World Bank Digs Deeper Into DLT and FinTech for Financial Inclusion

Latest NewsPublishedApr 14, 2020

The world’s largest development bank, the World Bank Group, has issued a new report on payment aspects of financial inclusion in the fintech era.

Financial institutions all over the world are increasingly experimenting with emerging technologies like blockchain to streamline payment systems and achieve financial inclusion. In a new study, the World Bank has once again emphasized blockchain’s potential for financial inclusion.

Issued by the Bank for International Settlements on April 14,the new report from the World Bank Group on “Payment aspects of financial inclusion in the fintech era” outlines a wide number of crypto and blockchain-related concepts like stablecoins and central bank digital currencies (CBDC). In the 70-page report, the bank provided a detailed overview of selected advances in technology that are considered to be the most relevant to payments as well as described their applications and associated risks.

Extended version of 2016 PAFI report

The new report reiterates and enhances the guidance developed in the report on Payment aspects of financial inclusion (PAFI) issued by the World Bank in collaboration with Committee on Payments and Market Infrastructures (CPMI) in 2016. Basically, the latest report sets out fintech-focused key aspects, putting them in the context of the general PAFI guidance, which was formulated in a tech-neutral way and did not include developments like blockchain.

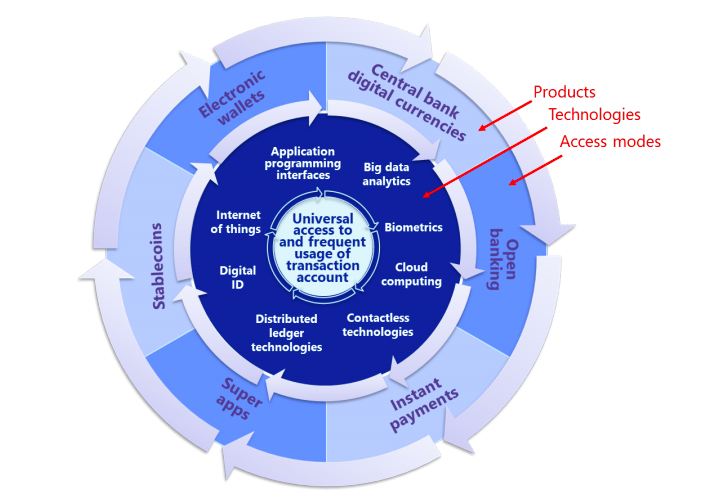

Among major PAFI tools, the World Bank listed distributed ledger technology (DLT), stablecoins, CBDCs and payment tokenization systems, placing them in line with other fintechs like big data analytics and cloud computing. Combining several technologies, products and access models, the World Bank drew up the so-called “PAFI fintech wheel” to identify fintech developments that are potentially relevant to the payment aspects of financial inclusion.

WBG’s “PAFI fintech wheel.” Source: Bank of International Settlements

Stablecoins prompted CBDC investigations for more efficient cross-border payment

Specifically, the report says that DLT “may further spur business model innovation in cross-border payments,” noting that the technology has a potential to streamline such payments in a permissioned, i.e. private environment.

The World Bank also pointed out the role of stablecoins and CBDCs in cross-border transactions, emphasizing that existing stablecoin projects like Facebook’s Libra pushed some jurisdictions to accelerate CBDC investigations to fix major issues of cross-border payments. Neither a global retail stablecoin project nor a CBDC live network is operational to date, the bank noted.

The report reads:

“Stablecoins have prompted central banks in some countries to accelerate their investigations into CBDCs and generally resulted in greater attention being paid to the challenges of financial inclusion and more efficient cross-border payments [...] No global retail stablecoin initiative is currently operational.”

Interestingly, the Bank for International Settlements found out in March 2020 that no existing CBDC project explicitly focuses on cross-border payments so far, as those initiatives do not go beyond the central bank’s jurisdiction.

World Bank’s previous interest in blockchain to drive financial inclusion

The World Bank’s fintech-focused report on financial inclusion is not the organization’s first foray into blockchain and associated emerging technologies.

In late 2017, the World Bank published an extensive blockchain report titled “Distributed Ledger Technology and Blockchain,” emphasizing that DLT implementation for financial inclusion goals requires the development of important accompanying components like interoperability with traditional payment services and effective oversight. The report also describes in detail major cryptocurrencies like Bitcoin (BTC) and Ether (ETH), as well as their public blockchains.

Subscribe to daily byte-sized crypto news from Cointelegraph

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.