co-founder Sam Bankman-Fried’s criminal trial.

“Singh testified that Fenwick merely advised on how to structure founder loans, which are common instruments for closely held companies like FTX,” the firm said.

Related: US appeals time served sentences for HashFlare Ponzi schemers

It added that “dozens of witnesses” in Bankman-Fried’s trial testified that the fraud at FTX was carried out “without the knowledge of even FTX’s in-house counsel, other FTX employees, executives, and directors, FTX’s long-time accountants, and other outside law firms and professionals that worked closely with FTX. Fenwick is no different.”

Fenwick rejects new securities claims

Meanwhile, Fenwick said the proposed complaint’s new claims that it helped launch and promote the FTX Token (FTT) in violation of Florida and California securities laws were far-fetched, frivolous and should have been “asserted months — if not years — earlier.”

“These new claims come far too late,” it wrote. “If Plaintiffs truly thought they had state securities claims against Fenwick, they had every opportunity to allege them at the outset.”

It accused the group of adding the two new allegations after a judge dismissed all but the state securities laws claims against celebrities that allegedly promoted FTX.

“This is an eleventh-hour attempt to evade the Court’s ruling on the Celebrity Defendants’ motion to dismiss, and to recast lawyers as ‘promoters,’” Fenwick said. “But this theory too goes nowhere.”

Magazine: The $2,500 doco about FTX collapse on Amazon Prime… with help from mom

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.

More on the subject