Banks fear stablecoin ‘bank run,’ regulators see limited impact

Latest NewsPublishedJan 28, 2026

Banks warn stablecoins could siphon deposits from the banking system, but policy and regulatory experts say there’s little evidence of it happening yet.

Banks warn that stablecoins, especially those paying yield, could pull deposits out of the banking system, but policy and finance experts say there’s little evidence of that so far.

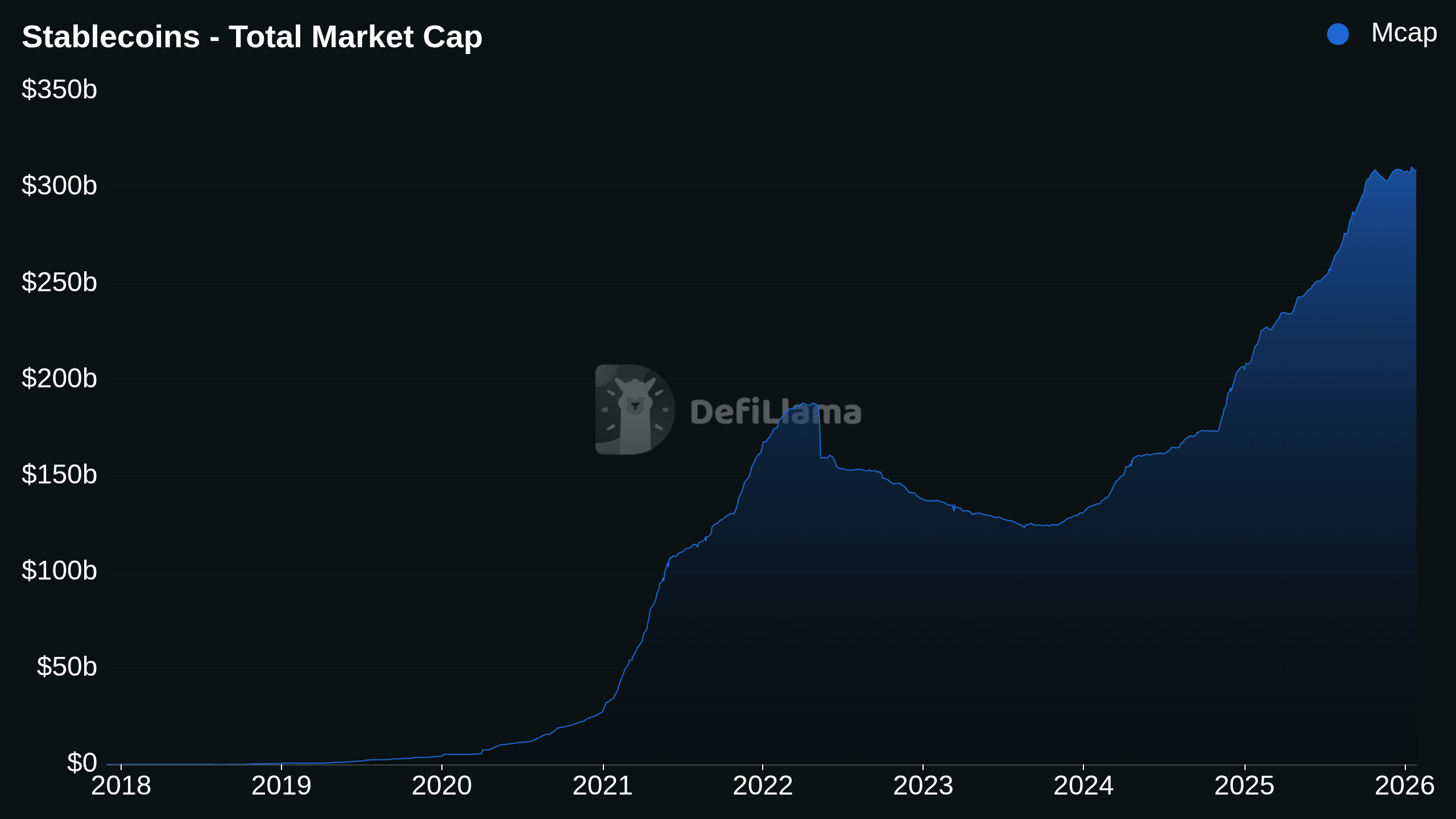

Major US bank Standard Chartered recently estimated in a research note that increasing stablecoin adoption could drain bank deposits. The report estimates “that US bank deposits will decrease by one-third of stablecoin market cap,” which stood at $308.15 billion at time of writing, according to DeFiLlama data.

The debate has intensified as US lawmakers weigh whether to prohibit interest on stablecoin holdings under a proposed version of the crypto market structure bill, or CLARITY Act, which has been delayed by protests from inside the crypto industry despite banking sector support.

Banks argue that allowing yield-bearing stablecoins could accelerate deposit flight, while critics say the risk remains largely theoretical.

Limited evidence of deposit outflows

Aaron Klein, a senior fellow in economic studies at the policy research institution Brookings, told Cointelegraph that so far, stablecoins have primarily been used for crypto-related activities and as a store of value in non-dollar countries. “You will find little evidence that stablecoins have drained bank deposits,” he said.

Related: US bank lobby says stopping stablecoin yields a top 2026 priority

European regulators may share a similar view. A representative of the European Banking Authority (EBA) said stablecoins in the European Union are mainly treated as payment instruments within the crypto ecosystem and remain lightly used by consumers. “Because of low engagement in [or] use of stablecoins currently within the EU, we do not see current currency substitution, capital flight or dollarisation risks,” they said.

Still, Klein suggested that this is subject to change. He highlighted that what can be found are “arguments that if stablecoins take off as their supporters claim they will, then it will likely result in a drain in bank deposits.”

Klein said this would reduce capital availability, as “bank deposits support bank lending, so reduced bank deposits reduce the supply of credit available through bank-based products.”

Similarly, the EBA representative told Cointelegraph that if stablecoin use were to increase significantly, it would give rise to potential “financial stability risks from stablecoins jointly issued by EU and non‑EU entities.”

Total stablecoin market cap chart. Source: DeFiLlama

Those risks would include bank-run risk, cross-border legal frictions, regulatory arbitrage and supervisory challenges. The EBA representative said that dollarization is primarily a concern for emerging markets and that a “shift away from euro‑denominated settlement assets toward US dollar‑backed stablecoins is not foreseen in the EU.”

Related: Who gets the yield? CLARITY Act becomes fight over onchain dollars

Stablecoin proponents disagree

Colin Butler, head of markets at Mega Matrix, said banning compliant stablecoins from offering yield would sideline regulated institutions while accelerating capital migration beyond US oversight and failing to protect the US financial ecosystem.

Jeremy Allaire, CEO of the publicly listed stablecoin issuer Circle, recently said that interest payments on stablecoins do not pose a threat to banks.

Speaking on the World Economic Forum stage in Davos, Allaire said that such bank-run concerns are “totally absurd.” He said that yields “help with stickiness, they help with customer traction,” but cannot undermine monetary policy.

Earlier this month, Anthony Scaramucci, founder of asset manager SkyBridge Capital, said that banks simply “do not want the competition from the stablecoin issuers, so they’re blocking the yield.”

In January, the People’s Bank of China, the country’s central bank, allowed commercial banks to pay interest on digital yuan deposits. Scaramucci suggested that this leads to China having an advantage over the US.

“In the meantime, the Chinese are issuing yield, so what do you think the emerging countries will choose as a rail system, the one with or without yield,” he said.

Magazine: Hong Kong stablecoins in Q1, BitConnect kidnapping arrests: Asia Express

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.

More on the subject