JPMorgan rates Circle underweight with $80 target by late 2026

Latest NewsPublishedJun 30, 2025

While seeing Circle as well-positioned in the market, JPMorgan analysts warned that competition is a potential threat to the stablecoin issuer.

Analysts at JPMorgan, a major US investment bank, have initiated coverage of Circle (CRCL) shares with an underweight rating and a $80 price target by December 2026.

JPMorgan’s analysts, led by Kenneth Worthington, on Monday presented their first formal Circle stock analysis in the “North America Equity Research” report, seen by Cointelegraph.

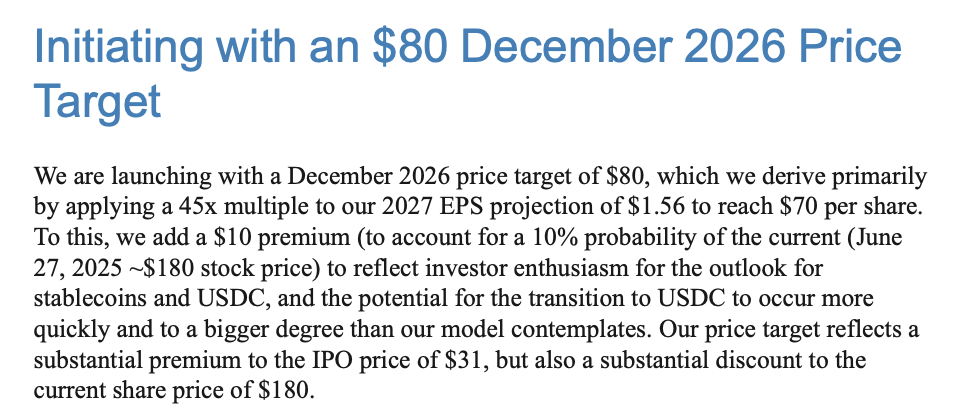

Down 55% from the current CRCL price of $180, the forecast is based on a 45x multiple of projected 2027 earnings per share (EPS) plus a $10 premium for upside potential.

An excerpt from JPMorgan’s North America Equity Research seen by Cointelegraph. Source: JPMorgan

“Our price target reflects a substantial premium to the IPO price of $31, but also a substantial discount to the current share price of $180,” the analysts wrote.

$21 billion market cap expected by late 2026

While seeing Circle as well-positioned in the nascent stablecoin market, given its early-mover advantage and numerous use cases, JPMorgan analysts suggested that its current market capitalization is elevated.

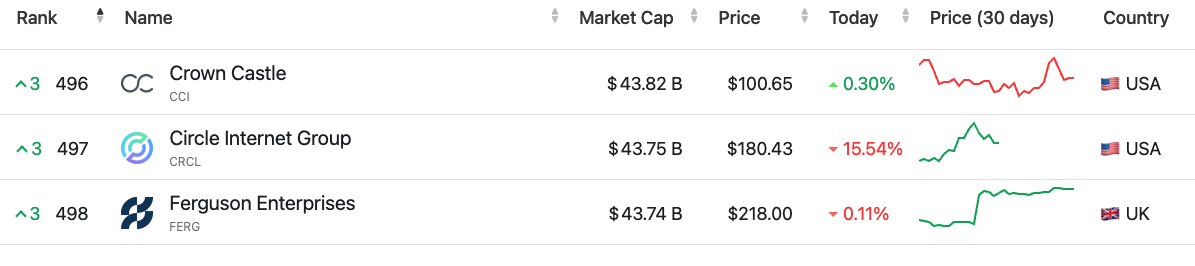

According to data from CompaniesMarketCap, Circle is valued at $43.8 billion, showing massive growth after CRCL shares started trading on the New York Stock Exchange (NYSE) with an $8 billion market cap on June 5.

Circle is the 497th largest company worldwide by market capitalization. Source: CompaniesMarketCap

“Our Dec-2026 price target of $80 implies a market cap of approximately $21 billion. We note that the mid-point of the IPO [initial public offering] was priced at $31 or an $8 billion market cap,” the analysts stated.

Competition as a potential threat to Circle

To justify their underweight rating of Circle, JPMorgan analysts mentioned a few developments that could potentially harm the company’s market value in the coming months, including implications of market competition.

“We see competition as a potential threat to Circle,” the analysts stated, referring to not only direct stablecoin competitors, but also other crypto investment products like tokenized deposit accounts and digital money market funds.

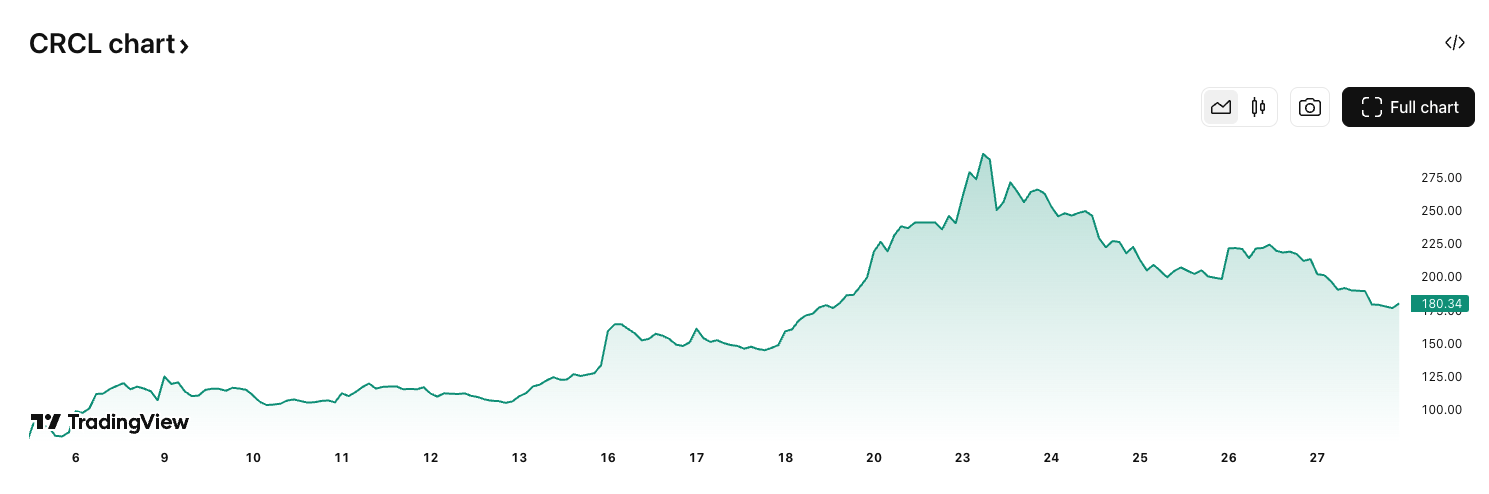

Circle (CRCL) shares tumbled 15.5% Friday after peaking above $290 in mid-June. Source: TradingView

Related: Coinbase stock approaches all-time high following 42% year-to-date gain

“The risk is that a few will succeed in taking enough share to reach critical mass in a business with low switching costs, allowing them to leverage the network built by Circle,” the analysts said.

CBDCs among the risks

Among other risks, JPMorgan referred to US stablecoin regulations, which may soon require issuers like Circle to hold equity capital based on the amount of stablecoins in circulation, similar to Europe’s Markets in Crypto-Assets (MiCA) regulation.

While JPMorgan estimated Circle has enough equity to support its USDC (USDC) stablecoin held in the US, the analysts suggested that higher capital requirements could restrict USDC growth.

Additionally, the analysts highlighted certain risks stemming from the development of central bank digital currencies (CBDCs). Although the US has taken a stablecoin-friendly approach to support the strength of the US dollar, other countries could potentially add some pressure to Circle’s expansion worldwide, JPMorgan’s report noted.

“Further global CBDC adoption, particularly in Europe, could impact Circle’s ability to scale globally, adversely impacting long-term growth and profitability,” the analysts wrote.

Magazine: Crypto wanted to overthrow banks, now it’s becoming them in stablecoin fight

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.