Finance Redefined: The curious implications of algorithmic stablecoins, Dec. 2–9

Latest NewsPublishedDec 10, 2020

Some stablecoins are more useful than others.

This is the latest issue of Finance Redefined, Cointelegraph's DeFi-centric newsletter delivered to subscribers every Wednesday.

A relatively quiet week in DeFi finally has given me some breathing room to talk about a subject I’ve been postponing since almost the beginning of this newsletter, namely: What’s up with decentralized finance’s weird obsession with algorithmic stablecoins?

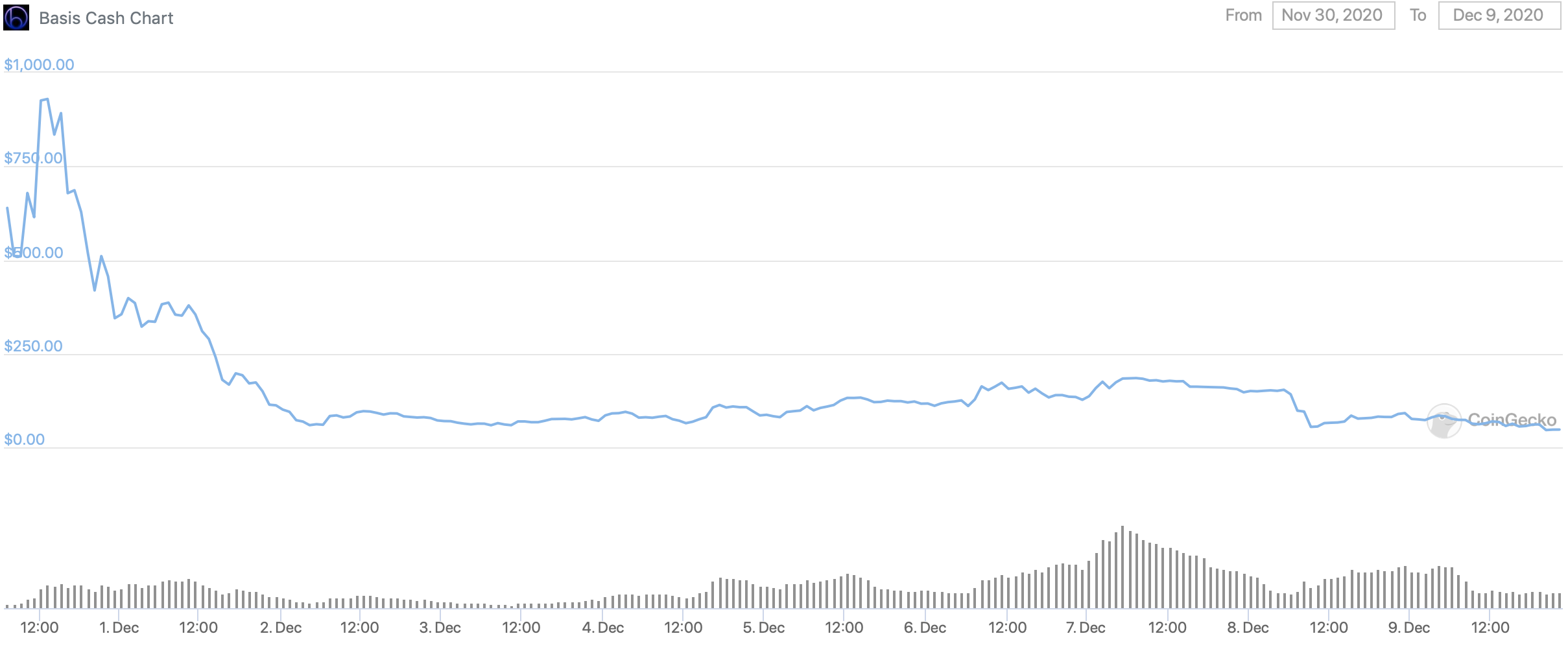

There are so many of them, and so many new projects get an unreasonable amount of attention. The latest is Basis Cash, which turned the heads of quite a few farmers this week.

BAC chart by CoinGecko. It’s supposed to trade at $1.

This week also saw the full launch of Neutrino’s NSBT governance token, which is used to backstop the reserves of the project’s stablecoins. Neutrino is not fully algorithmic, as it ultimately derives its value from its collateral of WAVES tokens. Dai is also not an algorithmic stablecoin for analogous reasons.

Algorithmic stablecoins, as defined by MakerDAO itself, use supply manipulation or market buying and selling to track a particular unit price — usually $1.

Perhaps the longest-running algorithmic token is Ampleforth (AMPL), though in the "Summer of DeFi" we also witnessed the creation of similar projects like Yam and Based. The basic principle of these coins is that smart contracts expand and contract the supply at predefined intervals. If oracles detect that the coin is trading for more than $1 or so, the supply expands. If it’s worth less, supply contracts.

The mechanism is called a rebase, and it is extremely powerful. Usually, it’s an adjustment of 10% of the deviation from $1, every day. So, if the price is $3, the supply changes by 20%, compounded every single day. That usually works pretty well to eventually bring it to $1.

For the Ampleforth and Yam family, supply changes affect every single wallet holding the coins. If you had 1,000 tokens one day, you may have 1,100 the next, without taking any action yourself. Basis is slightly different, as it limits the rebases to those who want to take the associated risks and rewards.

Now, Ampleforth never referred to itself as a stablecoin, preferring the categorization of “non-correlated asset.” But it does target the 2019 “value” of the U.S. dollar, and it is popularly called a stablecoin. The other projects are not so shy of that moniker.

Here’s the kicker: These assets are not stable, at all.

The quandary of creating something out of nothing

The fundamental purpose of a stablecoin — the one reason you would ever hold it — is to maintain a stable value. It just so happens that under normal circumstances, this means maintaining a stable price. The number of dollars in your bank account doesn’t really change, so the only thing affecting the account’s value is the dollar’s effective price.

The price of a stablecoin is essentially a red herring. It’s the value that matters. When in pursuit of a stable price you corrupt the supply portion of the equation, you achieve nothing. The total value of these stablecoins — the number you actually care about — is not pegged to anything.

As for Basis, so far we’re seeing that it’s not really good at maintaining the nominal peg either. It’s also worth mentioning Empty Set Dollar, which uses a mix of Basis’s and Ampleforth’s mechanisms. In terms of the peg it seems to be working relatively well, but we’ll see.

Ampleforth’s market capitalization would’ve also been your portfolio’s value.

These coins are a great example of the generalized principle of Goodhart’s law: “When a measure becomes a target, it ceases to be a good measure.”

But of course, who cares if they’re not actually stablecoins, right? It’s just semantics. The issue I’m seeing is that once you lack a stable asset, what exactly are you left with?

Proponents of these projects will point to the other uses of money beyond storage of value: unit of account (what you use to measure and compare economic quantities) and medium of exchange (what you pay your bills with). A good medium of exchange is an asset with a stable value, so that disqualifies these coins immediately.

Unit of account is a bit trickier, and on the surface, algorithmic stablecoins could work here. If your salary is in Yam, you’ll be fairly confident that you’ll receive more or less the same value every month.

Now, this only really works when algorithmic tokens are fringe assets. Imagine a country where everybody’s bank account balance changed by 10% every day. The fact that the nominal price of the currency is the same wouldn’t matter at all.

The choice of unit of account is particularly important for debt. If your debt is denominated in BTC and you have dollars, you have a short position on BTC. If it’s denominated in U.S. dollars and you have BTC, you have a leveraged long position.

Can we use algorithmic stablecoins to denominate debt? Well, not really. You have two choices: Either the debt follows the rebases or it doesn’t. The former case renders the entire concept useless, so we’ll ignore it. The latter is quite fun from a practical standpoint.

Imagine a positive rebase scenario: Yam is trading at $1.50, so every day it increases supply by 5%. Let’s also assume that the market is bullish and this price just won’t budge, which happens regularly. If you were to place your Yam in something like Compound, you’d abandon that 5% daily increase of your holdings, equal to a 1,825% annual percentage rate (and much more when compounded).

On the other side of the trade, you have the borrowers, who collect the rebases without being exposed to price drops. Would you really lend out your Yam in this scenario? Wouldn’t you rather borrow it? You can bet that the market would be extremely skewed toward borrowers, naturally pushing interest higher until it is roughly equal to the rebase yield.

This scenario is terrible for the average Joe who just wants a loan in a stable unit of account and immediately sells the Yam he borrowed. One day he’s paying 1% interest, the next 2,000%. The case in which the price falls below $1 is also not great. Borrowers would effectively be paying the entire negative rebase yield as interest. No one would take a loan at 1,000% APR, although the average Joe would be happy in this case.

Honestly, the complexity of integrating rebasing coins into a lending protocol is making my head spin. Borrowers and lenders will take turns at extracting immense value from each other due to the rebase mechanic, and the market will violently adjust to compensate. This whole thing just cannot work, although I’m certain people will try it anyway.

Both the lack of actual value stability and the funky stuff that happens with lending mean that algorithmic stablecoins are bad at being money. But they’re great at speculation, as they dilute price gains into yield for everyone. You won’t seriously miss out on any sudden hike, as you can just buy and hold through the rebases. Indeed you’re actually incentivized to buy when it’s above $1 and sell when it’s below $1, and that is not a recipe for stability.

Ultimately, it’s fine if people want to speculate on something. It’s just really important that they understand the game they’re playing with these tokens.

In other news

- Aave launches V2 of the lending platform with cool improvements: Unwinding positions is much easier, and collateral can be swapped on the fly.

- Cardano is taking steps to build its own DeFi ecosystem as it gets closer to enabling smart contracts.

- Solana, home of the Serum DEX, suffered a six-hour outage after consensus failure.

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.

More on the subject