Why banks are fighting stablecoins after shaping the rules

LearnPublishedMay 21, 2026

Stablecoin rules may legitimize crypto dollars enough to compete with banks for payments, savings and customer relationships.

How the digital dollar debate has shifted

For a long time, major banks urged Congress to impose strict rules on stablecoins. Industry associations highlighted the risks of privately issued digital dollars operating beyond conventional banking oversight. They called for mandatory reserve requirements, robust anti-money laundering measures and tighter regulatory supervision.

Now that US stablecoin legislation is moving closer to approval, some banks are confronting a consequence they may not have fully welcomed: Regulated stablecoins could become serious rivals to conventional bank deposits.

The Senate Banking Committee’s 309-page CLARITY Act discussion draft shows how central this issue has become. The draft proposes rules for digital assets, stablecoins and crypto platforms in the US. One of the biggest debates is whether stablecoin users should be allowed to earn returns that resemble interest.

At its core, the debate is about control over the future of money, payments and banking influence.

Why banks initially backed stablecoin regulation

Banks’ support for oversight was not just about opposing new technology. Their primary concern was that stablecoins were creating an alternative financial system without the same rules and protections applied to traditional banks.

Assets such as USDt and USDC are now deeply embedded in crypto trading, international transfers and decentralized finance (DeFi). Their total market value has grown large enough to rival the balance sheets of several mid-tier banks.

From the banking sector’s viewpoint, this raised several red flags:

- Are the reserves fully and safely backed?

- Could stablecoins trigger rapid digital bank runs?

- Would issuers comply with anti-money laundering (AML) standards?

- Could unregulated shadow banking risks develop?

As a result, banks advocated for rules that would bring stablecoins closer to established financial regulations, including regular audits, licensing and restrictions on high-risk activities.

Many institutions also saw potential upsides. They anticipated roles in managing reserves, offering custody services, forming partnerships with issuers or even issuing their own stablecoins through regulated subsidiaries. At that point, stablecoins appeared more like infrastructure that banks could help shape and benefit from, rather than direct threats.

Did you know? Most commercial banks create money primarily through lending, not by printing cash. This is why customer deposits matter so much. If stablecoins absorb deposits, banks may need to rely on more expensive funding sources to maintain lending activity.

Why stablecoin yield worries banks

Sentiment began to shift as discussions turned to allowing stablecoin holders to earn yield-like returns. This matters because meaningful rewards could change stablecoins from basic transaction tools into attractive substitutes for savings accounts. Users might then park more funds on crypto platforms instead of in traditional bank accounts.

That prospect worries banks, since deposits remain a vital and relatively low-cost source of funding. Banks rely on them to extend loans, finance mortgages, support commercial lending and handle everyday operations. A significant outflow of deposits would likely raise their overall funding costs.

This is why several banking organizations now oppose proposals that would let stablecoin issuers or platforms offer interest-like incentives outside the conventional banking framework.

The conflict has moved beyond simple crypto regulation. It is increasingly about which institutions will be allowed to provide digital dollars with financial returns attached.

Why banks worry customers may move their money

Stablecoins are gaining appeal by offering capabilities that conventional banks often find difficult to replicate:

- Round-the-clock, instant settlement

- Rapid cross-border payments

- Programmable money features

- Seamless blockchain connectivity

- Easy access to digital asset ecosystems

If these digital dollars start providing yield, financial institutions fear that savers may slowly move funds out of regular bank accounts and into tokenized versions instead.

Analysts have flagged potentially significant long-term effects. For instance, Standard Chartered reportedly estimated that American banks could see up to $500 billion in deposit outflows to stablecoins by 2028 if growth continues at pace.

Even if such forecasts turn out to be overstated, the underlying issue remains: Stablecoins could weaken the longstanding ties between banks and their customers.

Traditionally, banks have dominated key functions such as holding deposits, handling payments, managing savings and controlling the flow of dollars. Stablecoins could put pressure on several of these functions at the same time.

Did you know? Stablecoins already settle billions of dollars daily across global crypto markets. Unlike traditional banking systems, many blockchain networks operate continuously, allowing transfers 24 hours a day, including on weekends and holidays, without relying on banking hours.

Banks claim stablecoins could hurt overall lending

Banking associations tend to present their objections as concerns about systemic stability, not simply business competition. They emphasize that customer deposits are essential for supporting lending across the economy.

If these deposits migrate to stablecoins, banks could have less funding available for mortgages, small business loans, farm financing and everyday consumer credit. Regional and community banks could face the greatest pressure, given their dependence on steady local deposit bases.

From this perspective, allowing yield on stablecoins could draw money out of the heavily regulated banking system and into vehicles that do not face the same capital and liquidity standards.

Banks are particularly wary of workarounds. Even if direct interest payments by stablecoin issuers are banned, trading platforms could still introduce incentive or reward schemes linked to holdings. Industry groups argue that this would undermine regulatory intent. They believe stablecoins should remain primarily tools for transactions, not substitutes for interest-bearing savings accounts.

The White House sees it differently

Not all experts share the banks’ level of alarm. The White House’s Council of Economic Advisers recently indicated that prohibiting yield on stablecoins would likely deliver only limited benefits to bank lending capacity.

The council’s assessment is that banning stablecoin yield may keep some funds in bank deposits, but the effect on overall lending would likely be limited because the US banking system is already so large.

This cuts against one of the banks’ main arguments. They say stablecoin yield could weaken credit availability across the economy.

Critics argue that some banks may be overstating the risks, driven more by a desire to protect lucrative deposit franchises than by genuine concerns about financial stability. From the crypto sector’s perspective, traditional banks are mainly trying to protect their established dominance in payments and savings services.

The administration appears keen to foster agreement instead of escalating tensions between traditional banks and crypto companies.

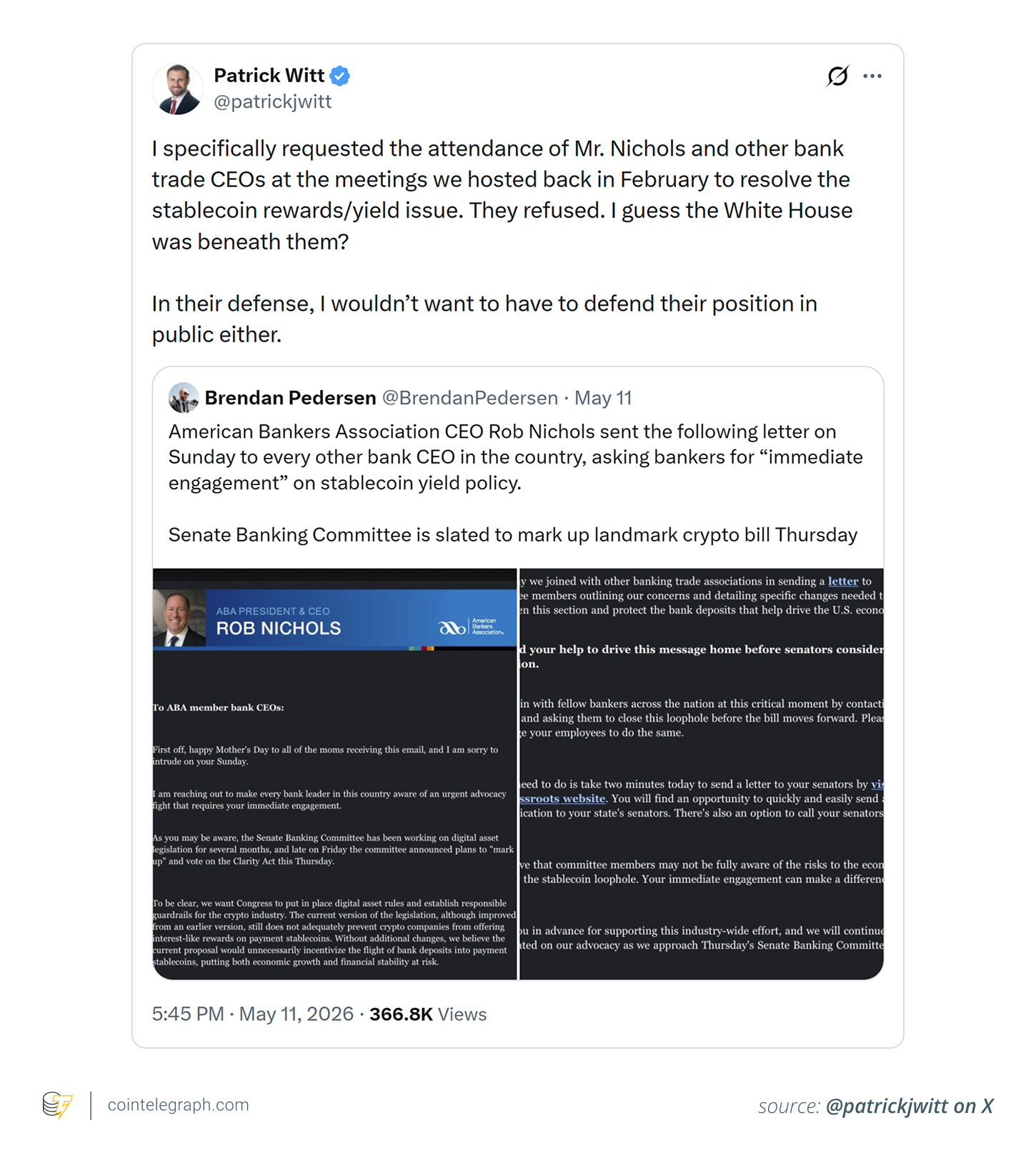

Patrick Witt, head of the President’s Council of Advisors for Digital Assets, recently noted that crypto firms have already eased some of their positions on stablecoin yield. He urged banks to respond with similar flexibility to help push the legislation through.

Witt added that the financial system of the future will likely be defined by greater integration between crypto and conventional banking, rather than sustained competition.

How regulation could boost stablecoins

Banks pushed for tighter oversight to contain stablecoin risks. But clearer rules could have the opposite effect by giving stablecoins greater legitimacy among institutions, businesses and mainstream users.

Clear rules tend to reduce uncertainty for a wide range of players, including financial institutions, payment companies, retailers, fintech startups and major corporations. With greater legal certainty, more businesses may feel confident using stablecoins in their everyday operations.

This creates an irony: Banks sought regulation mainly to curb potential risks to the financial system. Yet the same rules could legitimize stablecoins and turn them into even stronger rivals.

In effect, the banking sector may have inadvertently accelerated the integration of digital dollars into traditional finance.

Did you know? Some lawmakers want stablecoins to be treated mainly as payment tools rather than savings products. The debate over whether users should earn yield on stablecoins has become one of the biggest flashpoints in US crypto regulation.

How the crypto industry sees the debate

Crypto companies argue that banks are presenting a competitive threat as a stability concern. Stablecoin proponents, on the other hand, highlight their potential to improve cross-border payments, settlement speed and broader financial inclusion.

Another argument in favor of stablecoins is that they may give customers better options than low-yield bank savings accounts in a higher interest-rate environment.

From their standpoint, blocking rewards on stablecoins does more to protect traditional banking profits than to safeguard users. They believe programmable digital dollars can reduce costs and friction in global payments in ways traditional payment systems may not always match.

Ultimately, the disagreement comes down to two opposing views: Banks see stablecoins as possible sources of instability, while crypto proponents see them as innovative financial infrastructure.

What stablecoin users need to understand

For the public, this debate matters because it will shape the digital money tools available in the future.

Stablecoins bring clear benefits, such as quick transfers, global reach, blockchain-based features and tight integration with digital economies. However, they are not the same as traditional bank deposits.

Important differences include:

- No Federal Deposit Insurance Corporation (FDIC) coverage on stablecoin holdings

- Potential for issuers to restrict or freeze specific addresses

- Varying redemption processes

- Different approaches to reserve backing

Users should therefore treat stablecoins as distinct financial products. They may look like digital dollars, but they are governed by different rules and risks than insured bank accounts.

The bigger battle over digital money

This discussion is moving far beyond technical crypto rules. It is becoming a broader contest over who will shape the next era of financial infrastructure.

Banks have long held power over deposits, payments and money movement because these activities traditionally required large centralized institutions. Blockchain-based stablecoins challenge that model by enabling fast, programmable transfers across global networks without relying on conventional banking channels.

Banks originally supported bringing stablecoins under regulation to promote safety and control. Now they must confront the possibility that those same regulations could help turn stablecoins into widely accepted mainstream alternatives.

This is why the debate has grown more intense. The central issue is no longer whether stablecoins will exist, but whether they will remain limited to niche payments or develop into a fuller form of digital money.

This article is produced in accordance with Cointelegraph's Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

More on the subject