Why the ABA says stablecoin yields could drain US bank deposits

LearnPublishedMay 27, 2026

Could yield-bearing stablecoins disrupt US banks? The ABA warns of deposit outflow risks, while policymakers see limited impact.

The financial theory behind yield-bearing stablecoins

The debate over price-stable digital assets has moved beyond technical discussions and into fundamental financial theory. The big question is what happens when people can earn returns by holding stablecoins.

The American Bankers Association (ABA) argues that this development could shift capital away from traditional bank deposits. If stablecoins begin offering returns comparable to those of standard savings accounts, banks could face deposit outflows. According to the ABA, this could affect their ability to fund loans and manage liquidity.

Policymakers, however, do not share a unified view. While banking trade groups warn of significant deposit outflows, some officials argue that the impact on credit availability may be limited. This disagreement reflects broader uncertainty about how yield-bearing stablecoins could affect the financial system.

Yield changes the basic dynamics of stablecoins

Stablecoins were initially designed to function as digital versions of traditional fiat currencies, mainly for payments, trading and settlement. In this role, they operate alongside the existing banking system rather than directly competing with it.

The introduction of yield, however, changes the equation.

When a dollar-pegged stablecoin starts offering returns, whether through built-in features or related arrangements, it begins to resemble an interest-bearing savings product. This shift has raised concerns among traditional banking groups such as the ABA.

Depositors, particularly those with large balances or a strong focus on earning returns, may begin comparing stablecoins with bank deposit accounts rather than viewing them simply as digital cash.

As a result, funds traditionally held in savings or money market accounts could begin moving toward tokenized dollar-based alternatives.

Did you know? Stablecoins were initially used mainly to provide stable-value liquidity within crypto markets rather than compete directly with bank deposits.

Why bank deposits matter for lending

At the heart of the issue is how banks operate. Customer deposits are an important source of funding that banks use to provide loans to individuals and businesses.

Banks rely on a steady supply of relatively low-cost, stable deposits to support lending. If deposits decline, banks may need to rely on more expensive funding or reduce the amount of credit they provide.

This potential loss of deposits is the ABA’s main concern. Even if the money remains within the broader financial system, moving it out of traditional bank accounts could make it harder or more expensive for some banks to fund loans.

Stablecoin yields and the risk of deposit migration

The process that could lead people to move money out of traditional bank deposits is straightforward. Users compare the returns available to them. If bank accounts offer modest interest while stablecoins offer higher or more flexible returns, some users may have a stronger reason to move their funds.

Beyond potential returns, stablecoins may offer practical benefits, including faster transfers, 24/7 access and links to blockchain-based financial tools.

As stablecoin use expands, moving money between traditional bank accounts and stablecoins may become easier, reducing the barriers to shifting funds.

Together, these factors could make stablecoins more competitive in terms of both convenience and returns. This combination may increase the risk of deposits moving away from banks.

Which bank deposits are most exposed?

Not every type of bank deposit faces the same level of exposure. Funds held mainly to earn returns are likely to be more sensitive to competing yield opportunities.

Interest-bearing deposit categories, such as savings accounts and money market deposit accounts, along with large uninsured balances, may respond more quickly to differences in returns. These funds are often monitored closely and may move more easily when alternatives appear more attractive.

Everyday transaction accounts, such as standard checking accounts, are likely to remain more stable at first. However, if stablecoins continue to become easier and more convenient to use, even these routine balances could face greater pressure over time.

The extent of any movement will ultimately depend on how competitive stablecoin products become compared with traditional banking options.

Did you know? Major stablecoin issuers hold a big portion of their reserves in short-term US Treasury bills. This means that even if some funds move out of bank deposits, part of that money may still support government borrowing rather than leaving the broader financial system entirely.

Why smaller banks could be hit harder

The effects of any deposit outflows would likely vary across different types of banks.

Larger institutions typically have more diverse funding sources and easier access to wholesale capital markets. By contrast, smaller and community banks often rely more heavily on deposits from local customers.

For these smaller banks, even relatively limited outflows could create greater challenges. A decline in deposits may make it harder or more expensive to provide loans to local businesses and households.

This uneven impact is an important part of the ABA’s position. Its concern is not limited to the total volume of deposits that could move, but also includes the specific banks and communities that could lose access to funding.

If yield-bearing stablecoins gain widespread use, a meaningful share of rate-sensitive deposits could face greater competition. This supports the ABA’s view that stablecoins offering both returns and payment features could become an alternative place for consumers and businesses to hold funds.

Did you know? Unlike traditional bank deposits, stablecoins can generally be transferred globally at any time. This round-the-clock availability may make it easier for some users to move funds quickly when more attractive returns become available.

The opposing view: Limited overall impact

Not every assessment reflects the same level of concern. Some policymakers argue that the risk to bank lending may be far smaller than industry groups suggest.

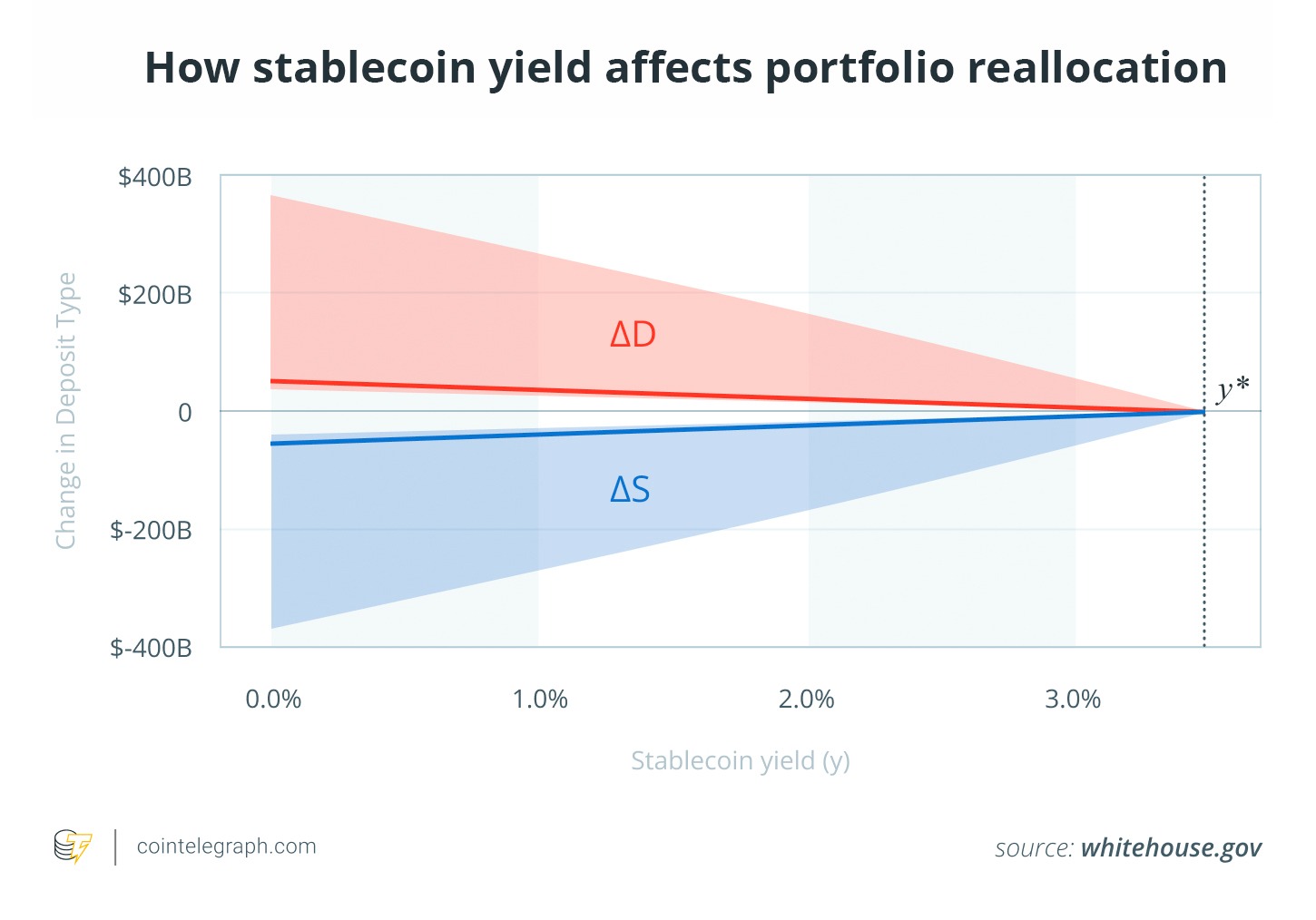

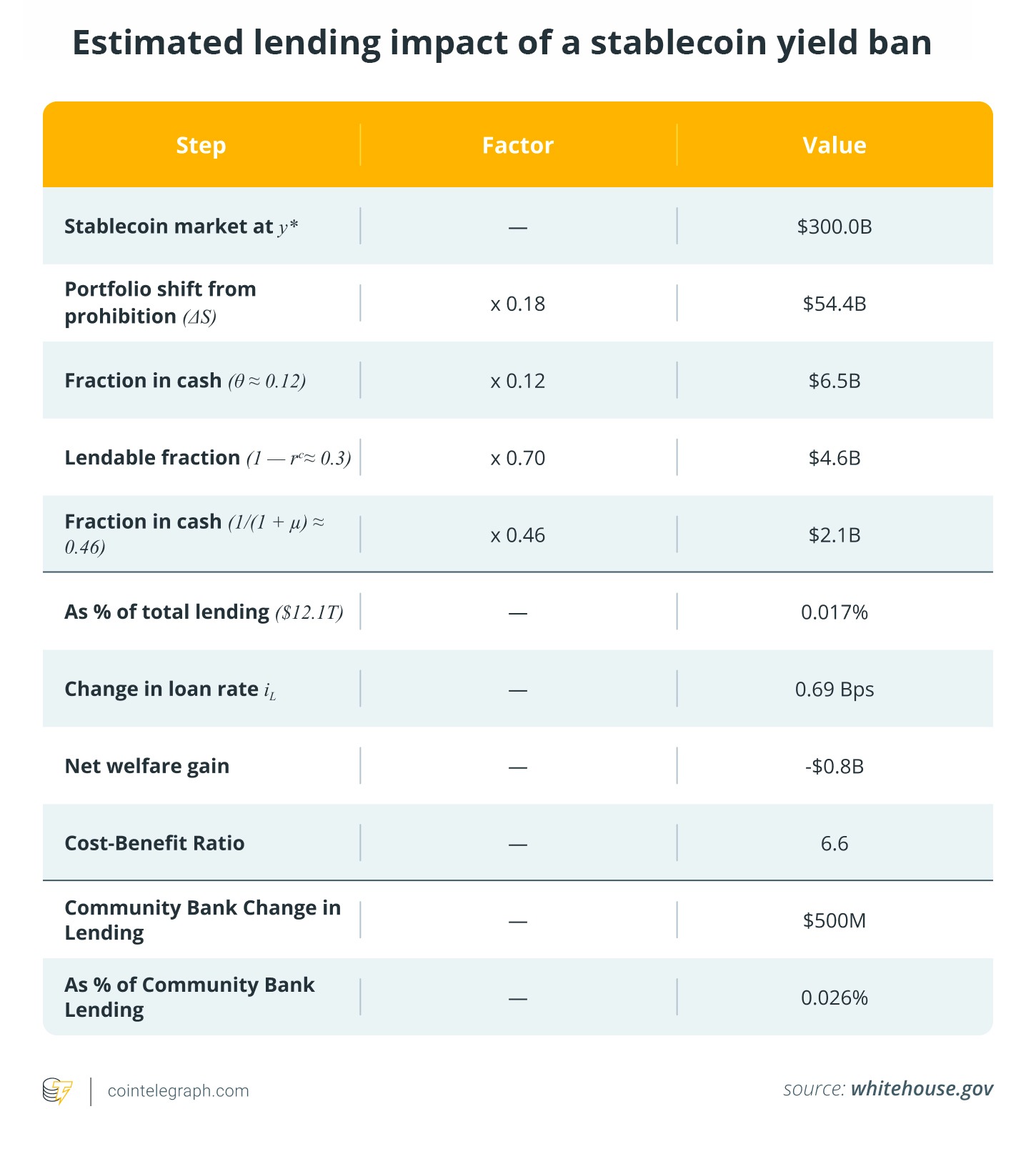

An analysis by the White House Council of Economic Advisers offers a more restrained outlook. Its calculations suggest that limiting stablecoin yields would increase bank lending by approximately $2.1 billion, equivalent to roughly 0.02% of total loans.

From this perspective, the broader effect of stablecoin competition on credit availability appears relatively limited. The key argument is that money used to back stablecoins does not simply disappear from the financial system. It is generally held in reserve assets such as bank deposits or short-term Treasury securities, keeping it within the broader financial ecosystem.

This suggests that while the composition of financial holdings may change, the overall impact on lending capacity would likely remain limited.

Where the disagreement lies

The difference between the ABA’s position and the White House analysis comes from how each evaluates the financial system.

The ABA focuses on the type and distribution of funding. It emphasizes the importance of stable, low-cost deposits in supporting lending, particularly for smaller banks.

The White House analysis, by contrast, focuses on system-wide totals. It examines how capital moves across the broader financial system and concludes that the overall impact on lending would remain limited.

Each view is based on different assumptions about how stablecoins may develop and how users are likely to respond.

Beyond returns: The broader shift

Although yield is the immediate point of debate, the broader challenge goes beyond returns.

Stablecoins are more than alternatives to savings products. Their programmable features, ease of transfer and connection to digital financial services may make them more attractive to some users than traditional bank accounts.

In this context, yield may act as an accelerator rather than the sole cause of change. It could speed up an existing shift toward forms of money that are easier to move and use across digital platforms.

What this debate means for regulators

This shift has made stablecoin oversight a central issue in regulatory debates.

Recent legislative proposals in the US have sought to restrict or prohibit interest payments on payment stablecoins. The aim is to preserve a distinction between traditional bank deposits and digital instruments designed primarily for payments.

Banking groups such as the ABA have also called for stricter rules to prevent indirect yield arrangements offered through affiliated entities or incentive programs. Their concern is that without clear boundaries, stablecoins could serve functions similar to bank deposits while operating under a different regulatory framework.

The outcome of this debate will help determine how directly stablecoins can compete with traditional banking products.

How stablecoin yields could reshape banking

From the ABA’s perspective, offering yield on stablecoins marks a critical turning point.

As long as stablecoins mainly serve as tools for payments and transfers, they can operate alongside the traditional banking system with limited friction. However, once they begin offering returns comparable to those of bank deposits, they may compete more directly for both retail and institutional funds.

It remains uncertain whether this shift would lead to significant deposit outflows. The debate reflects two opposing views: One emphasizes potential risks to the banking model, while the other suggests that the overall effect on lending and the wider financial system would be limited.

The line between digital money and yield-generating financial products is becoming less clear. As stablecoins continue to develop, the key question is no longer only how they work, but also how they could change where people and institutions choose to hold their money.

This article is produced in accordance with Cointelegraph's Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

More on the subject